Full News

Customs Appeal No. 42305 of 2013: Rejection of Declared Value Set Aside

Customs Appeal No. 42305 of 2013: Rejection of Declared Value Set Aside

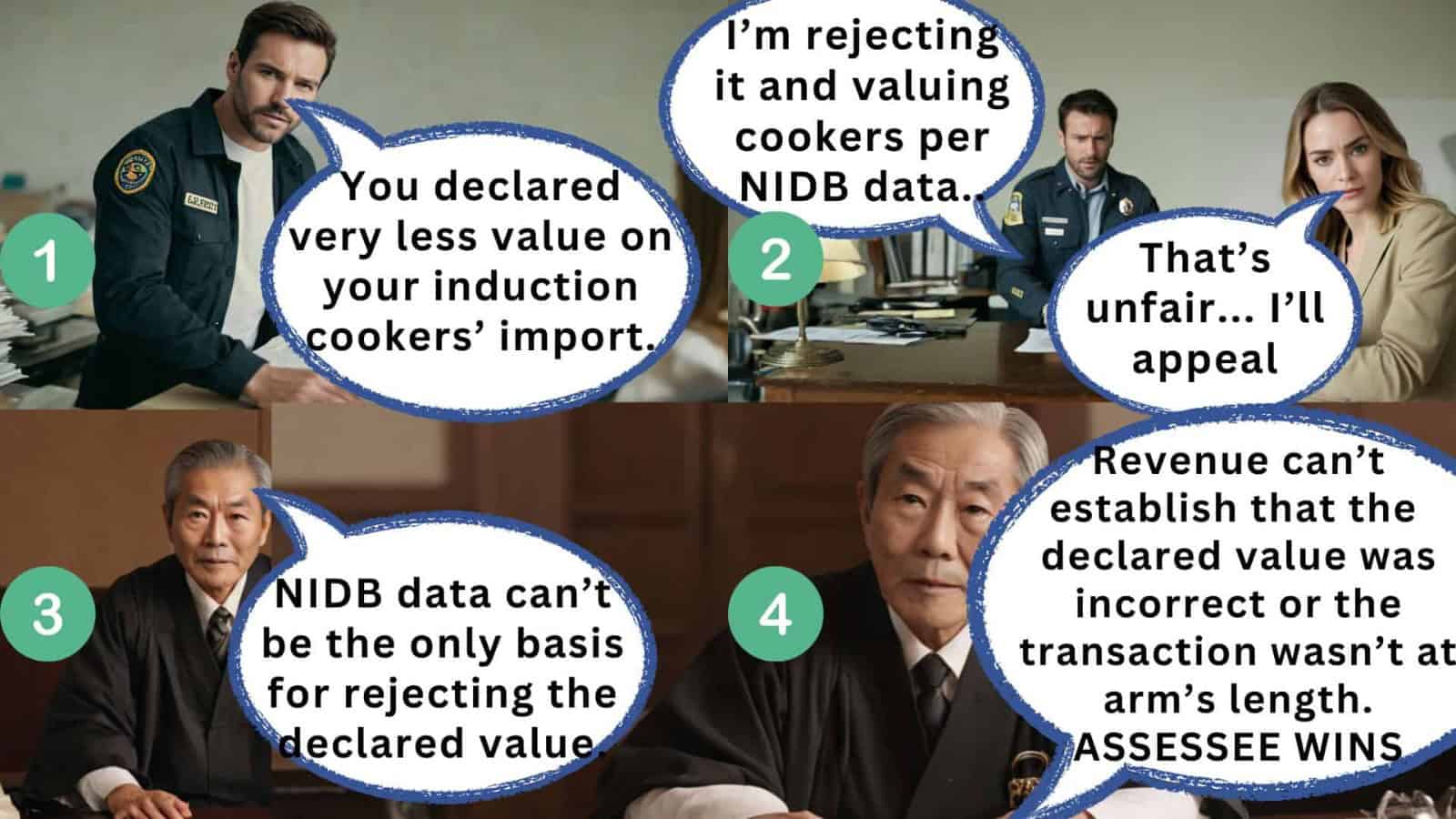

The Customs, Excise and Service Tax Appellate Tribunal in Chennai ruled in favor of M/s. Atlantis Trading Company in Customs Appeal No. 42305 of 2013, setting aside the rejection of the declared value of imported goods by the Revenue. The rejection was solely based on NIDB data, which the Tribunal found to be an insufficient basis for the rejection of the transaction value.

Case Name:

M/s. Atlantis Trading Company v. Commissioner of Customs, Custom House, Tuticorin

Key Takeaways:

- NIDB data alone cannot be the sole basis for rejection of the transaction value.

- The Revenue must establish a case for the rejection of the declared value and re-determination of the same.

- The rejection of the declared value solely based on NIDB data was found to be unjustified.

- The Tribunal set aside the impugned order and allowed the appeal with consequential benefits, if any, as per law.

Case Synopsis:

The appears to be a legal document related to a customs appeal filed with the Customs, Excise and Service Tax Appellate Tribunal in Chennai. The appeal number is C/42305/2013-DB, and it is against the Order-in-Appeal No. 152/2013 dated 20.08.2013 passed by the Commissioner of Customs and Central Excise (Appeals), Tiruchirappalli.

The appellant in this case is M/s. Atlantis Trading Company, located at Door No. 6/565, Thrikkankode Road, P.O. Manissery, Ottapalam, Palakkad, Kerala – 679 521. The respondent is the Commissioner of Customs, Custom House, New Harbour Estate, Tuticorin – 628 004.

The appeal was heard by HON’BLE MR. P. DINESHA, MEMBER (JUDICIAL) and HON’BLE MR. M. AJIT KUMAR, MEMBER (TECHNICAL). The final order number is 40988 / 2023, and the date of hearing was 13.10.2023, with the date of decision being 03.11.2023.

The main issue in this appeal was the rejection of the declared value of the imported goods by the Revenue and the consequent determination of the value by the original authority. The appellant contested the re-valuation of the impugned goods imported by it, which was done by the Assistant Commissioner, vide Order-in-Original No. 03/2013-A.C.(Imports) dated 27.03.2013.

The Assistant Commissioner rejected the declared value of the goods based on NIDB data, which showed similar goods being cleared at a higher rate. However, the appellant argued that the declared value was not false or incorrect and provided imports of similar goods by various other importers, the value of which almost matched with that of the appellant. The Tribunal found that the rejection of the declared value solely based on the NIDB data was not justified.

The Tribunal cited previous cases and held that the NIDB data alone cannot be the basis for rejection of the transaction value. It also stated that the Revenue had not made out a case for the rejection of the declared value and re-determination of the same. Therefore, the impugned order was set aside, and the appeal was allowed with consequential benefits, if any, as per law.

FAQ:

Q1: What was the basis for the rejection of the declared value?

A1: The rejection was solely based on NIDB data, which showed similar goods being cleared at a higher rate.

Q2: What was the appellant’s argument against the rejection of the declared value?

A2: The appellant argued that the declared value was not false or incorrect and provided imports of similar goods by various other importers, the value of which almost matched with that of the appellant.

Q3: What was the Tribunal’s ruling in this case?

A3: The Tribunal ruled in favor of the appellant, setting aside the rejection of the declared value and allowing the appeal with consequential benefits, if any, as per law.

×

Similar Ripples

Questions

Customs Appeal No. 42305 of 2013: Rejection of Declared Value Set Aside

Write your CommentSimilar Posts

Generic

- Reportdata/42305-2013.pdf