Full News

Customs Tribunal remands case of restricted titanium powder import for fresh adjudication after DGFT decision.

Customs Tribunal remands case of restricted titanium powder import for fresh adjudication after DGFT decision.

M/s. Asok Sparklers Factory successfully appealed against the confiscation of imported titanium powder, a restricted item under import policy, for which they had not submitted a DGFT import license at the time of clearance. The importer argued that the authorities had incorrectly treated the restricted item as prohibited. Citing a Supreme Court decision, they distinguished between prohibited and restricted goods. The CESTAT set aside the original order and remanded the case back to the adjudicating authority, instructing them to await the DGFT's decision on the importer's pending license application before passing a fresh order.

Case Name:

Asok Sparklers Factory Vs Commissioner of Customs (CESTAT Chennai)

Key Takeaways:

- The case highlights the distinction between prohibited and restricted goods under customs laws.

- The Tribunal relied on the Supreme Court’s decision in Commissioner of Customs v. M/s. Atul Automations Pvt. Ltd. [2019 (365) E.L.T. 465 (S.C.)] to differentiate between prohibited and restricted goods.

- The Tribunal emphasized the need for a fair adjudication process, considering the importer’s bona fide efforts to obtain the required license from the DGFT.

Issue:

Whether the customs authorities were correct in imposing redemption fine and ordering re-export of the imported titanium powder, which is a restricted item requiring a DGFT license for import.

Facts:

- M/s. Asok Sparklers Factory filed a Bill of Entry for clearance of goods, including titanium powder, which is a restricted item under the import policy.

- The importer did not submit a DGFT import license for the titanium powder at the time of clearance.

- The adjudicating authority ordered confiscation of the titanium powder under Section 111(d) of the Customs Act, 1962, and imposed redemption fine and penalty.

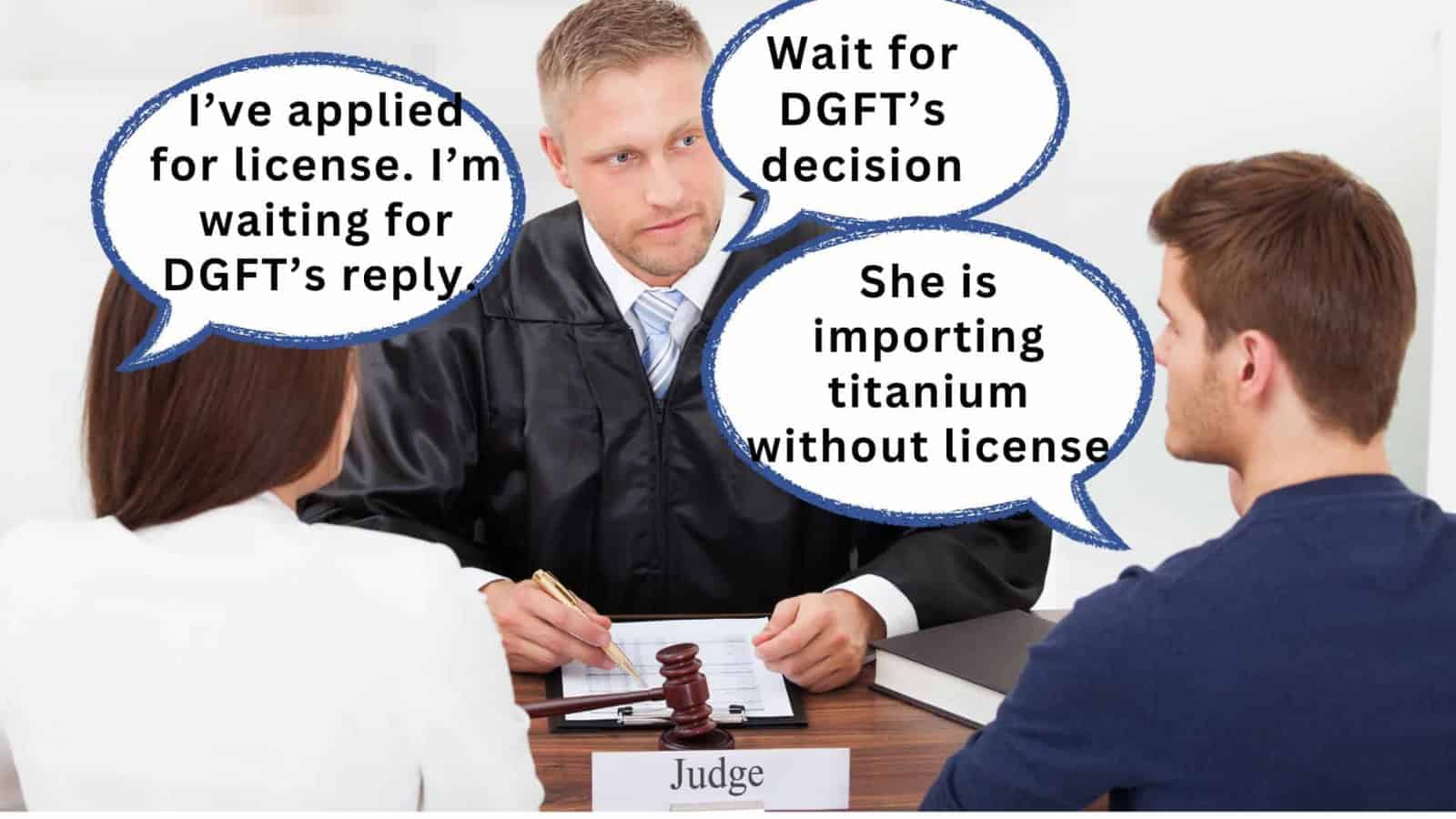

- The importer appealed against the order, stating that they had applied for a DGFT license, but the application was still pending.

Arguments:

- The importer argued that titanium powder is a restricted item, not a prohibited item, and the authorities erred in treating it as prohibited and ordering confiscation.

- The importer relied on the Supreme Court’s decision in Commissioner of Customs v. M/s. Atul Automations Pvt. Ltd. [2019 (365) E.L.T. 465 (S.C.)] and other CESTAT orders to distinguish between prohibited and restricted goods.

- The customs authorities contended that Section 3 of the Foreign Trade (Development and Regulation) Act requires a license for importing restricted items, failing which the import would be deemed prohibited.

Key Legal Precedents:

- Commissioner of Customs v. M/s. Atul Automations Pvt. Ltd. [2019 (365) E.L.T. 465 (S.C.)]

- Commissioner of Customs v. M/s. S.P. Associates & ors. [Final Order Nos. 41931 to 41971 of 2021 dated 27.08.2021 in Customs Appeal No. 40098 of 2021 & ors. – CESTAT, Chennai]

- M/s. Magal Engg. Tech Pvt. Ltd. v. Commissioner of Customs (Chennai-II) [Final Order No. 41039 of 2019 dated 09.09.2019 in Customs Appeal No. 40408 of 2019 – CESTAT, Chennai]

Judgment:

The CESTAT set aside the impugned order and remanded the matter back to the adjudicating authority. The adjudicating authority was directed to await the DGFT’s response/order on the importer’s application for an import authorization of the restricted item (titanium powder).

After receiving the DGFT’s decision, the adjudicating authority was instructed to pass a fresh speaking order, affording reasonable opportunities of being heard to the importer and considering the Supreme Court’s decision in M/s. Atul Automations Pvt. Ltd. case.

FAQs:

Q1: What is the significance of the Supreme Court’s decision in M/s. Atul Automations Pvt. Ltd. case?

A1: The Supreme Court’s decision in this case clarified the distinction between prohibited goods and restricted goods under customs laws. This precedent was crucial in the present case, as the Tribunal relied on it to differentiate between the treatment of prohibited and restricted goods.

Q2: Why did the Tribunal remand the case back to the adjudicating authority

A2: The Tribunal remanded the case because the importer had applied for a DGFT license, but the application was still pending. The Tribunal felt that the interests of justice demanded that the adjudicating authority await the DGFT’s decision on the license application before passing a fresh order.

Q3: What should the adjudicating authority consider while passing the fresh order?

A3: The adjudicating authority should consider the Supreme Court’s decision in M/s. Atul Automations Pvt. Ltd. case, which distinguishes between prohibited and restricted goods. The authority should also afford reasonable opportunities of being heard to the importer before passing the fresh order.

Q4: What is the significance of the importer’s bona fide efforts to obtain the DGFT license?

A4: The Tribunal noted that the importer’s application for a DGFT license, though belated, showed their bona fide intentions. This factor played a role in the Tribunal’s decision to remand the case for fresh adjudication, considering the importer’s efforts to comply with the legal requirements.

This appeal is filed against the Order-in-Appeal No. Seaport C.Cus.II No. 463/2023 dated 03.07.2023 passed by the Commissioner of Customs (Appeals-II), Chennai.

2. Heard Smt. A. Aruna, Ld. Advocate for the appellant and it is her case that the appellant-importer had filed Bill-of-Entry No. 9045755 dated 10.06.2022 for clearance of the goods which are mentioned in ‘Table-A’ of the Order-in-Original dated 05.08.2022. Out of the seven items, “Titanium Powder” at Sl. No. 2 appeared to be a restricted item as per the import policy, requiring licence from the DGFT for clearance of the same for home consumption.

3. It is an undisputed fact that the appellant had not submitted any such DGFT import licence for import of the Titanium Powder, which was treated as sufficient reason by the adjudicating authority to hold the said goods liable for confiscation under Section 111(d) of the Customs Act, 1962.

4. It appears that upon being pointed out, the appellant vide its letter dated 03.08.2022 requested the Deputy Commissioner of Customs to release the remaining cargo except Titanium Powder, for which an application for licence had already been made by them to the DGFT.

5. The adjudicating authority vide Order-inOriginal dated 05.08.2022, however, has only observed that the appellant had waived the Show Cause Notice and has proceeded to hold that Titanium Powder being a restricted item requiring DGFT licence for import and the importer having not produced the DGFT licence, the said goods were liable for confiscation under Section 111(d) ibid., however, also gave an option for redemption under Section 125(1) ibid. to redeem the said goods for the limited purpose of re-export only upon the payment of redemption fine of Rs.15,000/-. He has also ordered imposition of penalty under Section 112(a)(i) ibid.

6. Feeling aggrieved, it appears that the appellant filed an appeal before the first appellate authority, but however, even the first appellate authority vide impugned Order-in-Appeal dated 03.07.2023 having held that there was no irregularity or illegality in the order passed by the original authority, thereby rejecting their appeal, the present appeal has been filed before this forum.

7.1 The Ld. Advocate would submit at the outset that Titanium Powder is only a restricted item, but not a prohibited item under the Customs Act and therefore, the authorities below have clearly erred in treating the same as a prohibited item thereby ordering confiscation of the same.

7.2 She would also contend that the appellant, as pointed out in their letter dated 03.08.2022 before the adjudicating authority, had filed an application for import authorization of restricted item namely, Titanium Powder, vide application dated 12.07.2022, but the authority namely, DGFT, having not passed any order till date, no order as to confiscation should have been passed by the original authority.

7.3 She would also rely on a decision of the Hon’ble Apex Court in the case of Commissioner of Customs v. M/s. Atul Automations Pvt. Ltd. [2019 (365) E.L.T. 465 (S.C.)] wherein the Hon’ble Apex Court has clearly distinguished between prohibited goods and restricted goods after referring to the provisions of the Foreign Trade Act and Section 125 of the Customs Act. She would also place reliance on orders of the Chennai Bench of the Tribunal in the cases of Commissioner of Customs v. M/s. S.P. Associates & ors. [Final Order Nos. 41931 to 41971 of 2021 dated 27.08.2021 in Customs Appeal No. 40098 of 2021 & ors. – CESTAT, Chennai] and M/s. Magal Engg. Tech Pvt. Ltd. v. Commissioner of Customs (Chennai-II) [Final Order No. 41039 of 2019 dated 09.09.2019 in Customs Appeal No. 40408 of 2019 – CESTAT, Chennai] in support of her case.

8.1 Per contra, Shri M. Ambe, Ld. Deputy Commissioner, defended the orders of lower authorities. He would also submit that Section 3 of the Foreign Trade (Development and Regulation) Act requires licence for import of any restricted item, failing which the import of the said item would be deemed to be prohibited.

8.2 He would further draw my attention to paragraph 11 of the impugned order of the first appellate authority wherein the first appellate authority has held that when goods categorized as ‘restricted’ requiring an import licence are imported without licence, they may be treated as prohibited.

9. Having heard the rival contentions, I find that the only issue to be decided is: whether the authorities below were correct in imposing redemption fine while ordering re-export of the imported Titanium Powder?

10.1 Facts are not in dispute. What the original authority has missed is the application addressed to the DGFT, though belatedly, which only shows the bona fides of the appellant. When pointed out as to the requirement of licence, the appellant appears to have immediately made an application and there are no disputes that the said application is still pending with the DGFT and no order has yet been made on the said application. Hence, I am of the prima facie view that the interests of justice would demand that the matter be remanded to the file of the adjudicating authority awaiting the response from the DGFT on the application made by the appellant and then, pass an appropriate speaking order based on any such communication from the DGFT on the application for import authorization of the restricted items made by the appellant.

10.2 Hence, I do not propose to pass any order on the merits or otherwise of the claims and counterclaims. I find that the issue, therefore, depends on the response from the DGFT on the application made by the appellant.

11. In view of the above, I set aside the impugned order and remand the matter back to the file of the adjudicating authority, who shall await the response / order on the application for import authorization of restricted items filed by the appellant and then pass a de novo speaking order upon receipt of the said order from the DGFT. It goes without saying that the authority shall afford reasonable opportunities of being heard to the appellant before passing any de novo order. The adjudicating authority shall also keep in mind the binding decision of the Hon’ble Supreme Court in the case of M/s. Atul Automations Pvt. Ltd. (supra) wherein a specific distinction has been made between prohibited goods and restricted goods. All the contentions are therefore left open.

12. The appeal is treated as allowed by way of remand.

(Order pronounced in the open court on 21.11.2023)

(P. DINESHA)

(MEMBER (JUDICIAL)

×