Full News

AO's Overreach in Revision Case Quashed: High Court Upholds Limits of Section 264 (of Income Tax Act, 1961)

AO's Overreach in Revision Case Quashed: High Court Upholds Limits of Section 264 (of Income Tax Act, 1961)

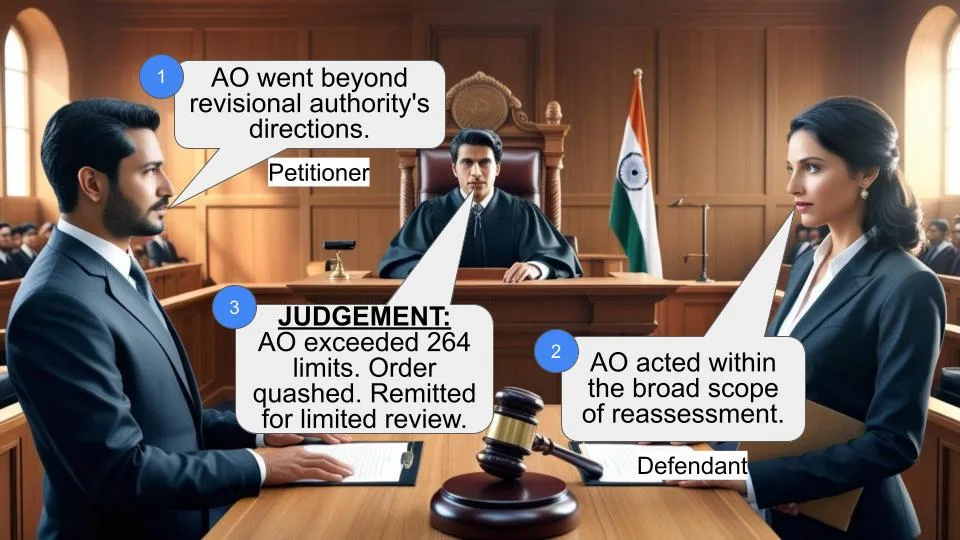

This case involves N. Seetharaman (the petitioner) challenging an order passed by the Assessing Officer (AO) following a revision under Section 264 (of Income Tax Act, 1961). The High Court ruled in favor of the petitioner, setting aside the AO's order and remitting the matter back for reconsideration within the limited scope of the revisional authority's directions.

Get the full picture - access the original judgement of the court order here

Case Name:

N. Seetharaman vs Commissioner of Income Tax (High Court of Madras)

W.P.No.12060 of 2004 W.P.M.P.No.14100 of 2004

Date: 29th November 2007

Key Takeaways:

1. The AO cannot exceed the scope of directions given by the revisional authority under Section 264 (of Income Tax Act, 1961).

2. An order under Section 264 (of Income Tax Act, 1961) should not be prejudicial to the assessee.

3. Writ petitions are maintainable in cases of jurisdictional errors, despite alternative remedies.

Issue:

Can the Assessing Officer expand the scope of assessment beyond the specific directions given by the Commissioner of Income Tax in a revision order under Section 264 (of Income Tax Act, 1961)?

Facts:

- The petitioner is a small-scale jeweler in Madurai.

- On 18.11.1998, he was apprehended in Trivandrum with 781.3 grams of jewelry and Rs.40,800 cash.

- The Income Tax Department seized these assets under Section 132-A (of Income Tax Act, 1961).

- The AO made an initial assessment computing undisclosed income of Rs. 2,79,087.

- The petitioner filed a revision petition under Section 264 (of Income Tax Act, 1961) to the Commissioner of Income Tax.

- The Commissioner directed the AO to reexamine specific issues raised by the petitioner.

- In the reassessment, the AO increased the total income to Rs. 6,55,540.

Arguments:

Petitioner:

- The AO exceeded his jurisdiction by considering issues not part of the original assessment.

- The revisional order under Section 264 (of Income Tax Act, 1961) cannot be prejudicial to the assessee.

Revenue:

- The scope of revision under the Income Tax Act is wide and not restricted.

- The AO can redo the assessment afresh, considering all materials.

Key Legal Precedents:

1. CIT v. D.N. Dosani (2006 ITR 275): AO has no jurisdiction to substitute the opinion of the Commissioner and expand the scope of assessment.

2. Fenner (India) Ltd. v. Dy. C.I.T. (241 I.T.R. 672 (of Income Tax Rules, 1962)): Jurisdictional errors can be corrected under Article 226 of the Constitution.

3. Whirlpool Corporation v. Registrar of Trade Marks, Mumbai (AIR 1999 SC 22): High Court's jurisdiction under Article 226 is not affected by alternative statutory remedies in cases of jurisdictional issues.

Judgement:

The High Court allowed the writ petition, setting aside the AO's order. It held that:

1. The AO clearly transgressed his powers beyond the scope of Section 264 (of Income Tax Act, 1961).

2. The revisional authority's directions were specific, and the AO couldn't expand them.

3. The matter was remitted back to the AO to confine himself to the limited questions addressed by the Revisional Authority.

FAQs:

1. Q: What is the significance of Section 264 (of Income Tax Act, 1961)?

A: Section 264 (of Income Tax Act, 1961) allows for revision of orders that are not prejudicial to the assessee. It's a safeguard against arbitrary assessments.

2. Q: Why did the court allow a writ petition despite alternative remedies?

A: The court held that in cases of jurisdictional errors, writ petitions are maintainable to correct such errors promptly.

3. Q: What are the limits of an Assessing Officer's power in reassessment?

A: The AO must confine themselves to the specific directions given by the revisional authority and cannot expand the scope of assessment on their own.

4. Q: How does this judgment impact future tax assessments?

A: It reinforces the principle that AOs must strictly adhere to the scope defined by higher authorities in revision orders, protecting assessees from arbitrary expansions of assessment.

5. Q: What should taxpayers do if they face similar situations?

A: If an AO exceeds the scope of a revisional order, taxpayers can consider filing a writ petition challenging the jurisdictional overreach, rather than just appealing through regular channels.

The petitioner has filed present Writ Petition to quash the File No.S-7028/Cir.II/Mdu for the Block Assessment years 1989-90 to 1999-2000 and consequently direct the respondent to restore the matter to the Assessing Officer with a direction to confine himself to the order under Section 264 (of Income Tax Act, 1961) of the Commissioner of Income Tax-I, Madurai.

2. Brief facts leading to the Writ Petition are as follows:

The petitioner is carrying on a small-scale business in making Gold jewellary out of old ornaments and the same is being sold in Trivandram. The making charges in the State of Kerala are comparatively higher than Madurai. His sons are also doing the same business and help him in his trade. They are assessed to income tax separately in Madurai. The petitioner is an assessee from the assessment year 1993-94 and presently assessed by the Assistant Commissioner of Income-Tax, Circle-II, Madurai. On 18.11.1998, when the petitioner was staying in a lodge in Trivandram, the local police apprehended him and found in his possession jewellery, weighing 781.3 grams and cash of Rs.40,800/-. On intimation by the police, the Director of Income Tax (Investigation), Cochin, gave a requisition under Section 132-A (of Income Tax Act, 1961), 1961 to the Police Department and the above said jewellary and cash were seized by the Income Tax Department. Pursuant to the notice under Section 158(B)(C) (of Income Tax Act, 1961), the petitioner filed a return of income in Form 2B on 25.08.1999, admitting a total income of Rs.6,000/- per month and requested that the tax payable be adjusted out of the seized cash.

3. The petitioner further submitted that being a small trader, he could not maintain any regular books of accounts. He further submitted that his sons are also petty traders and they do not maintain any accounts and they are filing their returns of income separately. It is the further case of the petitioner that based on the cash flow and the advise of his auditor, the petitioner voluntarily submitted his returns on 31.12.1997, for the assessment years 1993-94 and 1998-99, before action was taken under Section 132-A (of Income Tax Act, 1961) referred to above.

4. Referring to Section 158(B)(b) (of Income Tax Act, 1961), the petitioner has submitted that the income, which he had disclosed before the action under Section 132-A (of Income Tax Act, 1961), cannot fall within the definition of "undisclosed income". The Assessing Officer, rejecting the above said contention of the petitioner, by his order dated 31.03.2000, made an assessment computing the undisclosed income of Rs.2,79,087/-, including the income of his sons on the ground that no books of accounts were maintained by them. Aggrieved by the same, the petitioner has filed the Revision Petition on 26.03.2001 under Section 264 (of Income Tax Act, 1961) to the Commissioner of Income Tax-I, Madurai, by withdrawing the appeal so as to get the seized jewels. The Revisional Authority, by order dated 01.11.2002, found that the submissions of the petitioner were not appreciated in proper perspective by the Assessing Officer and therefore, with a view to re-examine the matter, directed the assessing Officer to adjudicate the matter afresh, after taking into account the assessee's version. Pursuant to the revisional order, the assessing officer went on to consider the other issues for the first time and completed the assessment on a higher total income of Rs.6,55,540/-. The above said order was received by the assessee/petitioner on 18.03.2004 and the same is challenged in this Writ Petition.

5. Mr.R.Srinivasan, learned counsel for the petitioner submitted that the revisional powers under Section 264 (of Income Tax Act, 1961) clearly provide that the Commissioner can pass such order, not being prejudicial to the assessee and when the Commissioner himself is prohibited by passing an order prejudicial to the assessee under Section 264 (of Income Tax Act, 1961), the assessing officer has exceeded in its jurisdiction by considering certain issues in the remand proceedings, which were not the subject matter of the original assessment order and therefore, the assessment order is per se illegal and liable to be set aside. He further submitted that the revisional order itself, having been passed after the limitation prescribed under Section 264 (of Income Tax Act, 1961), the consequential order of the assessing officer, enhancing the total income, prejudicial to the assessee, is patently without jurisdiction and therefore, the order needs correction in exercise of the powers under Article 226 of the Constitution of India.

6. On the issue of scope and powers of the revisional authority under the Income Tax Act, learned counsel for the petitioner relied on a decision in CIT v. D.N.Dosani reported in 280 I.T.R 275 (Guj). To support his contention that the error of jurisdiction can be corrected under Article 226 of the Constitution of India, he cited decisions in Fenner (India) Ltd., v. Dy.C.I.T., reported in 241 I.T.R. 672 (of Income Tax Rules, 1962), and Whirlpool Corporation v. Registrar of Trade Marks, Mumbai reported in AIR 1999 SC 22.

7. On the other hand, Mr.S.Narayanasamy, learned counsel for the Revenue submitted that the scope of the revision under the Income Tax Act is wide open and it is not restricted and therefore, the assessing officer can re-do the assessment afresh, taking into consideration of the materials gathered during enquiry. He further submitted that as against the order of assessing officer, an alternative remedy of appeal is provided under the Statute before the Commissioner (Appeals) and therefore, the present Writ Petition is not maintainable in law.

8. Learned counsel for the respondent placed reliance on the decision in C.I.T. v. Geo Indus. & Insecticides Pvt. Ltd., (Mad) reported in 1998 I.T.R., 541, and submitted that the powers of the Income Tax Officer to make assessment is not confined or restricted to the directions given by the Commissioner of Income Tax and it is open to the Assessing Officer to examine the matter afresh for the purpose of proper assessment of income.

9. Heard both sides.

10. On consideration of the materials and the returns submitted by the petitioner and his sons, the assessing officer by his order dated 31.03.2000, estimated an "undisclosed income" for the block period between 1989-90 to 1999-2000. The submissions of the assessee before the Revisional Authority are extracted hereunder:

"The Income Tax Practitioner mentioned that the subject matter of block assessment was addition of the value of gold jewellery weighing 781.340 grams and cash of Rs.40,800/- both requisitioned under Section 132 (of Income Tax Act, 1961) A from the Police Authorities. The Act defines in Section 158B(b) (of Income Tax Act, 1961) that "undisclosed income" includes any money, bullion, jewellery or other valuable articles or thing or any income based on any entry in the books of account or other documents or transactions, where such money, bullion, jewellery, valuable article, thing, entry in the books of accounts or other document or transaction represents wholly or partly income or property which has not been or would not have been disclosed for the purposes of this Act. The manner in which the undisclosed income has to be computed has been provided in Section 158B(b) (of Income Tax Act, 1961). Section 132A (of Income Tax Act, 1961) contains provisions relating to powers to requisition books of accounts etc. The authority conferred by Section 132 (of Income Tax Act, 1961) A of the Act can be exercised only when the specified authority, in consequence of the information in his possession, has reason to believe that the circumstances enumerated in Clauses (a) or (b) or ) of sub-section 1 (of Income Tax Act, 1961) of Section 132A (of Income Tax Act, 1961) exist. The authority can be exercised only under circumstances where 'any assets either wholly or partly income or property which has not been or would not have been, disclosed for the purposes of the Indian Income Tax Act from any person from whose possession or control such assets have been taken into custody by any officer or authority under any other law for the time being in force' (Clause ) of Section 132A (of Income Tax Act, 1961). The applicant submits that none of this conditions (a) to (c) existed in applicant's case. Since, the applicant did not possess any money, bullion, jewellary or other valuable article or thing which could represent any undisclosed income or property, it was impossible that the authorised officer would have 'reason to believe' to act for the purposes of authorising proceedings U/s.132A (of Income Tax Act, 1961). It is clear from the proceedings conducted during the course of seizure that the authorised officer, while examining on oath U/s.132(4) (of Income Tax Act, 1961) had not recorded any information to the effect the assets seized represented undisclosed income. The block assessment order also clearly indicates that the seized assets did not represent undisclosed income of the applicant. Hence, the proceedings initiated by issue of notice U/s.158B(c) (of Income Tax Act, 1961) ought to have been dropped by the AC as there was no case for the department to make assessment. There can be no inference of income for the purpose of block assessment, if the evidence relating to them is not found during such. The other additions can be made only in regular assessment and the pretext of the Block Assessment cannot lead to inclusion of the income, which was not discovered during search,"

11. The Revisional Authority, in his order dated 01.11.2002, observed that the above mentioned issues raised by the assessee were not examined by the assessing officer during the block assessment proceedings and that the assessing officer was guided by the presumption that since the assessee had not maintained books of accounts and furnished only cash flow statement, the assets seized viz., jewellery weighing 781.340 grams and cash of Rs.40,800/- were not disclosed. The Revisional Authority has further observed that the assessing officer did not examine the assessee's repeated statement that the above said assets belonged to the petitioner's family and they form part of the stock in trade of the assessee's family business. With the above specific issues, the Revisional Authority directed the Assessing Officer to adjudicate the matter afresh, after taking into account the assesse's version and giving him an opportunity of being heard before deciding the issue.

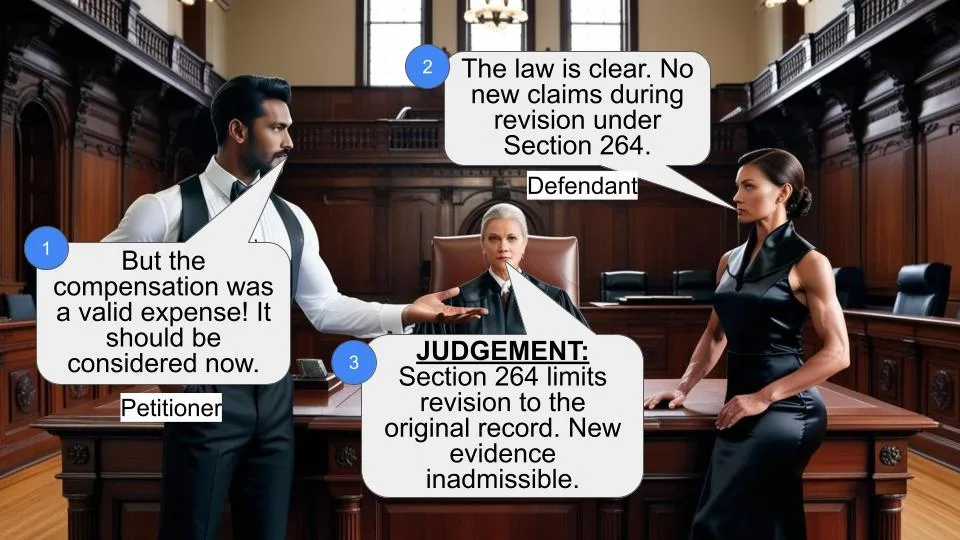

12. When the directions of the Revisional Authority are specific, the Assessing officer proceeded on the footing that the directions of the Revisional Authority to consider the issue afresh would mean that all the issues emanating from the information collected by him, have to be considered as a whole in order to arrive at a total undisclosed income, assessable for the block period. He further proceeded on the footing that even though all the materials were available with him, certain source of income was lost sight of in computation of the total undisclosed income and therefore, examined the assessment afresh for the block assessment period and arrived at a total undisclosed income at Rs.2,79,087/-.

13. The relevant Sections 263 and 264 of the Income Tax Act dealing with revisional powers of the Commissioner of Income Tax are extracted for adjudication of the issue as to whether the assessing officer is empowered to pass an order prejudicial to the interest of the assessee, in a proceeding emanating under revisional jurisdiction of the Commissioner of Income Tax under Section 264 (of Income Tax Act, 1961).

"263. Revision of orders prejudicial to Revenue:- (1) The Commissioner may call for and examine the records of any proceeding under this Act, and if he considers that any order passed therein by the Assessing Officer is erroneous in so far as it is prejudicial to the interests of the Revenue, he may, after giving the assessee an opportunity of being heard and after making or causing to be made such inquiry as he deems necessary, pass such order thereon as the circumstances of the case justify, including an order enhancing or modifying the assessment, or cancelling the assessment and directing a fresh assessment."

"264. Revision of other orders:- (1) In the case of any order other than an order to which Section 263 (of Income Tax Act, 1961) applies passed by an authority subordinate to him, the commissioner may, either of his own motion or on an application by the assessee for revision, call for the record of any proceeding under this Act in which any such order has been passed and may make such inquiry or cause such inquiry to be made and, subject to the provisions of this Act, may pass such order thereon, not being an order prejudical to the assessee, as he thinks fit.

(2) The commissioner shall not of his own motion revise any order under this Section if the order has been made more than one year previsously.

(3) In the case of an application for revision under this section by the assessee, the application must be made within one year from the date on which the order in question was communicated to him or the date on which he otherwise came to know of it, whichever is earlier:

Provided that the Commissioner may, if he is satisfied that the assessee was prevented by sufficient cause from making the application within that period, admit an application made after the expiry of that period.

(4) The Commissioner shall not revise any order under this section in the following cases-

(a) where an appeal against the order lies to the Deputy Commissioner (Appeals) or to the Commissioner (Appeals or to the Appellate Tribunal but has not been and the time within which such appeal may be made has not expired, or, in the case of an appeal to the Commissioner (Appeals) or to the Appellate Tribunal, the assessee has not waived his right of appeal; or

(b) where the order is pending on an appeal before the Deputy Commissioner (Appeals); or

(c) where the order has been made the subject of an appeal to the Commissioner (Appeals) or to the Appellate Tribunal.

(5) Every application by an assessee for revision under this section shall be accompanied by a fee of twenty-five rupees."

14. In Commissioner of Income Tax v. D.N.Dosani reported in 2006 ITR 275, a Division Bench of the Gujarat High Court, while considering the scope and power of the Assessing officer, held that the assessing Officer has no jurisdiction to substitute the opinion of the Commissioner and expand the scope of assessment, while answering the reference, the Division Bench held as follows:

"9. A bare perusal of the aforesaid provision makes it clear that, before the CIT can pass any order, he has to give the assessee an opportunity of being heard and thereafter record, at least prima facie, that the order made by the assessing officer is erroneous insofar as it is prejudicial to the interests of the revenue. The requirement of giving the assessee an opportunity of hearing is, for the simple reason that the assessee may be able to refute the belief of the CIT, which might have been formed on examination of the record of any proceeding under the Act, that is to say, assessee may be in a position to point out that the assessment order is neither erroneous nor prejudicial to the interests of the revenue, or even if it is erroneous, it is not prejudicial to the interests of the revenue, or it may not be erroneous, even if it is prejudicial to the interests of the revenue. Therefore, the moment the revenue's contention is accepted that in the fresh assessment, the assessing officer is entitled to examine items which did not form part of Section 263 (of Income Tax Act, 1961) proceedings, the statutory requirement of framing an order under Section 263 (of Income Tax Act, 1961) after giving the assessee an opportunity of being heard, stands obliterated or is made redundant. This interpretation goes against clear unambiguous language in which the section is couched.

10. The provision also requires the CIT to record that an order passed by the assessing officer is erroneous and prejudicial to the interests of the revenue. The satisfaction of these two pre-requisite conditions is a must before assumption of the jurisdiction under Section 263 (of Income Tax Act, 1961). This legal position is well established and bears no repetition. Hence, the CIT can exercise jurisdiction only after establishing on record that the assessment order is erroneous and prejudicial to the interests of the revenue and for this purpose, he has to show from the record as to what portion of the assessment order is erroneous and prejudicial to the interests of the revenue. In a given case, the entire order may be erroneous and prejudicial to the interests of the revenue, but the record of Section 263 (of Income Tax Act, 1961) proceedings must reflect that. In the instant case, and it is not disputed, the CIT has issued show cause notice only on two grounds, and those are the only grounds processed by the CIT while framing the order under Section 263 (of Income Tax Act, 1961). The operative portion of the order, therefore, cannot be read, as submitted by the revenue de hors the contents of the show cause notice and the order.

11. Considering the issue from a slightly different angle. The assessee was called upon by CIT to tender explanation qua two items mentioned in the show cause notice. On a plain reading of Section 263(1) (of Income Tax Act, 1961), it is apparent that the CIT could not have treated any further item or part of the assessment order as being erroneous and prejudicial to the interests of the revenue without giving the assessee an opportunity of being heard. Therefore, what the CIT himself could not have done, cannot be permitted to be done by the assessing officer while giving effect to the order under Section 263 (of Income Tax Act, 1961). It is necessary to bear in mind that powers of revision can be exercised only by the CIT and therefore, the assessing officer cannot, under the guise of framing fresh assessment, exercise the said powers in relation to other items forming part of the assessment record. The provision which permits exercise of jurisdiction under Section 263 (of Income Tax Act, 1961) in the first instance requires the CIT to call for and examine the record of any proceeding under the Act. The logical presumption is, therefore, that before issuance of show cause notice under Section 263 (of Income Tax Act, 1961), the CIT has examined the record, and found prima facie that the assessment order is erroneous and prejudicial to the interests of the revenue only in relation to the items mentioned in the show cause notice. For the assessing officer, to substitute his opinion in place of the opinion of CIT is not envisaged by the provision and therefore also, action of the assessing officer in expanding scope of consequential assessments cannot be upheld.

12. The Scheme of the Act has provided different powers to different authorities and these are required to be exercised after satisfying the pre-requisite conditions and jurisdictional facts. The assessing officer can disturb / re-open a finalized assessment by invoking his powers either under Section 154 (of Income Tax Act, 1961) or under Section 147 (of Income Tax Act, 1961), provided he can show that the necessary requirements are fulfilled. If, what revenue contends today, is accepted, these and other such provisions which empower different authorities to exercise jurisdiction at different point of time in distinct settings would be rendered otiose and that can never be the legislative intent. It is almost akin to providing separate keys for separate locked doors and the person wanting to open a particular door is required to apply the correct key which matches the concerned lock. Therefore, in proceedings, to give effect to order under Section 263 (of Income Tax Act, 1961), the assessing officer cannot be permitted to undertake an exercise not warranted by the legislative scheme."

15. In Commissioner of Income Tax v. GEO Industries and Insecticides (I) Pvt. Ltd., reported in 234 ITR 541, the Commissioner of Income Tax initiated suo-moto revision proceedings under Section 263 (of Income Tax Act, 1961) on the ground that the losses of the cashew department and the losses of the hessian department could not be set off against the profits of the insecticides department for and from the assessment year 1974-75. The Income-tax Officer thereafter made a fresh assessment under Section 143 (of Income Tax Act, 1961) in pursuance of the directions of the Commissioner and accepted the claim of the assessee that even ignoring the cashew department loss, there was available loss in the pesticides department to be set off against the net profit. However, the assessee made a claim for deduction of Rs.79,000/- being damages paid which was disallowed for the assessment year 1976-77 on the ground that it did not represent the loss of that year but relate to the assessment year prior to 1976-77. The Income-tax Officer rejected the claim of the assessee on the ground that the Commissioner of Income-tax in the revisional order set aside the order of assessment only for a specific purpose of excluding the loss from the cashew department and it was not open to the assessee to make a claim for the deduction of Rs.79,000/- in the fresh assessment made on the basis of the directions of the Commissioner of Income-tax. On appeal, the Commissioner of Income-tax (Appeals) held that there was nothing in law preventing the Income-tax Office from going through the question of set off of Rs.79,000/- and hence directed the Income-tax Officer to examine the matter on merits for allowance of the damages paid. On further appeal, the Tribunal held that when the Income-tax Officer makes a fresh assessment, he has all the powers at the time of making assessment in terms of Section 143(3) (of Income Tax Act, 1961) and the Commissioner of Income-tax (Appeal) was justified in directing the Income-tax Officer to consider the claim of the assessee for deduction of the sum of Rs.79,000/- in the fresh assessment made on the basis of the directions of the Commissioner of Income-tax.

16. In the above reported judgment, the Commissioner of Income Tax considered that the order passed by the assessing officer was erroneous in so far as it was prejudicial to the interest of the Revenue and directed the Income Tax officer to make fresh assessment in accordance with law so as to exclusde the losses of the Cashew department and of the hessian department (if any) after giving adequate opportunity to the assessee company. It was a case where the Revenue established on the basis of the record that the assessment order was erroneous and prejudicial to the interests of the Revenue and directed the Income Tax Officer to make a fresh assessment in accordance with law and the order in the revision reflected that the set off loss from the defunct cashewnut business against the profit of the business in the manufacture and sale of pesticides was erroneous. In the case on hand, it is not the case of the revenue before the revisional authority that the original assessment order was erroneous and prejudicial to the interests to the revenue nor there is any finding by the revisional authority to redo the entire exercise in that direction. Therefore, the decision relied on by the counsel for the revenue is not applicable to the facts of the present writ petition.

17. Perusal of the revisional order demonstrates that the revisional authority has directed the assessing officer to adjudicate specific issues, addressed and examined by the revisional authority. As rightly contended by the learned counsel for the petitioner, if the revisional authority had intended that the entire assessment has to be re done, then he would issued appropriate directions following the mandatory provision in Section 263 (of Income Tax Act, 1961). When the directions are precise, the assessing officer cannot expand the revisional order.

19. It is not in dispute that the Commissioner may in his exercise of his revisional power, modify or reverse the order in favour of the assessee. The revisional authority can also cancel the assessment order for a fresh assessment, but the order under this Section should not be prejudicial to the assessee. Therefore, when the Revisional Authority passes an order not being prejudicial to the assessee, the consequential duty that is cast on the assessing authority is to confine himself to the specific directions contained in the order. When an assessee is aggrieved by an order of the assessing officer and files a revision petition before the competent authority and if the resultant order under Section 264 (of Income Tax Act, 1961), made in the revision, puts the assesse in a position, worse than that in which he was placed before, it is clearly prejudicial to the assessee. When the revisional authority himself lacks the jurisdiction to reassess the proceedings and pass orders adverse to the interest of the assessee, the assessing officer, cannot exceed in his jurisdiction and redo the assessment afresh. When the powers of the revisional authority are limited under the scheme of the Act, the assessment made by the respondent, by assuming more powers than that of the revisional authority, is patently illegal and without jurisdiction. At best, the assessing officer could confine himself only to the limited extent of scrutiny of cash flow statement and valuation statement.

20. As regards the plea of alternative remedy, this Court in Fenner (India) Ltd., v. Dy.C.I.T., reported in 241 I.T.R. 672 (of Income Tax Rules, 1962), at page 682, held that,"As the error here is one of jurisdiction it is not necessary for the assessee to have recourse to the remedies by way of appeal, revision etc. It is well settled that when a jurisdictional error is brought to the notice of this court such errors are capable of being corrected by this Court in exercise of the Court's powers under article 226 of the Constitution of India. The Supreme Court in the case of CIT v. Progressive Engineering [1993] 200 ITR 231 (sic), held that when all the relevant facts were before the Court and the law is clear on the subject, it is the duty of the High Court to interfere. That was also a case where the proceedings were sought to be initiated against the assessee under Section 147 (of Income Tax Act, 1961)."

21. In Whirlpool Corporation v. Registrar of Trade Marks, Mumbai reported in AIR 1999 SC 22, the Supreme Court at Paragraphs 20 and 21, held as follows:

"20. Much water has since flown beneath the bridge, but there has been no corrosive effect on these decisions which, though old, continue to hold the field with the result that law as to be jurisdiction of the High Court in entertaining a writ petition under Article 226 of the Constitution. Inspite of the alternative statutory remedies, is not affected, specially in a case where the authority against whom the writ is filed is shown to have had no jurisdiction or had purported to usurp jurisdiction without any legal foundation.

21. That being so, the High Court was not justified in dismissing the Writ Petition at the initial stage without examining the contention that the show cause notice issued to the appellant was wholly without jurisdiction and that the Registar, in the circumstances of the case, was not justified in acting as the "TRIBUNAL"."

22. As the assessing officer has clearly transgressed his powers beyond the scope of Section 264 (of Income Tax Act, 1961), driving the petitioner to seek recourse to file an appeal before the Commissioner, is not justifiable in the interest of the justice. Therefore, the Writ Petition is maintainable in law.

23. In view of the above, the impugned order passed by the assessing officer is set aside and the matter is remitted back to the assessing officer to confine himself to the limited question addressed by the Revisional Authority and pass orders in accordance with law, after giving adequate opportunity to the assessee of being heard.

24. In the result, the Writ Petition is allowed. No costs. Consequently, connected Miscellaneous Petition is also closed.

29.11.2007

S. MANIKUMAR, J.

×

Similar Ripples

Questions

AO's Overreach in Revision Case Quashed: High Court Upholds Limits of Section 264 (of Income Tax Act, 1961)

Write your CommentSimilar Posts

Generic

- Reportdata/5124_.pdf