Assessee Wins: Court Upholds Section 54F (of Income Tax Act, 1961) Deduction El…

Full News

Assessee Wins: Court Upholds Section 54F (of Income Tax Act, 1961) Deduction Eligibility

Assessee Wins: Court Upholds Section 54F (of Income Tax Act, 1961) Deduction Eligibility

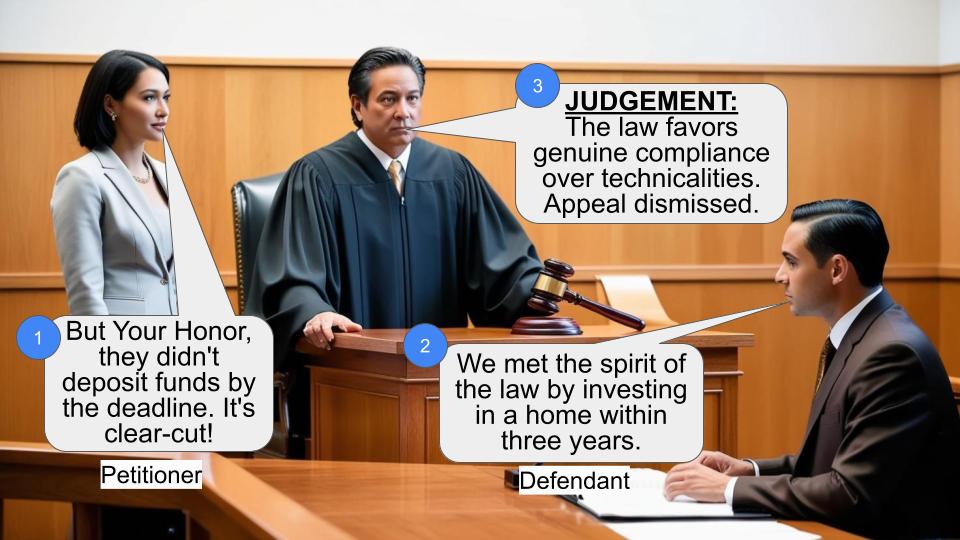

In the case of “Commissioner of Income Tax vs I. Ifthiqar Ashiq,” the High Court ruled in favor of the assessee, allowing a tax deduction under Section 54F (of Income Tax Act, 1961). The court found that the assessee met the necessary conditions for the deduction, despite the Revenue’s contention that the case fell under the proviso, which would disqualify the deduction.

Get the full picture - access the original judgement of the court order here

Case Name

Commissioner of Income Tax vs I. Ifthiqar Ashiq (High Court of Madras)

Tax Case Appeal No.54 of 2016

Date: 8th February 2016

Key Takeaways

- The court clarified the application of Section 54F (of Income Tax Act, 1961), emphasizing the conditions under which a taxpayer can claim a deduction for capital gains.

- The decision highlighted the importance of the assessee not owning more than one residential house, other than the new asset, at the time of the original asset’s transfer.

- The judgment reinforced that the proviso to Section 54F(1) (of Income Tax Act, 1961) cannot be applied independently of its main clause.

Issue

Does the assessee qualify for a deduction under Section 54F (of Income Tax Act, 1961), despite the Revenue’s claim that the case falls under the proviso, which would negate the deduction?

Facts

- The assessee sold a piece of land in Neelankarai and invested the proceeds in constructing a residential house in Kodaikanal.

- The assessee claimed a deduction under Section 54F (of Income Tax Act, 1961) for the capital gains from the sale.

- The Revenue argued that the assessee owned more than one residential property, which would disqualify him from the deduction under the proviso to Section 54F(1) (of Income Tax Act, 1961).

Arguments

- Assessee’s Argument: The assessee contended that he did not own more than one residential house, other than the new asset, at the time of the original asset’s transfer. Therefore, he met the conditions for the deduction under Section 54F (of Income Tax Act, 1961).

- Revenue’s Argument: The Revenue argued that the assessee’s case fell under the proviso to Section 54F(1) (of Income Tax Act, 1961), as he allegedly owned more than one residential property, thus disqualifying him from the deduction.

Key Legal Precedents

- Section 54F (of Income Tax Act, 1961): This section provides for a deduction on capital gains if the assessee invests in a new residential house, subject to certain conditions.

- Shambhu Investments Private Limited v. Commissioner of Income Tax: Cited by the Tribunal, this case was used to support the interpretation of “building” under Section 22 (of Income Tax Act, 1961).

Judgement

The court ruled in favor of the assessee, stating that he did not own more than one residential house, other than the new asset, at the time of the original asset’s transfer. Therefore, the conditions of Section 54F (of Income Tax Act, 1961) were satisfied, and the proviso did not apply. The court dismissed the Revenue’s appeal, allowing the deduction.

FAQs

Q: What is Section 54F (of Income Tax Act, 1961)?

A: Section 54F (of Income Tax Act, 1961) provides a tax deduction on capital gains if the proceeds are invested in a new residential house, subject to specific conditions.

Q: Why did the Revenue believe the deduction should not apply?

A: The Revenue argued that the assessee owned more than one residential property, which would trigger the proviso to Section 54F(1) (of Income Tax Act, 1961) and disqualify the deduction.

Q: What was the court’s reasoning for allowing the deduction?

A: The court found that the assessee did not own more than one residential house, other than the new asset, at the time of the original asset’s transfer, thus meeting the conditions for the deduction under Section 54F (of Income Tax Act, 1961).

The Revenue has come up with the above appeal, raising the following two substantial questions of law:-

"1. Whether on the facts and circumstances of the case, the Tribunal was right in allowing assessee claim for deduction u/s. 54F (of Income Tax Act, 1961) especially when assessee owned two properties on the date of transfer of original assets and income from two properties were chargeable to tax under the head income from house property?

2. Is not the finding of the Tribunal bad especially when the assessee case is hit by clauses (a)(1) and (b) of the proviso to Section 54F (of Income Tax Act, 1961) a d therefore no deduction can be granted u/s 54F (of Income Tax Act, 1961)?"

2. We have heard Mr.M.Swaminathan, learned Standing Counsel for the Department and Dr.Anita Sumanth, learned counsel appearing for the respondent/assessee.

3. The Respondent/Assessee filed his Return of Income on 4.11.2009 for the Assessment Year 2009-10. The case was selected for scrutiny and notice was issued.

4. It was found that the assessee made cash deposits of Rs.66,50,000/- at Indian Bank at various dates. When questioned, the assessee explained that the cash represented the sale proceeds of a land owned by him at Neelankarai. The total sale consideration was Rs.1,14,88,000/-. The assessee claimed that the entire sale consideration was invested in the construction of a residential house at Kodaikanal. Therefore, he claimed exemption under Section 54F (of Income Tax Act, 1961).

5. But the Assessing Officer held by his order dated 23.12.20911 that the case is covered by the proviso to Section 54F(1) (of Income Tax Act, 1961). This was on the basis of an opinion tendered by the Joint Commissioner under Section 144A (of Income Tax Act, 1961).

6. The assessee filed an appeal to the Commissioner of Income Tax (Appeals). The appeal was dismissed, forcing the assessee to file a further appeal before the Income Tax Appellate Tribunal. By an order dated 11.6.2013, the Tribunal allowed the appeal of the assessee on the ground that Section 22 (of Income Tax Act, 1961) uses only the expression "building", without qualifying it with an adjective "residential". The Tribunal in support of the said consideration, relied upon a decision of the Supreme Court in Shambhu Investments Private Limited v. Commissioner of Income Tax [(263) ITR 143 (SC). Therefore, the Revenue has come up with the above appeal.

7. The actual question of law that arises for consideration in the appeal is as to whether the case of the assessee is covered by the substantive part of sub-section (1) of Section 54F (of Income Tax Act, 1961) or the proviso thereunder.

8. If the case of the assessee comes within the substantive part of Section 54F(1) (of Income Tax Act, 1961), he is entitled to the deduction. If the case is covered by the proviso to Section 54F (of Income Tax Act, 1961), the assessee is not entitled to the benefit of the substantive part of sub-section (1) of Section 54F (of Income Tax Act, 1961).

9. Under the substantive part of Section 54F(1) (of Income Tax Act, 1961), the capital gain arising from the transfer of any long term capital asset, not being a residential house, shall not be subjected to the taxation provisions, if the assessee had within the period of one year before or two years after the date on which the transfer took place, purchased a residential house. Alternatively he should have constructed one residential house in India within a period of three years. If these conditions are satisfied, the capital gain will be dealt with in accordance with Clauses (a) and (b) of sub-section (1) of Section 54F (of Income Tax Act, 1961).

10. There is no dispute about the fact that the assessee in this case made a transfer of a long term capital asset it which not a residential house.

There is no dispute about the fact that there was capital gain arising from the transaction. There is also no dispute about the fact that within a period of two years after the date on which the sale of Neelankarai property took place, the assessee purchased a residential house in Kodaikanal. Therefore, all the three conditions stipulated in sub-section (1) of Section 54F (of Income Tax Act, 1961), is satisfied in the case on hand.

11. But according to the Revenue, the case of the assessee would fall within the proviso to Section 54F (of Income Tax Act, 1961) and hence the benefit is not available to him. To appreciate the reach of the said contention, it is necessary to extract proviso to Section 54F(1) (of Income Tax Act, 1961), it reads as follows:-

"54F. (1) [Subject to the provisions of sub- section (4), where, in the case of an assessee being an individual or a Hindu undivided family], the capital gain arises from the transfer of any long-term capital asset, not being a residential house (hereafter in this section referred to as the original asset), and the assessee has, within a period of one year before or 89[two years] after the date on which the transfer took place purchased, or has within a period of three years after that date constructed, a residential house (hereafter in this section referred to as the new asset), the capital gain shall be dealt with in accordance with the following provisions of this section, that is to say,—

(a) if the cost of the new asset is not less than the net consideration in respect of the original asset, the whole of such capital gain shall not be charged under section 45 (of Income Tax Act, 1961) ;

(b) if the cost of the new asset is less than the net consideration in respect of the original asset, so much of the capital gain as bears to the whole of the capital gain the same proportion as the cost of the new asset bears to the net consideration, shall not be charged under section 45 (of Income Tax Act, 1961):

[Provided that nothing contained in this sub- section shall apply where—

(a) the assessee,—

(i) owns more than one residential house, other than the new asset, on the date of transfer of the original asset; or

(ii) purchases any residential house, other than the new asset, within a period of one year after the date of transfer of the original asset; or

(iii) constructs any residential house, other than the new asset, within a period of three years after the date of transfer of the original asset; and

(b) the income from such residential house, other than the one residential house owned on the date of transfer of the original asset, is chargeable under the head “Income from house property”.]

Explanation.—For the purposes of this section,—

“net consideration”, in relation to the transfer of a capital asset, means the full value of the consideration received or accruing as a result of the transfer of the capital asset as reduced by any expenditure incurred wholly and exclusively in connection with such transfer."

12. A careful look at the proviso to Section 54F(1) (of Income Tax Act, 1961) would show that clause (a) of the proviso gives three alternatives. But clause (a) and clause(b) are intertwine with the use of a conjunction "and".

13. In other words, to attract the proviso under Section 54F(1) (of Income Tax Act, 1961), the conditions stipulated in clause (a)(i) together with clause (b) should be satisfied. Alternatively the contingency stipulated in clause (a)(ii) together with clause (b) should be satisfied or at least the contingency stipulated in clause (a)(iii) together with clause (b) should be satisfied.

14. It is not a case of the Department that the case of the assessee would fall under any one of the three sub-clauses of clause (a) together with clause (b). The case of the Department is that the assessee had income from a commercial property that was treated as income from house property. To be precise, the assessee had one residential house in Chennai, one commercial flat in Chennai, from out of both of which, he was deriving a total income of Rs.4,25,131/-. He also had a land in Neelankarai which was sold and a house property was purchased in Kodaikanal.

15. Under Section 22 (of Income Tax Act, 1961), any income from any buildings, irrespective of which the use which has to be treated under the head "income from house property". Therefore, the Revenue cannot take above all the terminology use in clause (b) under the proviso. This is a mistake into which the Revenue has fallen to treat the case of the assessee as falling within the purview of the proviso.

16. The facts of the case as narrated in the order of assessment would show that the assessee did not own more than one residential house other than the new asset on the date of transfer of the original asset so as to fall clause (a)(i) of the proviso. The assessee did not purchase any residential house other than the new asset within one year of the transfer of the original asset. Therefore, his case did not also fall within clause (a)(ii) of the proviso.

The assessee did not construct any residential house other than the new asset, so as to fall under clause (a)(iii). Therefore, the assessee did not satisfy any of the three sub-clauses contained in clause (a). Hence, the question of applying clause (b) of the proviso independent of the clause (a) of the proviso did not arise.

17. In view of the above, the substantial question of law is answered in favour of the assessee. Accordingly, the appeal is dismissed.

18. Before parting with, we should record that the Tribunal has wrongly indicated the address of the respondent/assessee as that of his counsel. Since the counsel does not want to take care the Original Order of Assessment and the order of the Appellate Authority contained the correct address of the assessee. Therefore, while issuing a certified copy of the order, the Registry shall indicate the correct address of the assessee as shown in the Original Order of Assessment without showing the address of the counsel for the assessee.

(V.R.S., J) (N.K.K., J)

08.02.2016

Index : Yes or No

Internet : Yes or No

To

Income tax Appellate Tribunal, Madras 'C' Bench, Chennai.

V.RAMASUBRAMANIAN, J

AND

N.KIRUBAKARAN, J

×

Questions

Assessee Wins: Court Upholds Section 54F (of Income Tax Act, 1961) Deduction Eligibility

Write your CommentSimilar Posts

Generic

- Reportdata/3117.pdf