Assessee Wins: No Evidence of Unexplained Investment in Lamborghini

Full News

COMMISSIONER OF INCOME TAX VS PROVESTMENT SECURITIES PVT. LTD.-(High Court)

Assessee Wins: No Evidence of Unexplained Investment in Lamborghini

Assessee Wins: No Evidence of Unexplained Investment in Lamborghini

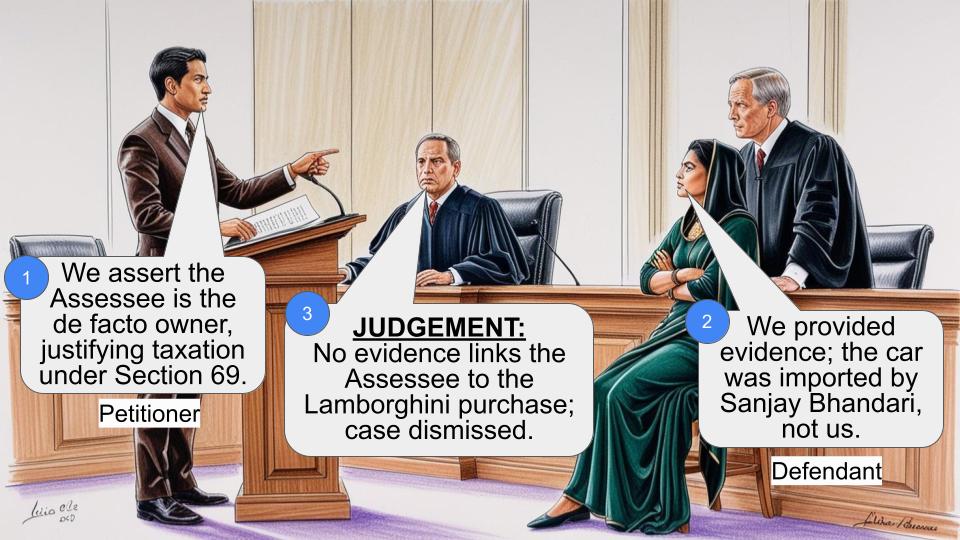

This case involves a dispute over whether an Assessee made an unexplained investment in a Lamborghini car. The Revenue claimed the Assessee was the de facto owner and sought to tax the vehicle’s value as an unexplained investment under Section 69 of the Income Tax Act, 1961. However, the court found no evidence linking the Assessee to the purchase, ruling in favor of the Assessee and against the Revenue.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs. Provestment Securities Pvt. Ltd. (High Court of Delhi)

ITA 86/2013

Date: 30th November 2015

Key Takeaways:

- The court emphasized the importance of evidence in establishing ownership and investment.

- The decision highlights the necessity for the Revenue to provide concrete evidence before making additions under Section 69.

- The ruling reinforces the principle that ownership cannot be presumed without clear evidence.

Issue:

Did the Assessee make an unexplained investment in the Lamborghini car, warranting taxation under Section 69 of the Income Tax Act, 1961?

Facts:

- The Assessee was accused of owning a Lamborghini used by Mr. Sameer Thapar, a major shareholder.

- The vehicle was imported by Mr. Sanjay Bhandari and registered under VKTT, a proprietorship of Bhandari.

- The Assessee paid duties and penalties for the car but claimed it was only for trial purposes.

- The Revenue argued the Assessee was the de facto owner, while the Assessee denied making any investment in the car.

Arguments:

- Revenue: Claimed the Assessee was the de facto owner and sought to tax the car’s value as unexplained investment.

- Assessee: Argued they did not own the car, provided evidence of the vehicle’s purchase by Sanjay Bhandari, and claimed payments were made for trial purposes only.

Key Legal Precedents:

- Section 69 of the Income Tax Act, 1961: This section allows for taxation of unexplained investments. The court emphasized that for this section to apply, it must be established that an investment was made and not recorded in the books.

Judgement:

The court ruled in favor of the Assessee, stating that there was no evidence to prove the Assessee made an investment in the car. The court found the Revenue’s claims unsubstantiated and dismissed the appeal, affirming the Tribunal’s decision.

FAQs:

Q1. Why was the Assessee not taxed for the car?

A1. The court found no evidence linking the Assessee to the purchase of the car, thus no unexplained investment was established.

Q2. What does this mean for similar cases?

A2. This case sets a precedent that ownership and investment must be clearly evidenced before applying Section 69.

Q3. What was the role of Sanjay Bhandari in this case?

A3. Sanjay Bhandari was the original importer of the car, and the Assessee provided evidence that Bhandari’s entities handled the purchase and registration.

Q4. Why did the Assessee pay duties if they didn’t own the car?

A4. The Assessee claimed the payments were made for trial purposes and not as an indication of ownership.

1. The Revenue has filed the present appeal under Section 260A of the

Income Tax Act, 1961 (hereafter ‘the Act’) calling into question an order dated 13th July, 2012 passed by the Income Tax Appellate Tribunal

(hereafter ‘the Tribunal’) in ITA No. 2485/Del/2010. The said appeal was

filed by the Assessee challenging an order dated 31st March, 2010 passed

by the Commissioner Income Tax (Appeals) [hereafter ‘CIT(A)’)] in

Appeal no. 153/CIT(A) (xvii)/ Del/ 08-09 whereby the appeal filed by the

Assessee against the assessment order dated 15th December, 2008 passed by the Assessing Officer (hereafter ‘the AO’) for the assessment year 2006-07, was rejected.

2. The principal controversy in the present case involves a Lamborghini

Car bearing registration no. PB-09G-0052, which had been exclusively

used by one Mr Sameer Thapar who is a major shareholder of the Assessee

Company in his capacity as a Karta of Sameer Thapar & Sons (HUF).

Whilst the Assessee Company has paid the import duty, penalty and fine

for the aforesaid motor vehicle and has also capitalized the said asset in its books in a later year, the Assessee has claimed that it has not paid any consideration towards the cost of the car. Neither the AO nor the CIT(A) accepted the explanations offered by the Assessee for being in possession of the vehicle and, in effect, concluded that the Assessee was de facto owner of the vehicle in question. Accordingly, the value of the vehicle was sought to be taxed as unexplained investment under Section 69 of the Act.

The Tribunal, however, accepted the contention of the Assessee and held

that the Assessee was not the owner of the vehicle in question within the scope of “ownership” as defined under Section 2(30) of the Motor Vehicles Act, 1988; the Assessee was not registered as a owner with the concerned authorities under the said Act. The Tribunal held that there was no material which indicated that the Assessee had paid for the car or that the purchase transaction was a benami transaction. The Tribunal, thus, allowed the Assessee’s appeal, which is impugned by the Revenue.

3. By an order dated 2nd July, 2013 this Court framed the following

questions of law:-

“1. Whether the Income Tax Appellate Tribunal has

rightly interpreted Section 69 of the Income Tax Act, 1961 and

was right in deleting the addition of Rs.1,37,07,306/ made by

the assessing officer on account of undisclosed investment in

Lamorghini Car?

2. Whether the order of the Income Tax Appellate

Tribunal is not perverse in the facts and circumstances of the

case?”

4. The relevant facts necessary to address the aforesaid controversy are

briefly stated as under:-

4.1 The Assessee is a promoter of a public company – JCT Ltd.

(hereafter referred as ‘JCT’) which belongs to the Thapar Group. Mr

Sameer Thapar is the Vice-chairman-cum-Managing Director of JCT Ltd.

He is also the Karta of Sameer Thapar & Sons (HUF), which is stated to

own 99% of the shareholding of the Assessee. The Department of Revenue

Intelligence (Customs Department) (hereafter referred as ‘DRI) conducted

search and seizure operations on the premises of one Mr Sanjay Bhandari in the month of September 2005, in connection with the import of motor

vehicles under the EPCG Scheme at a concessional rate of duty.

4.2 Pursuant to the search, notices were issued by the DRI for production of the vehicle in question, which was in possession of Mr Sameer Thapar.

The vehicle in question was produced before the DRI on 10th September,

2005 and was seized by the DRI on that date for alleged violation of duty payment.

4.3 The vehicle in question had been imported in India by Mr Sanjay

Bhandari in the name of his sole proprietorship concern. According to the Assessee, the said vehicle was purchased by Mr Sanjay Bhandari,

proprietor of M/s History Logistics (a proprietorship concern of Mr Sanjay Bhandari). It is claimed that, thereafter, the said vehicle was sold to another proprietorship concern of Mr Sanjay Bhandari - M/s V.K. Tours & Travels (hereafter ‘VKTT’) through a High Sea Sale Agreement and

Contract executed on 4th April 2005. Although the Revenue had also raised a question whether a sale between two proprietorship concerns could take place, however, the same is not material inasmuch as it is not disputed that the vehicle in question came to be registered in the name of VKTT, which at the material time was a sole proprietorship concern of Mr Sanjay Bhandari.

4.4 On the basis of information received from the Assistant Director of

Income Tax regarding the vehicle in question, a show cause notice was

issued by the AO to the Assessee on 19th November, 2008 requiring the

Assessee to explain the source of the investment of the vehicle in question.

In response to the show cause notice, the Assessee filed a letter dated 22nd November, 2008. The Assessee explained that VKTT had approached the

Assessee for taking the vehicle on lease and had handed over the possession of the vehicle for trial. While the vehicle was still on trial, the same was seized by the DRI. Subsequently, the vehicle was released to the Assessee on the payment of differential duty, execution of bond and submission of bank guarantee for fine and penalty. Since no consideration was shown to have been paid for the original cost of the vehicle, the AO was not convinced of the explanation offered as to the rights being exercised by the Assessee in respect of the vehicle in question.

4.5 Accordingly, the AO held that the Assessee’s investment in

purchasing the vehicle was liable to be taxed in its hands, as unexplained investment.

4.6 The Assessee preferred an appeal against the assessment order before

the CIT(A).

4.7 Before the CIT(A), the Assessee sought to produce further

documents and filed an application under Rule 46A for production of

additional evidence, which included an invoice in favour of M/s History

Logistics; copy of the letter of credit issued by the Oriental Bank of

Commerce; copy of the bank advice dated 15th April, 2005 for remittance

of Rs.70,89,972/-; marine insurance policies; invoice dated 31st March,

2005 for the sale of car by M/s History Logistics to VKTT; a copy of

challans/invoice for payment of insurance premium of Rs.2,96,793/, custom duty for Rs.4,89,968/-, commission for Rs.42,978/- and other charges for Rs.88,945 paid by VKTT; and confirmation from Mr Sanjay Bhandari regarding the purchase of the car and payment of the aforesaid amounts. The CIT(A) called for the comments of the AO. Although the AO opposed the production of additional evidence but the CIT(A) allowed the

Assessee’s application and called for a remand report.

4.8 After examining the application of the Assessee, the letters submitted by Mr Sanjay Bhandari as well as the order of the Settlement Commission, the CIT(A) upheld the assessment order for addition of the value of the car under Section 69 of the Act. However, the CIT(A) enhanced the quantum of addition by Rs.2,92,694/- from Rs.1,37,07,306/- to Rs.1,40,00,000/-,which was the value computed by the Directorate of Revenue Intelligence (hereafter ‘DRI’).

5. In the aforesaid context, it would be expedient to examine the

explanation provided by the Assessee before the CIT(A) as well as the

explanation of Mr Sanjay Bhandari in his letter submitted by the Assessee before the CIT(A).

6. The relevant extracts of the letter dated 29th June, 2009 submitted by the Assessee before the CIT(A), which contains the Assessee’s explanation for being in possession of the car are quoted below:-

“(i) M/s VK Tour and Transport approached the Appellant

Company for exploring the possibility of giving vehicle No.

PB09G0052 on lease and possession was handed over to M/s

Provestment Securities Pvt Ltd for trial of the vehicle so that

the same, if found suitable, could be taken on lease by the

Company.

(ii) Meanwhile, when the vehicle was in possession of the

Company, DRI seized the vehicle. It was subsequently

informed to the Appellant Company that Vehicle No.

PB09G0052 was imported by M/s VK Tour and Transport

New Delhi against EPCG Licence No. 13000858 dated

25.01.2005 vide Bill of Entry 0985 dated 08-04-2005.

(iii) The vehicle was released by DRI provisionally on its

own volition on the condition of payment of differential duty

and execution of bond and bank guarantee for fine and penalty

to be made by the persons from whom the same was seized.

Thus, the Appellant Company was advised to make the

payment and also to submit the bank guarantee after which the

vehicle was given to it on superdari.

(iv) Accordingly, the payment of Rs.68,58,244/- towards

duty was made by the company comprising bankers cheque

No. 347142 dated 13.09.2005 for Rs.65,00,000/- of American

Express Bank Ltd and bankers cheque No. 243559 dated.

15.09.2005 of HSBC for Rs. 3,58,244/- which were duly

recorded in the books of accounts. Further an amount of Rs.

41,13,971/- was paid on 25.04.2007 vide bankers cheque No.

428331 dated 25.04.2007 as demanded by DRI.

(v) A show cause notice was Issued by DRI to M/s VK Tour

& Transport and to the Appellant Company. The Appellant

Company was advised to approach the Settlement Commission

primarily due to the fact that in case its petition is accepted, it

will get immunity from prosecution.

(vi) DRI after passing the final order on 20.12.2007,

released the vehicle to the Appellant Company and encashed

the Bank Guarantee of Rs.35,00,000/- given by the company

towards redemption fine of Rs. 7,13,000/-, penalty of

Rs.5,48,000/- and interest of Rs. 16,68,2 3 4/-.

(vii) The amount of Rs.68,58,2441/- was shown as duty

recoverable as on 31.03.2006 since the vehicle was

provisionally released to the Appellant Company, although the

vehicle was in its possession but the same was to be returned

to M/s V.K. Tour and Transport once the duty amount paid by

it is refunded.

(viii) When the final duty amounting to Rs.1,09,72,215/-

(inclusive of Rs.68,58,244/- which had already been paid

during the year ended 31.03.2006) was subsequently paid, the

entire amount comprising the duty, was paid by the Appellant

Company during the year ended 31.03.2008 and capitalized

under the head vehicle in the books of accounts. The balance

comprising of penalty, redemption fine and interest on the

differential duty amount was charged to the respective heads

during the year ended March 31,2008.

(ix) The Appellant Company has on date paid on aggregate

sum of Rs.1,39,01,449/- in respect of the said vehicle as per

the details given below:-

Date Amount Remarks

13.09.2005 65,00,000 Duty

15.09.2005 3,58,244 Duty

25.04.2007 41,13,971 Duty

22.01.2008 7,13,000 Redemption fine

22.01.2008 5,48,000 Penalty

22.01.2008 16,68,234 Interest

As such whatever payments have been made stand duly

reflected in the books and cannot be characterized as

investment from the undisclosed sources. The total amount

paid by the Assessee Company in respect of the said vehicle

amount toRs.1,39,01,449/- and not Rs.1,37,07,306/-."

7. Before the Assessing Officer, the Assessee contended that the

vehicle was imported by VKTT against EPCG Licence No. 13000858 dated

25th January, 2005 vide Bill of Entry 0985 dated 8th April, 2005. It was

stated that VKTT had approached the Assessee company for trial of the

vehicle and if found suitable, to enter into a lease agreement for the vehicle.

However, in the meantime, the vehicle in question was seized by DRI and

was subsequently released on the condition of payment of differential duty and execution of bond and bank guarantee for fine and penalty. The

Assessee had made payments towards duty and had also submitted a bond

and a bank guarantee for the fine. The vehicle was released on superdari

by the DRI and thereafter continued to be in possession of the Assessee.

8. Before the CIT(A), the Assessee repeated the above explanation.

However, the Assessee produced several documents to indicate that the

vehicle had been purchased by M/s History Logistics and was, thereafter,

transferred to VKTT (both proprietary concerns of Sanjay Bhandari). The

Assessee also produced a letter from Sanjay Bhandari which indicated that Sanjay Bhandari had agreed to transfer the vehicle to the Assessee or its nominee in consideration of the amounts paid by the Assessee to the Authorities for release of the vehicle and without any further consideration.

The letter also indicated that the duties had been paid by the Assessee on an understanding that the vehicle would be transferred to the Assessee on the final order being passed by the Settlement Commission.

9. It is apparent from the above that the Assessee claims that it had

neither executed any agreement for hire of the vehicle nor paid any

consideration for the vehicle in question; yet, the vehicle was registered at the address of the related entity and, indisputably, the Assessee/Sameer Thapar has been in physical possession of the vehicle from May 2005 (except for the few days that the vehicle was in possession of the DRI). Although the Assessee claims that the vehicle was to be leased to the Assessee, its actions are clearly not consistent with this position. If the vehicle was provided to the Assessee only for a trial purpose, there was no occasion for the Assessee to file an application or move the Settlement Commission for settlement of the duties with respect to the said vehicle or

seek release of the vehicle. However, the Assessee acted in complete

variance with this position; it paid the duty for release of the vehicle,obtained possession of the same on superdari and continued to use the vehicle. During the relevant period, Assessee showed the payment of duty as a recoverable from VKTT even though there was no agreement with VKTT for payment of such duty at the time nor was it produced at any later stage. During the year ended 31st March, 2008, the Assessee capitalized the payments of duty under the head of ‘vehicle’ in its books of accounts and the penalty, redemption fine and interest were debited by the Assessee under the respective heads. Thus, the Assessee indicated the payment of penalty, redemption fine and interest as its liability in its books during the year ended 31st March, 2008 and not as amounts paid on behalf of VKTT. At this stage, (i.e. during the year 31st March, 2008) the Assessee’s books reflected the Assessee to be the owner of the vehicle in question.

Concededly, no agreement had been entered into by the Assessee with

VKTT during the interregnum period entailing the transfer of the vehicle.On a query whether there was any change in the situation between 2005 when the vehicle was seized and 2008 for the Assessee to now hold out as an owner of the vehicle, the learned counsel for the Assessee answered in the negative. He submitted that vehicle in question had been shown as an asset under the head ‘vehicle’ in the year ending 2008 as the Assessee had paid the duty for the said vehicle. It is clear from the above that the payment of duties as well as the treatment accorded by the Assessee to such payments in its books militates against the Assessee’s explanation that it was only a hirer of the car in question and was not the owner. There is also no explanation as to why the Assessee had to make the payments of duty, if the Assessee did not own the asset seized.

10. At this stage, it would also be relevant to refer to the relevant

portions of the order passed by the Settlement Commission, which were

extracted by the CIT(A) in its order dated 31st March, 2010. The said

extracts are reproduced as under:-

“18.9. Shri H.S. Wig, Sr. VP, JCT Ltd.

represented Shri Sameer Thapar (With regard to two

vehicles BMW X5 DL2CAC 0002 and Lamborghini

Gelardo PBO9G 0052) during the hearing on

27.07.07.2007 and stated and also vide submission dated

30.07.2007, submitted that the co- applicant had taken

the said vehicles on Hire Agreement dated 03.09.2002

from Shri Sanjay Bhandari for 3 years. DRI seized the

vehicle vide Panchnama dated 10.09.2005. It was

prayed that the co-applicant be granted waiver from

penalty, redemption fine, interest and prosecution. He

also prayed that the Bank guarantee and Provisional

Duty Bond furnished by him the DRI be also released.”

“22. ...Bench notes that it is not a solitary case of

import of a single vehicle by a person or a firm. A large

number of vehicles have been imported over a period of

time under 30 EPCG licenses. DRI's investigations have

very clearly brought out that EPCG licenses were

obtained by resorting to mis-declaration of premises

with regard to their status vis-à-vis the activity declared

to be carried out from the said premises. Investigations

have also clearly brought out that vehicles were

transferred to other persons by resorting to different

kinds of subterfuges and were not used for the purpose

for which they were imported under the respective

EPCG Licenses. It is immaterial whether the ownership

of the vehicles was transferred or not in a legal manner.

Perhaps legal transfer of the vehicles was not possible as

it could have resulted in creation of evidence that the

vehicles were not used for the purpose for which they

were imported. Different kinds of deceptions were

adopted by the firms and the company operating through

Shri Sanjay Bhandari who was their Proprietor/Director

to part with the vehicles and yet take advantage of duty

concession under the EPCG Scheme and also to show

fulfillment of export obligation. Evidence unearthed by

DRI has very clearly proved that dishonest motive of

evading duty was the sole objective behind the import of

these 61 vehicles. Such a motive is quite manifest

despite the dissembling resorted to on the papers.

Bench, on a careful consideration of the evidence and

facts and circumstance of the cases, is convinced that

these imports were actuated by a dishonest motive of

making profit by evading payment of appropriate

Custom Duty. Even the so called fulfillment of the

export obligation was not achieved from the foreign

exchange generated from or through the use of these

vehicles. Evidence shows that remittances were made

from some other source. In view of this position, Bench

is of the view that the arguments of the ld. advocate in

favour of grant of immunity have no substance and the

main applicants can not be granted full immunity from

penalty and redemption fine.

23. ...In the present case, Bench has already

observed in para 22 above that it was a well-planned

operation on the part of Shri Sanjay Bhandari wherein

deceitful contrivances and tricks were adopted to evade

payment of due customs duty, yet maintain the façade of

observance at the conditions of EPCG scheme and

thereby make undue profit at the cost of exchequer.

Further the duty evaded was paid as differential duty

only after the DRI was able to unearth the racket and

seize 55 vehicles. Therefore duties were paid belatedly

and to that extent the main applicants have enjoyed

financial accommodation at the cost of Government

Exchequer.....”

“25 ..... Bench finds that it is quite obvious that they

were complicit in improper transfer of the vehicles in

question the imports of which are tainted by evasion of

customs duty. All the, vehicles were of foreign origin and

were, relatively speaking, of high value. There is evidence

in case of a number of vehicles that prior arrangements

were made between the main applicants and the

transferees and amounts were received from the persons to

whom the said vehicles were claimed to have been leased

out. It can not be believed that they had taken over these

vehicles without checking up the import documents. As

such, the Bench holds them liable to penalty.

...Similarly, co-applicant Shri Sameer Thaper is also

not entitled to release of bank guarantee and provisional

duty bond for the reasons of his complicity in the entering

of hire agreement to circumvent the provisions of the

EPCG Scheme with regard to two vehicles.”

11. The vehicle was registered on 23rd May, 2005 and it is apparent that

even at the time of registration, it was known that the vehicle would be

used by JCT, Sameer Thapar or any of the Thapar Group entities. The only

explanation offered before the DRI for registering the car at the address of JCT is that this had been done to inspire confidence and secure the concerns of JCT. However, as per the version of the Assessee, there was no agreement in May 2005 for lease of the vehicle and the vehicle in question was handed over only for the purposes of a trial. According to the statement made by Mr Satish Kapoor (an officer of JCT) before the DRI,the vehicle continued to be in possession of Mr Sameer Thapar from May till 10th September, 2005 when it was seized by DRI. Thus, admittedly, the vehicle continued to be in possession of Mr Sameer Thapar from the month of its registration till its seizure but no agreement for lease or hire of the vehicle had been executed. Although, it is stated that in addition to lease rentals the Assessee/JCT Ltd. was also to place a security deposit with Mr Sanjay Bhandari/VKTT, concededly, no such deposit had been placed. It was also material to note that there is also a variance in the amount of the

security deposit payable to VKTT; whilst Mr Sameer Thapar, in his

statement recorded u/s 108 of the Customs Act, 1962, claims that Rs.48

lacs was payable as security deposit whereas the Assessee Company in its

reply dated 22nd November, 2008 to the show cause notice dated 19th

November, 2008 claims that the security deposit was Rs.60 lacs.

12. The CIT(A) examined the relevant facts and rejected the explanation

offered by the Assessee for being in possession of the vehicle as a hire.

13. It does appear that the Assessee’s explanation of coming into

possession of the vehicle only for trial purposes and continuing to be in possession of the vehicle is a subterfuge. However, the question to be addressed is whether, in the facts and circumstances of the case, the value of the vehicle could be added to the income of the Assessee under Section 69 of the Act.

14. At this stage it is necessary to refer to Section 69 of the Act, which reads as under:-

“69. Where in the financial year immediately preceding the

assessment year the assessee has made investments which are not

recorded in the books of account, if any, maintained by him for

any source of income, and the assessee offers no explanation

about the nature and source of the investments or the explanation

offered by him is not, in the opinion of the Assessing Officer,

satisfactory, the value of the investments may be deemed to be

the income of the assessee of such financial year.”

15. It is apparent from the plain language of Section 69 of the Act that in order for any addition to be made under Section 69 of the Act, the

following conditions must be met:

(a) it is established as a fact that the Assessee has made an investment;

(b)that the investment made is not recorded in the books of the

Accounts, if so maintained; and

(c) the Assessee offers no explanation as to the nature and source of

investment made or the explanation offered by the Assessee is, in the

opinion of the AO, not satisfactory.

16. Thus, first and foremost, AO must come to a conclusion that an

Assessee had, in fact, made an investment. Once an AO finds that an

investment has been made, he has to examine the Assessee’s explanation as to the source of that investment. It is only in cases where the Assessee is unable to explain the source of the investment made that provisions of Section 69 of the Act can be applied to tax the value of the investment made.

17. In the present case, the threshold condition of the Assessee making

an investment is not satisfied. Before the CIT(A), the Assessee had

produced additional evidence. This included; (i) copy of the Invoice

No.73015 dated 6th April, 2005 issued by London Country Club Ltd. in

favour of M/s History Logistics (Prop. Sh. Sanjay Bhandari) for purchase

of car; (ii) copy of Letter of Credit No.01790002340204 issued by Oriental Bank of Commerce, New Delhi for GBP 85395; (iii) copy of Bank Advice dated 15th April, 2005 for Rs.17,89,972/- (enclosure of Bank Charges) towards payment of the purchase of car; (iv) copy of Marine Insurance Policy No. 1000025538 dated 24th November, 2004 for Rs.23,419/-; (v)Copy of Invoice No. HL002/04-05 dated 31st March, 2005 for sale of Rs.72,05,521/- for sale of car on High Sea Sale basis by M/s History Logistics to VKTT; (vi) Copy of challans/invoice for payment of Insurance of Rs.2,96,763/-, Custom Duty of Rs.4,89,668/-, Commission Agency Charges of Rs.42,978/- and other charges of Rs. 88,945/-. The Assessee had also produced a letter from Sanjay Bhandari. The relevant extract of which reads as under:-

“2. That the said Vehicle was purchased from London

Country Club Limited 1-2 Rutland Garden, Knights

bridge London vide their Invoice No 73015 dated

06/04/2005 for GBP85395.00 (Invoice copy enclosed).

3. That the payment of the said invoice was made by my

bankers, Oriental Bank of Commerce, Connaught Place,

New Delhi vide, their Letter of Credit No:

0179000230204dated 21/12/2004 and on 15/04/2005

and the account of History Logistics was debited for Rs.

70,77,773/-. Apart from above bank charges of Rs.

12,199/- were also paid by History Logistics, New Delhi.

(Copy of L/C, payment as well as relevant Bank

Statement are enclosed)

4. Further a sum of Rs. 23,4797- was also paid to Reliance

General Insurance Company towards Marine Insurance

vide Cheque No: 108516 dated 24/11/2005.

5. The said vehicle was sold by History Logistics to V.K.

Tours and Transport vide their Invoice No. HL002/04-05

dated31/03/2005 for Rs.72,05,5211- vide High Sea Sale

Agreement and Contract between both the parties was

executed on 04/04/2005.Please note that V.K. Tour and

Transport is also a proprietary concern and proprietor

being the undersigned.(Copy of Invoice enclosed). The

High Sea Sales Agreement was executed as the EPCG

license for the B5/ 110, 2nd floor, Safdarjung Enclave,

New Delhi- 110029 import of the said car could not

granted to History Logistics, but was granted to V.K.

Tour and Transport instead.

6. All custom formalities were then completed by V.K.

Tours and Transport and amount of Rs.4,89,968/- was

paid to Custom authority towards Import duty. Apart

from the above payment of Rs. 42,978/- was made as

clearing agency charges and Rs. 88,945/- as other

incidental expenses (Copy of Bill of entry as well as the

bills are enclosed).

7. The said vehicle was imported under EPCG scheme

under import License No. 1330000858 dated 25/01/2005

issued by DGFT, Jaipur, Rajasthan.

8. After clearing all the custom formalities the delivery of

the vehicle was taken by V.K. Tours and Transport and

the vehicle was registered in their name under

Registration No: PB 09 G0052 on 23/05/2005 (Copy

enclosed).

9. Undersigned approached you to take the car on lease

and it was agreed that you shall pay Rs. 2lacs every

month as lease rental for three years and also make a

security deposit of Rs. 48lacs. Further it was also agreed

that in case you decide to purchase the vehicle in the

future, the security deposit of Rs.48 lacs shall be

appropriated and be treated as the payment of the

vehicle otherwise the security deposit shall be released

on the return of the car. However before the agreement

could be executed, the DRI initiated an investigation of

all firms of Shri. Sanjay Bhandari. Along with 54

vehicles, this vehicle was seized by DRI on 10/09/2005

and therefore the lease deed could not be finalized.

10. After the seizure of the vehicle by DRI, to take provisional

release of the vehicle, you made a revenue deposit of

Rs.68,58,244/- toward the differential duty/duty forgone

and also furnished the bank guarantee for Rs 35 lacs

favoring the Authorities.

11. Vide their Show Cause Notice, the DRI on

23/08/2006further additional payment of Rs. 41,13,971/-

toward Custom Duty and the same was also paid on

26/04/2007 by you on our behalf after admission of my

application with the Hon'ble Settlement Commission vide

their order dated 28/12/2006.

12. The above payments were made by you with an

understanding that as and when the Settlement

Commission would pass a final order, V.K. Tour and

Transport, after fulfilling the conditions of the order,

would receive a final release of the vehicle and be

legally allowed to transfer the ownership of the

abovementioned vehicle, the same shall be transferred to

your desired name, or your nominee in as true and

absolute owner for no further consideration.

13. The Settlement Commission vide its order dated

20/12/2007has allowed our application by imposing

redemption fine, penalty and interest amounting to Rs.

31,38,755/- in this car, which has since been paid by you

on our behalf.

14. Although the Settlement Commissioner has passed the

order on 20/12/2007, still the vehicle could not be

transferred to you due to differences between me and

DRI on calculation of interest for the waiver period

provide, along with non-consideration of some valid

notifications in the final order, I have challenged the

Final Order after depositing over Rs. 5.24Crores before

the Bombay High Court, the case is awaiting final

disposal. The DRI has also challenged the immunity

granted to me and my co-applicants by the Settlement

Commission, before the Hon'ble Delhi High Court, the

proceeding are awaiting final disposal. The car cannot

be transferred pending these litigations.”

18. It is apparent from the above that the Assessee had produced

sufficient material to establish that the vehicle had been imported by the Sanjay Bhandari (in the name of VKTT) and evidence was also produced to show payment of the cost of the vehicle. The AO on the other hand, has discovered no evidence or material on the basis of which it could be

concluded that the cost of the vehicle and the initial duty had not been paid by Sanjay Bhandari. The assertion that the Letter of Credit had been issued by Oriental Bank of Commerce on 21st December, 2004 and subsequently,the Bank Account of M/s History Logistics had been debited by a sum of Rs.70,77,773/- towards cost of the vehicle has not been contested by the AO or the CIT(A). Neither the AO nor the CIT(A) has any material to dispute these assertions.

19. In the circumstance, we are inclined to agree with the Tribunal that

the question whether an investment had been made or not is a matter of fact and the same cannot be presumed. In the present case, it is probable that either the Assessee or any other person related to the Assessee, would have paid for acquiring the vehicle in question. An investigation into the sources of the funds of Sanjay Bhandari/VKTT may perhaps have established a link between the funds used for the purchase of the vehicle and JCT/Sameer Thapar/the Assessee. However, no such link has been established. In absence of any material to show that the consideration for the vehicle had not been paid by Sanjay Bhandari/M/s History Logistics, it is not possible to conclude that the Assessee had made an investment in purchase of the vehicle in question.

20. In the facts and circumstances, we are unable to hold that the

decision of the Tribunal is perverse. The questions of law framed are

answered in affirmative and in favour of the Assessee and against the

Revenue.

21. The Appeal is, accordingly, dismissed. Parties are left to bear their own costs.

VIBHU BAKHRU, J

S. MURALIDHAR, J

NOVEMBER 30, 2015

×

Similar Ripples

Questions

Assessee Wins: No Evidence of Unexplained Investment in Lamborghini

Write your CommentGeneric

- Reportdata/3281.pdf