Assessing Officer’s Reopening Notice Quashed: Court Upholds Original Assessment…

Full News

Assessing Officer’s Reopening Notice Quashed: Court Upholds Original Assessment Decision

Assessing Officer’s Reopening Notice Quashed: Court Upholds Original Assessment Decision

In the case of Nirma Ltd. vs. Deputy Commissioner of Income Tax, the court addressed whether the Assessing Officer (AO) could reopen an assessment based on grounds previously rejected in the original assessment. The court ruled against the reopening, emphasizing that the AO must rely on the original order of assessment and cannot issue a notice of reopening on grounds already considered and rejected.

Get the full picture - access the original judgement of the court order here

Case Name:

Nirma Ltd. vs. Deputy Commissioner of Income Tax (High Court of Gujarat)

Special Civil Application No. 16613 of 2010

Date: 30th August 2016

Key Takeaways:

- The court reinforced that an AO cannot reopen an assessment on grounds that were already examined and rejected in the original assessment.

- The decision highlights the importance of finality in assessments and the limitations on the AO’s power to revisit decisions.

- The ruling underscores the necessity for the AO to rely on the original assessment order unless new, valid grounds for reopening are presented.

Issue:

Can the Assessing Officer reopen an assessment on grounds that were already considered and rejected in the original assessment order?

Facts:

- Nirma Ltd. filed a return of income for the Assessment Year 2005-06, which was scrutinized by the AO, resulting in an assessed income of Rs.370.12 crores.

- The AO initially disallowed a claim of interest expenditure on Deep Discount Bonds due to non-deduction of tax at source.

- Despite this, the AO issued a notice to reopen the assessment, citing the same grounds previously rejected.

- Nirma Ltd. challenged this notice, arguing that the issue had already been examined and rejected in the original assessment.

Arguments:

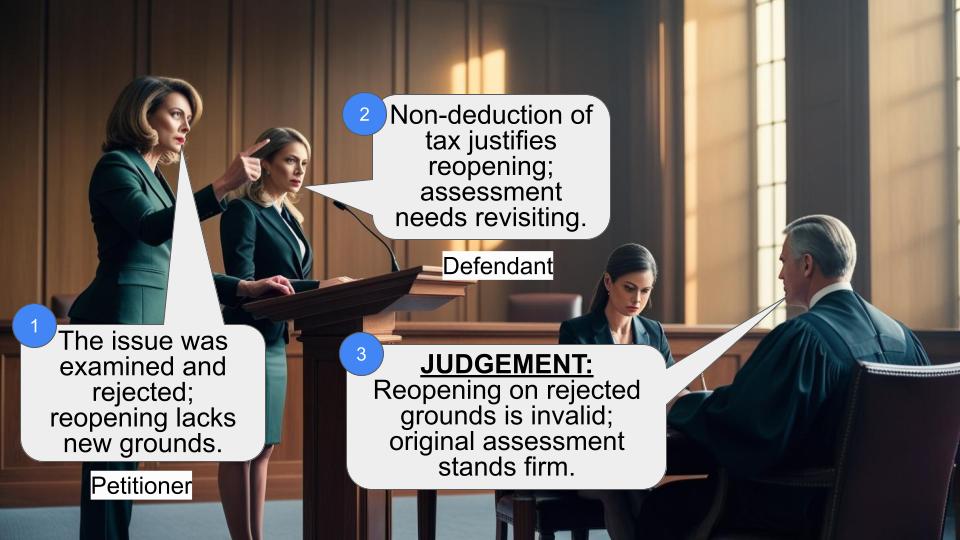

- Nirma Ltd.: Argued that the AO had no valid grounds to reopen the assessment as the issue had been thoroughly examined and rejected in the original assessment. They contended that no income had escaped assessment.

- Revenue: Claimed that the non-deduction of tax at source on the interest expenditure justified the reopening of the assessment under Section 40(a)(ia) of the Income Tax Act, 1961.

Key Legal Precedents:

- The court referenced the principle that reopening an assessment is not permissible on grounds already considered and rejected. The case of Gujarat Power Corporation Ltd. was mentioned, but the court noted its limited applicability when the AO has already rejected a claim.

Judgement:

The court quashed the reopening notice, ruling in favor of Nirma Ltd. It held that the AO could not reopen the assessment on grounds that were already examined and rejected. The court emphasized that the AO must rely on the original assessment order unless new grounds are presented.

FAQs:

Why was the reopening notice quashed?

The notice was quashed because the AO attempted to reopen the assessment on grounds that were already considered and rejected in the original assessment.

What does this decision mean for future assessments?

It reinforces the principle that AOs cannot revisit decisions on the same grounds without new evidence or reasons, ensuring finality in assessments.

Can the AO ever reopen an assessment?

Yes, but only if there are new grounds or evidence that justify the reopening, not on previously rejected grounds.

1. The petitioner has challenged a notice dated 30.3.2010 issued by the respondent – Assessing Officer to reopen the assessment of the petitioner for the Assessment Year 2005-06.

2. Brief facts are as under :

2.1 The petitioner is a company registered under the Companies Act. For the Assessment Year 2005-06, the petitioner had filed a return of income on 31.10.2008 declaring total income of Rs.164.15 crores (rounded off). A revised return was filed on 28.3.2007 declaring Nil income. The return was taken in scrutiny by the Assessing Officer. He passed the order of assessment under Section 143(3) (of Income Tax Act, 1961) (for short ‘the Act’) on 31.12.2007 assessing total income at Rs.370.12 crores. To reopen such assessment, the Assessing Officer issued the impugned notice. For such purpose, he had recorded the following reasons : “The assessee company filed return of income on 28.3.2006, declaring total income at Rs.NIL. Assessment u/s.143(3) (of Income Tax Act, 1961) was finalized on 31.12.2007, determining total income at Rs.370,12,92,640/-.

2. On verification of records, it is seen that the assessee has claimed interest expenses of Rs.26,40,09,503/- on Deep Discount Bonds. Hence, it is seen that the assessee claimed the interest expenditure but no TDS was made from the same, even though there was redemption of DDBs to Nirma Chemical Works Ltd. Therefore, the claim was required to be disallowed u/s.40(a)(ia) (of Income Tax Act, 1961), which has not been done.

3. Hence, I have reason to believe that income chargeable to tax has escaped assessment within the meaning as envisaged by section 147 (of Income Tax Act, 1961) r.w explanation 2(c) of the Act.”

2.2 The petitioner raised detailed objections to the notice for reopening under a letter dated 10.12.2010. Such objections were, however, rejected on 20.12.2010. Hence, this petition.

3. Taking us through the materials on record, learned counsel for the petitioner raised following contentions :

(i) There was no income which had escaped assessment and in that view of the matter, the reasons recorded by the Assessing Officer lack validity.

(ii) The entire issue based on which the notice of reopening is issued was minutely examined and the claim of the assessee was rejected by the Assessing Officer during the original assessment.

(iii) The question of interest expenditure of Rs.26.40 crores (rounded off) on deep discount bonds has merged with the decision of CIT (Appeals) in an appeal filed by the assessee.

4. On the other hand, learned counsel for the revenue submitted that in the reasons recorded, the Assessing Officer referred to non-deduction of tax at source on the interest expenditure which would invite dis-allowance under Section 40(a)(i) (of Income Tax Act, 1961). This was not the ground on which the Assessing Officer had rejected the claim of the expenditure in the assessment.

5. Having thus heard learned counsel for the parties and having perused the documents on record, we may recall that in the reasons recorded the Assessing Officer referred to assessee’s claim of interest expenditure of Rs.26.40 crores on Deep Discount Bonds. In his opinion, since on such expenditure, no tax was deducted at source, the same had to be disallowed in terms of Section 40(a)(ia) (of Income Tax Act, 1961). It was on this premise that the Assessing Officer recorded his reasons to believe that income chargeable to tax has escaped the assessment.

6. However, when we peruse the order of assessment dated 30.12.2007, we notice that the claim of interest expenditure of Rs.26.40 crores came up for consideration at the hands of the Assessing Officer. In the order of assessment itself, he has devoted several pages to come to the conclusion why according to him, such expenditure claimed by the assessee on accrual basis was not a valid claim. Eventually, in the order of assessment, he disallowed the claim observing as under :

“In the light of all these observations, the claim of the assessee pertaining to accrued interest on these DDBs is hereby disallowed, thus Rs.26,40,09,503/- is hereby disallowed.

The penalty proceedings u/s.271(1)(c) (of Income Tax Act, 1961) are separately initiated on this issue for furnishing the inaccurate particulars of income and thereby concealing the income.”

7. The conclusion of the Assessing Officer is based on his perception that the liability to pay interest on this Deep Discount Bonds had not accrued and would accrue only at the end of the period of the bond. He was further of the opinion that deductions under Section 36 (of Income Tax Act, 1961) are such which may not be allowed as revenue expenditure unless provided under Section 36 (of Income Tax Act, 1961). The assessee could not have claimed such expenditure on prorata basis.

8. Significantly, he was also conscious about the provision for deducting TDS on such expenditure. In this respect, he observed as under :

“v) The assessee has also not deducted the TDS on all the accrued interests. If the assessee claims the same it shall be implied obligation on the part of the assessee to deduct TDS, but the same has not been done, therefore the assessee would become liable for penalty. As per Explanation to sec.193 (of Income Tax Act, 1961), it has been clarified that if the assessee claims such interest by crediting the ‘interest payable account’ or ‘suspense account’, it is bound to deduct the TDS on the same but the same has not been done. Therefore if the assessee claims this exp., then the assessee is bound to deduct the TDS. The relevant Explanation of sec.193 (of Income Tax Act, 1961) is produced as under :

Explanation.-For the purpose of this section, where any income by way of interest on securities is credited to any account, whether called ‘ interest payable account’ or ‘suspense account’ or by any other name, in the books of account of the person liable to pay such income, such crediting shall be deemed to be credit of such income to the account of the payable and the provisions of this section shall apply accordingly.

This shows that assessee itself treats the premium as capital expenditure of future and does not treat it as interest by not deducting TDS.”

9. It can thus be seen that the Assessing Officer had examined the entire claim from various angles and concluded that the claim of expenditure of the assessee was not valid. That being the position, in plain terms he could not have resorted to reopening of the assessment on the ground that the expenditure had to be disallowed for not deducting the tax at source. Firstly, this aspect was also in his mind when he passed the order of assessment. Secondly, on various grounds he had himself rejected the claim. Having thus examined the claim and in fact, having rejected the same, the Assessing Officer must rely on the order of assessment. He cannot issue a notice of reopening on this very ground which he rejected in the order of assessment. In fact, when reasons were recorded and the notice for reopening was issued, his view on this issue was confirmed by the CIT (Appeals). Though we are informed that subsequently the Tribunal had allowed the assessee’s appeal on this issue; on the date on which the reasons were recorded and notice was issued, the order of CIT (Appeals) prevailed. On all grounds therefore, we cannot uphold the impugned notice.

10. Learned counsel for the revenue tried to bring in the observations made by this Court in case of Gujarat Power Corporation Ltd. V/s. Assistant Commissioner of Income-Tax, reported in 350 ITR 266, to contend that if an element of a claim had not been examined during the scrutiny assessment, reopening on such basis may still be, in a given case, permissible. Quite apart from very limited application of such observations in exceptional cases, obviously the same would not apply when the Assessing Officer has rejected the claim. In other words, there cannot be a reopening of assessment for rejecting a claim on an additional ground which for whatever reason the Assessing Officer did not press in service during the original assessment. In fact, in the present case, he did not even miss-out on the later ground on which the notice for reopening has been premised. For all the reasons, the impugned notice dated 30.3.2010 is quashed. Petition is allowed and disposed of.

(AKIL KURESHI, J.)

(A.J. SHASTRI, J.)

×