Conflict on Section 80AC (of Income Tax Act, 1961): Mandatory or Directory? Cou…

Full News

Conflict on Section 80AC (of Income Tax Act, 1961): Mandatory or Directory? Court Sides with ITAT

Conflict on Section 80AC (of Income Tax Act, 1961): Mandatory or Directory? Court Sides with ITAT

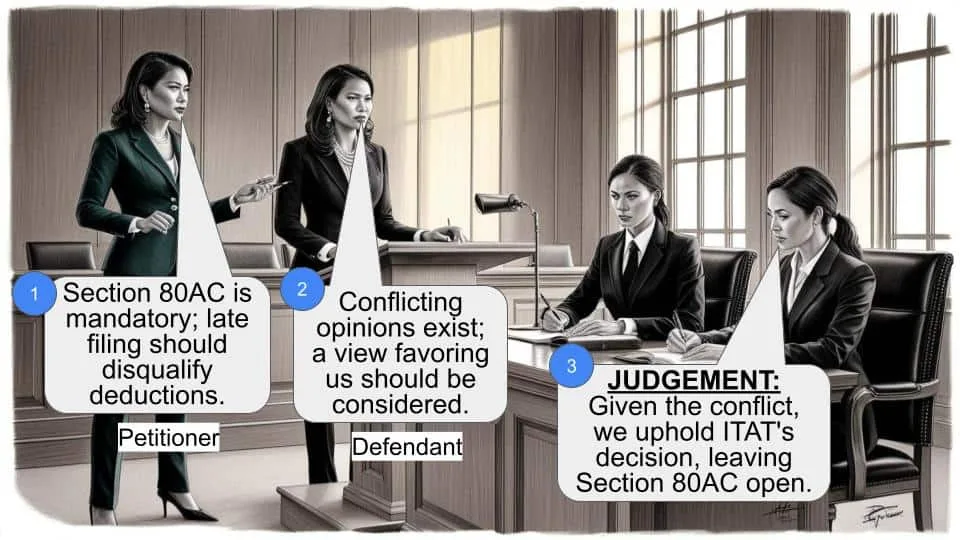

In the case of Commissioner of Income Tax vs. Unitech Ltd., the court addressed whether the requirement under Section 80AC (of Income Tax Act, 1961), which mandates filing returns by a specific deadline, is mandatory or directory. The Income Tax Appellate Tribunal (ITAT) had previously ruled in favor of the assessee, Unitech Ltd., due to conflicting opinions on the matter. The court upheld the ITAT’s decision, leaving the question open for future consideration.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs. Unitech Ltd. (High Court of Delhi)

ITA 239/2015 & CM No. 6678/2015

Date: 5th October 2015

Key Takeaways:

- The court acknowledged a conflict in opinions regarding whether Section 80AC (of Income Tax Act, 1961) is mandatory.

- The ITAT’s decision to favor the assessee was upheld due to this conflict.

- The court did not make a definitive ruling on the mandatory nature of Section 80AC (of Income Tax Act, 1961), leaving it open for future cases.

Issue

Is the requirement under Section 80AC (of Income Tax Act, 1961), which mandates filing returns by a specific deadline, mandatory or directory?

Facts

- Unitech Ltd. filed its income return late for the assessment year 2008-09 but claimed a deduction under Section 80IB(10) (of Income Tax Act, 1961).

- The Assessing Officer allowed this deduction, but the Commissioner of Income Tax (CIT) challenged it under Section 263 (of Income Tax Act, 1961), arguing the late filing violated Section 80AC (of Income Tax Act, 1961).

- The ITAT ruled in favor of Unitech Ltd., citing conflicting opinions on the mandatory nature of Section 80AC (of Income Tax Act, 1961).

Arguments

- Revenue’s Argument: Section 80AC (of Income Tax Act, 1961) is mandatory, and late filing should disqualify the deduction.

- Assessee’s Argument: There is a conflict in judicial opinions, and a view favoring the assessee can be taken.

Key Legal Precedents

- CIT v. Integrated Databases (I) Ltd. and CIT v. Contimeters Electricals § Ltd. were referenced but not directly applicable to the Section 80AC (of Income Tax Act, 1961) issue.

- CIT v. Sri S Venkataiah and decisions from the Uttarakhand and Calcutta High Courts supported the mandatory view of Section 80AC (of Income Tax Act, 1961).

Judgement

The court upheld the ITAT’s decision, noting the conflict in opinions and the lack of an authoritative pronouncement on Section 80AC (of Income Tax Act, 1961)’s mandatory nature. The appeal by the Revenue was dismissed, and the question was left open for future consideration.

FAQs

Q1: What does this decision mean for taxpayers?

A1: It means that, for now, there is no definitive ruling on whether Section 80AC (of Income Tax Act, 1961) is mandatory, allowing for some flexibility in interpretation.

Q2: Why didn’t the court make a definitive ruling?

A2: The court recognized the existing conflict in opinions and chose to leave the question open for a more appropriate case.

Q3: What should taxpayers do if they file late?

A3: While this case provides some leeway, it’s advisable to file returns on time to avoid potential disputes.

CM No. 6678/2015 (Delay in refiling)

1. For the reasons stated in the application, the delay of 296 days in

refiling the appeal is condoned.

2. The application stands disposed of.

3. This is an Appeal by the Revenue against the order dated 18th December,2013 passed by the Income Tax Appellate Tribunal (‘ITAT’) in ITA No.1014/Del/2012 for the Assessment Year (AY) 2008-09.

4. In the present case the Assessee filed its return of income for the AY in question on 2nd April 2009 claiming the benefit of deduction under Section 80IB(10) (of Income Tax Act, 1961). This was allowed by the Assessing Officer (AO) while making assessment under Section 143(3) (of Income Tax Act, 1961) of the Income Tax on 30th December,2009. In terms of Section 80AC (of Income Tax Act, 1961) the return had to be filed by the Assessee, ‘on or before the due date specified under Section 139(1) (of Income Tax Act, 1961)’, whichin this case meant on or before 31st October, 2008.

5. A short question before the Commissioner of Income Tax (CIT) who

initiated proceedings under Section 263 (of Income Tax Act, 1961) and proceeded to withdraw the

deduction claimed by the Assessee under Section 80IB(10) (of Income Tax Act, 1961) was whether the

requirement under Section 80AC (of Income Tax Act, 1961), that the return had to be filed within the time prescribed under Section 139(1) (of Income Tax Act, 1961), was mandatory.

6. The ITAT in the impugned order allowing appeal filed by the Assessee

noted that there was a cleavage of opinion on the issue as was evident from two lines of decisions of the ITAT itself. Since a possible view in favour of the Assessee could be taken if one line of decisions was applied, the ITAT concluded that there was no justification for CIT to have invoked the jurisdiction Section 263 (of Income Tax Act, 1961).

7. Before this Court Mr Rohit Madan, learned Standing Counsel for the

Revenue has placed reliance on the decision dated 27th August 2012 of the Uttarakhand High Court in ITA No. 07/2012 (Umesh Chandra Dalakoti v.

Assistant Commissioner of Income Tax) as well as of the Calcutta High

Court in CIT v. Shelcon Properties (P) Ltd. [2015] 370 ITR 305 (Cal) both of which have held the provision under Section 80AC (of Income Tax Act, 1961) to be mandatory. He has also referred to the decisions of the ITAT Special Bench in Saffire Garments v. ITO 20 ITR (Trib) 623, of the ITAT Madras Bench in 1219-1223/MDS/2012 (ACIT v. Shri V.N. Devadoss), of the ITAT

Chandigarh Bench in 250-2511CHD/2003 (Lakshmi Energy and Foods

Ltd. v. ACIT) and the decision dated 30th January 2015 of the ITAT

Mumbai Bench in ITA No. 4727/Mum/2012 (Dwarkadas Panchmatiya v.

ACIT).

8. Mr Salil Aggarwal, learned counsel for the Assessee, on the other hand,has placed reliance on the decisions of this Court in CIT v. Integrated Databases (I) Ltd. (2009) 178 Taxman 432 (Del) and CIT v. Contimeters Electricals (P) Ltd. (2009) 178 Taxman422 (Del). He also placed reliance on the decision dated 26th June 2013 of the Andhra Pradesh High Court in

ITTA No. 114 of 2013 (CIT v. Sri S Venkataiah), the decisions dated 29th

April 2013 of the ITAT Madras in ITA No. 1214/Mds/2012 (ACIT v. Precot

Meridian Ltd.) and 4th February 2013 in ITA No. 1219-1223/Mds/2012

(ACIT v. V.N. Devadoss), the decisions of the ITAT Delhi dated 30th July

2010 in ACIT v. Dhir Global Industrial (P) Ltd. 133 TTJ (Del) 580 and

dated 25th January 2012 in ITA No. 3352/Del/2011(Hansa Dalakoti v.

ACIT), the decision of the Bangalore ITAT dated 12th April 2103 in M/s

Vanshee Builders & Developers P. Ltd. v. CIT 63 SOT 30 and the decision

of the Kolkata ITAT dated 19th April 2013 in ITA No. 1586/Kol/2012 (M/s

Shelcon Properties (P) Ltd. v. JCIT).

9. The Court notices at the outset that the decisions of this Court both in CIT v. Integrated Databases (I) Ltd. (supra) and CIT v. Contimeters Electricals (P) Ltd. (supra) were on the question whether the provision of Section 10-B(5) (of Income Tax Act, 1961) which requires the filing of a report of an accountant along with the return was mandatory. Neither decision was directly on question whether the time limit for filing the return in terms of Section 80AC (of Income Tax Act, 1961) read with Section 139(1) (of Income Tax Act, 1961) was mandatory. Although the decision of the A.P. High Court in CIT v. Sri S Venkataiah (supra) concerned this very issue, it was one declining to frame a question of law thereby affirming the order of the ITAT. It was a short order in the facts of the case where the Assessee appears to have shown “reasonable cause for filing the return of income belatedly” and that it was “beyond the control of the Assessee.” On

the other hand, the decisions of the Uttarakhand High Court in Umesh

Chandra Dalakoti (supra) and of the Calcutta High Court in CIT v. Shelcon Properties (P) Ltd. (supra) appear to support the case of the Revenue that Section 80 (of Income Tax Act, 1961) AC is mandatory. However, there appears to be no authoritative pronouncement of this Court on the interpretation of Section 80AC (of Income Tax Act, 1961) and whether the said provision is mandatory or directory.

10. As far as the present case is concerned, the Court is satisfied that at the time when the CIT passed the order dated 6th February, 2012 under Section 263 (of Income Tax Act, 1961) there was a conflict of opinions of the various benches of the ITAT on whether 80AC was mandatory. Consequently, the ITAT was not in error in reversing the order of the CIT as far as the question of exercising jurisdiction under Section 263 (of Income Tax Act, 1961) was concerned. No substantial question of law arises on the said issue.

11. It is clarified that the question whether the requirement under Section 80AC (of Income Tax Act, 1961) is mandatory is left open for consideration in an appropriate case. The appeal is dismissed in the above terms.

S.MURALIDHAR, J

VIBHU BAKHRU, J

OCTOBER 05, 2015

×

Similar Ripples

Questions

Conflict on Section 80AC (of Income Tax Act, 1961): Mandatory or Directory? Court Sides with ITAT

Write your CommentSimilar Posts

Generic

- Reportdata/3403.pdf