Court Allows Interest Deduction for Company's Interlinked Transactions

Full News

Court Allows Interest Deduction for Company's Interlinked Transactions

Court Allows Interest Deduction for Company's Interlinked Transactions

This case involves the Principal Commissioner of Income Tax (Revenue) and Jubilant Energy NELP-V-Pvt. Ltd. (assessee). The dispute centered around the deductibility of interest paid by the assessee on inter-corporate deposits (ICDs) and the taxability of interest earned. The High Court dismissed the Revenue's appeal, allowing the assessee to deduct the interest paid against the interest earned.

Get the full picture - access the original judgement of the court order here

Case Name:

Principal Commissioner of Income Tax Vs Jubilant Energy Nelp-V-Pvt. Ltd. (High Court of Delhi)

ITA 1440/2018

Date: 12th December 2018

Key Takeaways:

1. Interest paid to earn interest can be allowed as a deduction under Section 57 (of Income Tax Act, 1961) when there's a direct nexus between interest paid and received.

2. The court emphasized the importance of factual evidence in determining the nature of transactions and business setup.

3. The judgment highlights the significance of proper documentation and cash flow statements in tax disputes.

Issue:

Was the assessee entitled to deduct the interest paid on ICDs against the interest earned, and was the assessee's business set up for tax purposes?

Facts:

- Jubilant Energy NELP-V-Pvt. Ltd. was incorporated on March 13, 2007, for oil and gas exploration.

- The company entered into a business transfer agreement with Jubilant Capital Private Limited and Jubilant Securities Private Limited.

- The assessee took ICDs of Rs. 55.30 Crores at 12% interest from Jubilant Energy (Kharsang) Private Limited.

- Rs. 50 Crores from these ICDs were advanced to Jubilant Enpro Private Limited at 12.5% interest.

- The assessee paid interest of Rs.1,88,98,763/- and earned interest of Rs. 1,78,03,962/-.

- The company incurred expenses on operations and support staff and provided performance bank guarantees for two oil blocks.

Arguments:

Revenue's Arguments:

- The assessee's business was not set up and ready for commencement.

- Interest paid should be capitalized, not allowed as a revenue expense.

- Interest earned should be taxed under "income from other sources" and not set off against interest paid.

Assessee's Arguments:

- There was a direct nexus between interest paid and received.

- The business was set up as evidenced by the business transfer agreement and incurred expenses.

- The company had commenced business activities, including providing performance guarantees.

Key Legal Precedents:

The judgment doesn't explicitly mention any specific legal precedents. However, it refers to Sections 57 and 35D of the Income Tax Act, 1961.

Judgement:

The High Court dismissed the Revenue's appeal and ruled in favor of the assessee. Key points of the judgment include:

1. The court accepted the direct nexus between interest paid and received on ICDs.

2. Interest paid to earn interest was allowed as a deduction under Section 57 (of Income Tax Act, 1961).

3. The court found sufficient evidence that the business was "set up" based on the business transfer agreement and other activities.

FAQs:

1. Q: What was the main issue in this case?

A: The main issue was whether the assessee could deduct interest paid on ICDs against interest earned, and if the business was considered "set up" for tax purposes.

2. Q: Why did the court allow the deduction of interest paid?

A: The court allowed the deduction because there was a direct nexus between the interest paid and received, and the assessee had actually earned a small profit on the transaction.

3. Q: What evidence supported the claim that the business was "set up"?

A: The business transfer agreement, expenses incurred on staff, provision of performance bank guarantees, and advancement of funds for participatory interest in oil blocks supported this claim.

4. Q: What is the significance of Section 57 (of Income Tax Act, 1961) in this case?

A: Section 57 (of Income Tax Act, 1961) allows for deductions of expenses incurred to earn income from other sources. In this case, it permitted the deduction of interest paid to earn interest income.

5. Q: How did the cash flow statement impact the court's decision?

A: The cash flow statement helped prove that the funds used for various transactions were not solely from the ICDs, countering the Revenue's claims about fund diversion.

This appeal by Revenue under Section 260A (of Income Tax Act, 1961) (‘Act’ for short) in the case of M/s Jubilant Energy NELP-V- Private Limited ('respondent-assessee', for short)relates to the Assessment Year 2011-12 and arises from the order dated 28th June, 2018 passed by the Income Tax Appellate Tribunal (‘Tribunal’ for short).

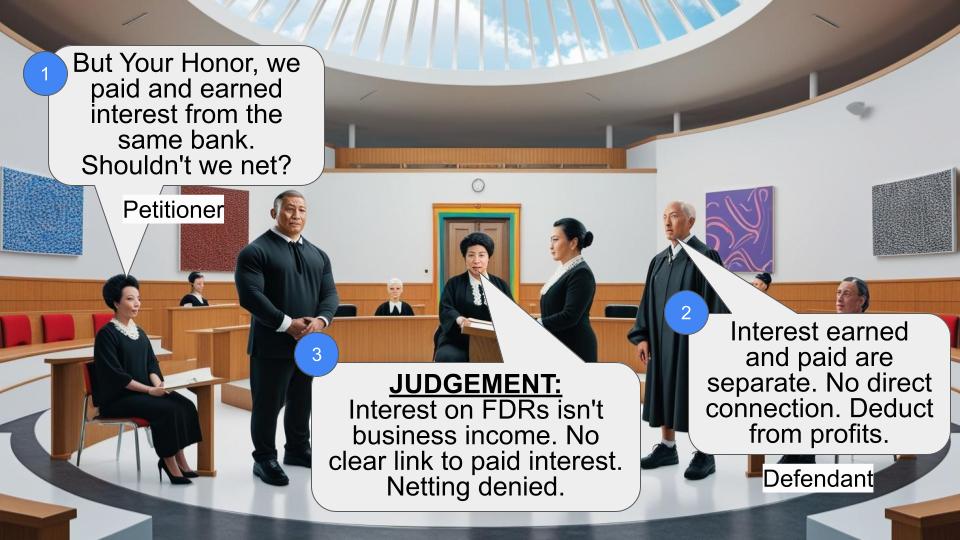

2. Revenue relying on the assessment order and the order of the Commissioner of Income Tax (Appeals), ('CIT (Appeals)', for short) submits that business of the respondent-assessee was not set up and was not ready for commencement. Respondent-assessee was incorporated on 13th March, 2007 for the purpose of carrying out business of exploration, development and production of oil and gas. In furtherance of this objective, the respondent-assessee had entered into a business transfer agreement with M/s Jubilant Capital Private Limited and M/s Jubilant Securities Private Limited for acquiring their 20% and 35% participatory interest in Ankleshwar Block and Golaghat Block, respectively. However, due to formalities and want of approvals, actual transfer of interest had not materialized. In the absence of business operations, interest of Rs. 1,88,98,763/- paid to a sister concern M/s Jubilant Energy (Kharsang) Private Limited was not allowable as a revenue expense and should be capitalized. Similarly, interest of Rs. 1,78,03,962/- on the Fixed Deposits Receipts ('FDRs', for short) in bank and Inter-Corporate Deposits ('ICDs', for short) with sister concerns earned by the respondent-assessee were taxable under the head 'income from other sources' and not as 'business income'. Interest of Rs. 1,78,03,962 /- cannot be deducted/set-off from interest paid at Rs. 1,88,98,763/-.

3. On the other hand, the respondent-assessee had stated that they had taken ICDs of Rs.55.30/- Crores at the interest rate of 12% per annum from M/s Jubilant Energy (Kharsang) Private Limited. Payments under the ICDs were received during the preceding year, except for Rs.15/- lacs, which was received between 5th April, 2010 and 4th May, 2010. ICDs were repaid to M/s Jubilant Energy (Kharsang) Private Limited between 31st May, 2010 to 25th March, 2011 leaving an outstanding balance of Rs.1 Crore at the end of the year in question. Rs.50 Crores received under the ICD's were advanced to M/s Jubilant Enpro Private Limited in the preceding year vide IDCs of Rs. 20 Crores on 10th October, 2009, Rs. 20 Crores on 29th October, 2009 and Rs. 10 Crores on 25th June, 2010, on which interest @ 12.5% per annum was paid. Thus, the respondent-assessee had paid interest @ 12% on the sum borrowed and had received interest @ 12.5 % on the money lent. M/s Jubilant Enpro Private Limited had repaid Rs. 50 crores between 28th May, 2010 to 25th June, 2010. Rs. 50 Crores was repaid was on the same day to M/s Jubilant Energy (Kharsang) Private Limited.

4. Respondent-assessee had relied on the cash flow statement, and cash and ledger account of advances which had opening balance of more than Rs.6.85/-Crores as on 1st March, 2011, which amount it was stated was advanced to M/s Jubilant Capital Private Limited in the period relevant to the Assessment Year 2008-09. The amount advanced to M/s Jubilant Capital Private Limited was not from the funds procured by the respondent-assessee under the ICDs.

5. As per the respondent-assessee, additional sum of money of Rs.5.20 Crores advanced to M/s Jubilant Capital Private Limited on 25th March, 2011 was paid/advanced from FDRs made in the earlier years and from reserves and surplus from share capital and share premium. On 25th March, 2011 the outstanding balance of loan from Jubilant Energy (Kharsang) Private Limited was Rs. 1 Crore only. Thus, the finding of the Assessing Officer that interest bearing funds were diverted as non-interest bearing funds to M/s Jubilant Capital Private Limited was factually incorrect.

6. The Tribunal after referring to the submissions, which rely on documents and papers, had agreed and accepted that the money received by the respondent-assessee under the ICDs of Rs. 55.30 Crores was in the preceding year. Rs. 50 Crores was thereafter transferred and given as ICDs to M/s Jubilant Enpro Private Limited also in the preceding year. There was a nexus between the interest paid @ 12 % per annum and the interest received @ 12.5% per annum. In fact, the respondent-assessee had earned interest of half percent. Even if the interest received was taxable under the head 'income from other sources', the interest paid was deductable under section 57 (of Income Tax Act, 1961).

7. We have not been shown any infirmity in the said findings, which are based on facts asserted by the respondent-assessee and accepted. Papers and documents referred to in the impugned order, have not been filed before us to show any incongruity and perversity in the factual and consequently in the legal finding. Accordingly, we do not think that the Assessing Officer and the First Appellate Authority were justified in not allowing deduction of the interest paid from interest received.

8. The Tribunal, after recording the above findings, had referred to the original business transfer agreement between the respondent-assessee and M/s Jubilant Capital Private Limited and M/s Jubilant Securities Private Limited. It was observed that the respondent-assessee had incurred expenses of more than Rs.2,00,000/- on operations and support staff etc. The Tribunal has opined that the business had commenced as the respondent-assessee had entered into business transfer agreement dated 1st April, 2007. It could be urged that this finding is not detailed, albeit the respondent-assessee had furnished performance bank guarantee for M/s Jubilant Capital Private Limited and M/s Jubilant Services Private Limited. Thus, the performance guarantees for the two blocks were given by the respondent- assessee. Interest earned on the FDRs obtained to procure the performance bank guarantees was connected with the two oil blocks. The Tribunal has mentioned that the Commissioner of Income Tax (Appeals) had allowed deduction under Section 35D (of Income Tax Act, 1961), thereby indirectly accepting that respondent-assessee had commenced business. Further the respondent-assessee had advanced more than Rs.12.11 Crores to M/s Jubilant Capital Private Limited in furtherance to the business transfer agreement to meet the cash calls for participatory interest in the Ankleshwar Block. Thus, the finding that the business was ‘set up’ has sufficient backing and support from the material and evidence referred to in the impugned order. In any case, this objection regarding 'commencement of business' loses much significance and importance in view of the direct nexus between interest paid and interest received on ICDs. Interest paid to earn interest has to be allowed as a deduction under Section 57 (of Income Tax Act, 1961).

9. In the above background, we are not inclined to issue notice in the present appeal. Appeal is dismissed.

SANJIV KHANNA, J.

ANUP JAIRAM BHAMBHANI, J.

DECEMBER 12, 2018

×

Similar Ripples

Questions

Court Allows Interest Deduction for Company's Interlinked Transactions

Write your CommentSimilar Posts

Generic

- Reportdata/1018_0WfcgpR.pdf