Court Dismisses Income Tax Appeal on Share Application Amounts

Full News

Court Dismisses Income Tax Appeal on Share Application Amounts

Court Dismisses Income Tax Appeal on Share Application Amounts

This case involves an appeal by the Commissioner of Income Tax against a taxpayer (Vikas Oberoi) regarding the treatment of share application amounts received by companies. The Income Tax Appellate Tribunal had previously ruled in favor of the taxpayer, and the High Court dismissed the appeal, upholding the Tribunal’s decision.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax VS Vikas Oberoi (High Court of Bombay)

Income Tax Appeal No. 84, 86, 87 & 366 of 2014

Date: 8th June 2016

Key Takeaways:

- The court found no substantial question of law in the appeal.

- The decision reinforces the interpretation that share application amounts may not always be considered as loans or advances under Section 2(22e) (of Income Tax Act, 1961).

- The court’s dismissal of the appeal suggests a consistent approach in similar cases.

Issue:

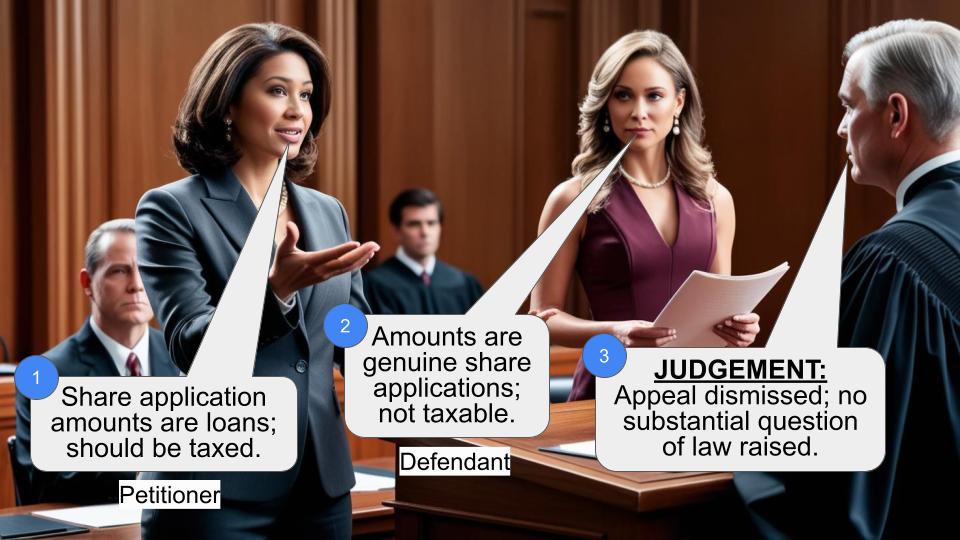

The main issue was whether the amounts received as share applications by companies, in which the respondent-assessee (Vikas Oberoi) has a beneficial interest, should be considered as loans and advances for the purpose of Section 2(22e) (of Income Tax Act, 1961).

Facts:

- The case relates to Assessment Years 2002-03, 2004-05, 2005-06, and 2007-08.

- The Income Tax Appellate Tribunal had previously ruled in favor of the assessee (Vikas Oberoi).

- The Commissioner of Income Tax filed an appeal under Section 260A (of Income Tax Act, 1961).

- A similar case for the Assessment Year 2006-07 (Income Tax Appeal No. 2479 of 2013) had been decided earlier on the same day.

Arguments:

While the judgment doesn’t explicitly state the arguments, we can infer:

- The Income Tax Department likely argued that the share application amounts should be treated as loans and advances, making them taxable under Section 2(22e) (of Income Tax Act, 1961).

- The assessee (Vikas Oberoi) probably contended that these amounts were genuine share applications and shouldn’t be considered loans or advances for tax purposes.

Key Legal Precedents:

The judgment doesn’t mention specific legal precedents. However, it refers to a decision made on the same day in a similar case:

- Income Tax Appeal No. 2479 of 2013, concerning the same respondent-assessee for the Assessment Year 2006-07

This suggests that the court relied on its own recent decision in a similar matter involving the same taxpayer.

Judgement:

- The court dismissed the appeal for all four assessment years.

- The judges determined that the question raised did not give rise to any substantial question of law.

- The court based its decision on the reasons provided in the order passed on the same day in Income Tax Appeal No. 2479 of 2013.

- No order was made regarding costs.

FAQs:

Q: What was the main issue in this case?

A: The main issue was whether share application amounts received by companies should be treated as loans and advances for tax purposes under Section 2(22e) (of Income Tax Act, 1961).

Q: Why did the court dismiss the appeal?

A: The court found that the question raised didn’t constitute a substantial question of law, based on a similar decision made on the same day in a related case.

Q: What is the significance of Section 2(22e) (of Income Tax Act, 1961)?

A: Section 2(22e) (of Income Tax Act, 1961) deals with the definition of dividends and includes certain payments or distributions to shareholders that are treated as dividends for tax purposes.

Q: Does this judgment set a precedent for future cases?

A: While it may not set a new precedent, it reinforces the court’s approach to similar issues and may be referred to in future cases dealing with the treatment of share application amounts.

Q: What does this decision mean for taxpayers?

A: This decision suggests that genuine share application amounts may not be automatically treated as loans or advances for tax purposes, which could be beneficial for taxpayers in similar situations.

1. This Appeal under Section 260 (of Income Tax Act, 1961)A of the Income Tax Act, 1961 (the Act) challenges the order dated 20th March, 2013 passed by the Income Tax Appellate Tribunal (the Tribunal) relating to Assessment Years 2002-03, 2004-05, 2005-06 and 2007-08.

2. This appeal raises the following common question of law in respect of all the four Assessment Years for our consideration :

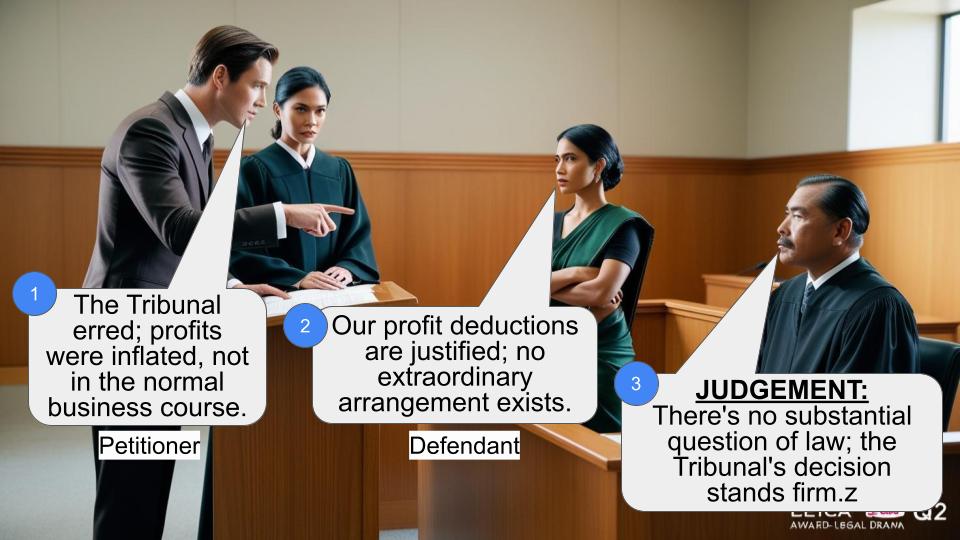

(i) Whether on the facts and circumstances of the case and in law, the Tribunal was justified in holding that the amounts received as share application by companies from companies in both of which the respondent assessee has beneficial interest, is not loans and advances for the purposes of invoking Section 2(22e) (of Income Tax Act, 1961) ?

3. We have today passed an order in respect of the same respondentassessee for A. Y. 200607 in Income Tax Appeal No.2479 of 2013 in respect of question no.(i) therein, which is identical to the question proposed for our consideration herein. It is further agreed between the parties that for the reasons indicated in the order passed today with regard to the aforesaid question in Income Tax Appeal No.2479 of 2013, the question as formulated would not give rise to any substantial question of law. Accordingly, question as proposed is not entertained.

4. All the four appeals are dismissed. No order as to costs.

(A.K. MENON, J.) (M.S. SANKLECHA, J.)

×

Similar Ripples

Questions

Court Dismisses Income Tax Appeal on Share Application Amounts

Write your CommentSimilar Posts

Generic

- Reportdata/2790.pdf