Full News

Court dismisses Revenue's appeal due to low monetary limit and lack of substantial questions of law.

Court dismisses Revenue's appeal due to low monetary limit and lack of substantial questions of law.

The case involves the Revenue's appeal against the Income Tax Appellate Tribunal's (ITAT) decision to dismiss their appeal on the grounds of low monetary limit. The Tribunal's decision was based on CBDT Circular 3/2011, which sets a threshold for appeals. The High Court upheld the Tribunal's decision, noting the absence of any substantial questions of law and the lack of documentation regarding a Revenue Audit Objection.

Get the full picture - access the original judgement of the court order here.

Case Name:

Commissioner of Income Tax vs. Shanthinath Benefit Fund Ltd. (High Court of Madras)

T.C.A. No. 1047 of 2014

Date: 7th January 2025

Key Takeaways

- The ITAT dismissed the Revenue's appeal due to the low monetary limit as per CBDT Circular 3/2011.

- The High Court upheld the ITAT's decision, emphasizing the absence of substantial questions of law.

- The case highlights the importance of adhering to procedural thresholds and the necessity of proper documentation in appeals.

Issue

Whether the Tribunal was correct in dismissing the Revenue's appeal on the grounds of low monetary limit, especially in the absence of substantial questions of law and proper documentation of a Revenue Audit Objection.

Facts

- The assessee filed a return of income, which was processed and later scrutinized by the Assessing Officer (AO).

- The AO found that the company had paid excess remuneration to its directors, which was added back to the income.

- The assessee appealed to the CIT (Appeals), who deleted the addition.

- The Revenue then appealed to the ITAT, which dismissed the appeal based on the low monetary limit set by CBDT Circular 3/2011.

- The Revenue further appealed to the High Court, arguing that the case fell under an exception in the CBDT Circular due to a Revenue Audit Objection.

Arguments

- Revenue's Argument:

The case should be considered under sub-clause (c) of clause 8 of CBDT Circular 3/2011, which allows appeals despite low monetary limits if there is a Revenue Audit Objection.

- Assessee's Argument:

The ITAT correctly dismissed the appeal based on the low monetary limit, and there was no substantial question of law.

Key Legal Precedents

- CBDT Circular 3/2011:

Sets monetary limits for appeals and outlines exceptions, including cases with Revenue Audit Objections.

- Section 198 (of Income Tax Act, 1961) r/w 309 and Schedule XIII of the Companies Act:

Prescribes limits for director remuneration, which was central to the AO's addition.

Judgement

The High Court dismissed the Revenue's appeal, agreeing with the ITAT that the appeal was not maintainable due to the low monetary limit. The court noted the absence of any substantial questions of law and the lack of documentation regarding the Revenue Audit Objection.

FAQs

Q1: What was the main reason for dismissing the Revenue's appeal?

A1: The main reason was the low monetary limit as per CBDT Circular 3/2011, and the absence of substantial questions of law.

Q2: What is CBDT Circular 3/2011?

A2: It is a circular issued by the Central Board of Direct Taxes that sets monetary thresholds for filing appeals and outlines exceptions.

Q3: Why was the Revenue Audit Objection not considered?

A3: There was no documentation provided to support the existence of a Revenue Audit Objection.

Q4: What does this decision mean for future cases?

A4: It underscores the importance of adhering to procedural thresholds and ensuring proper documentation when filing appeals.

Q5: Who won the case?

A5: The assessee, Shanthinath Benefit Fund Ltd., as the High Court upheld the ITAT's decision to dismiss the Revenue's appeal.

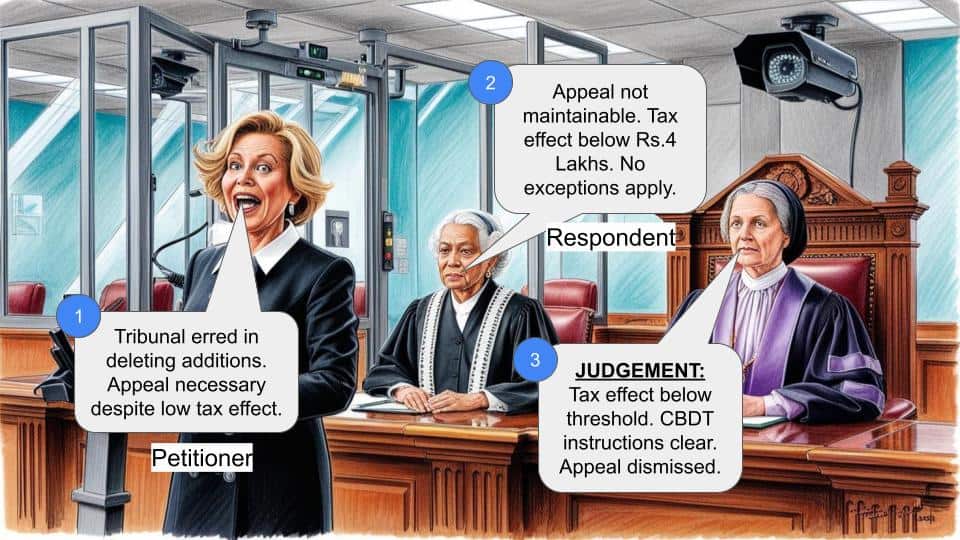

Aggrieved by the order passed by the Income Tax Appellate Tribunal in dismissing the appeal filed by it, the Revenue is before this Court by filing the present appeal, raising the following questions of law :-

“1) Whether it is proper for the Tribunal to dismiss the appeal of the

department without going into the merits of the case on the ground of low monetary limit especially when there was a revenue audit objection?

2) Whether it is proper for the Tribunal to dismiss the appeal of the

department on the ground that CBDT Circular No.3 of 2011 dated 9.2.2011 in paragraph 8 clearly mention the exception which was not considered while dismissing the appeal?

3) Whether the sitting fee amount of Rs.2,52,000/= being the excess

remuneration paid to the Director over and above the limits prescribed under the Companies Act are allowable?

4) Whether as per Section 198 (of Income Tax Act, 1961) r/w 309 and Schedule XIII of the Companies

Act which prescribes limit for paying remuneration by way of salary is to be followed or assessee is entitled to more than the limits prescribed therein?

5) Whether in Schedule XIII of the Companies Act, the remuneration has

been defined would include the Director's sitting fee also?”

2. The assessee, in the course of normal business, filed return of income on 24.11.03,which was processed under Section 143(1) (of Income Tax Act, 1961) on 6.12.03. A notice was issued under Section 143(2) (of Income Tax Act, 1961) on 15.2.06 to which the assessee filed its response. The

assessment was completed and the Assessing Officer found that during the year ending 31.3.05, the company had paid excess payment towards remuneration. Therefore, the Assessing Officer held that according to Schedule XIII of the Companies Act, remuneration would include any other allowance and, therefore, would cover sitting fees as well and,

therefore, while allowing the amount, the same was added as income by the Assessing Officer.

3. Aggrieved against the said order of the Assessing Officer, the assessee/respondent filed appeal before the CIT (Appeals), who allowed the appeal of the assessee and deleted the addition of Rs.2,52,000/= made by the Assessing Officer.

4. The Revenue, aggrieved by the order of the CIT (Appeals), dated 7.1.11, on the reopening done for the assessment year in question, i.e., 2003-2004, by which the CIT (Appeals) held that the addition is not valid and, thereby deleted the addition of Rs.2,52,000/= made by the Assessing Officer by disallowing the claim of remuneration paid to the Directors,filed appeal before the Tribunal. The Tribunal, in para 2 of its order, has categorically held that even if the reopening is held to be valid, the addition effected by the Assessing Officer is only

Rs.2,52,000/=, which is much less than Rs.3 Lakhs and the tax component is well below Rs.2 Lakhs and, placing reliance upon CBDT Circular No.3 of 2008 dated 9.2.11, held that the appeal is not maintainable. For better clarity, para-2 of the order passed by the Tribunal, is extracted

hereinbelow :-

“2. It is clear from the grounds itself that even if the reopening is held to be valid, the addition effected by the A.O. being only Rs.2,52,000/= the tax effect is much less than Rs.3 Lakhs and even well below Rs.2 Lakhs. Therefore, in view of CBDT Circular No.3 of 2008 dated 9.2.2011, the appeal is not maintainable.”

Aggrieved by the said order of the Tribunal, the Revenue is before this Court by filing the present appeal.

5. It is the primary contention of Mr.Ravikumar, learned standing counsel appearing forthe appellant/Revenue that the case will fall under sub-clause (c) of clause 8 of the CBDT Circular 3/2011 dated 9.2.2011. For better appreciation, sub-clause (c) of clause 8 of the CBDT

Circular 3/2011 dated 9.2.2011, is extracted hereunder :-

“8. Adverse judgments relating to the following issues should be contested on merits notwithstanding that the tax effect entailed is less than the monetary limits specified in para 3 above or there is no tax effect.

(a) Where the Constitutional validity of the provisions of an Act or Rule are under challenge, or

(b) Whete Board's order, Notification, Instruction or Circular has been held to be illegal or ultra vires, or

(c) Where Revenue Audit Objection in the case has been accepted by the

Department.”

6. It is the contention of Mr.Ravikumar that there being a Revenue Audit Objection insofar as the particular transaction is concerned, the same would fall well within sub-clause (c) of clause 8 of the CBDT Circular 3/2011 dated 9.2.2011. However, we find that there is no document relating to Revenue Audit Objection available in the typed set of documents filed along with this appeal. It is also evident from the order passed by the Tribunal that there is no reference to any document filed by the Department, before the Tribunal, insofar as Revenue

Audit Objection in relation to the said transaction is concerned. In such view of the matter,this Court is in agreement with the view taken by the Tribunal that CBDT Circular 3/2011 dated 9.2.2011 will come into play and, therefore, the dismissal of the appeal is entirely justified. No question of law, much less substantial questions of law arise for consideration in this appeal.

7. For the reasons aforestated, finding no infirmity with the order passed by the Tribunal warranting interference, this appeal fails and the same is dismissed.

(R.S.J.) (R.K.J.)

07.01.2015

Index : Yes/No

Internet : Yes/No

To

1. The Commissioner of Income Tax

Chennai.

2. The Income Tax Appellate Tribunal

Madras 'B' Bench

Chennai.

R.SUDHAKAR, J.

AND

R.KARUPPIAH, J.

×

Similar Ripples

Questions

Court dismisses Revenue's appeal due to low monetary limit and lack of substantial questions of law.

Write your CommentSimilar Posts

Generic

- Reportdata/4160.pdf