Full News

Court dismisses Revenue's appeal on settled issue, warns against frivolous appeals.

Court dismisses Revenue's appeal on settled issue, warns against frivolous appeals.

The High Court dismissed an appeal by the Revenue challenging an order by the Income Tax Appellate Tribunal. The court found that the issue had already been settled by previous decisions, including the case of "CIT v/s. Geoffrey Manners and Co. Ltd." The court criticized the Revenue for filing appeals on issues already decided and warned of imposing costs on officers responsible for such actions.

Get the full picture - access the original judgement of the court order here.

Case Name:

Commissioner of Income Tax vs. Proctor & Gamble Home Products Ltd. (High Court of Bombay)

Income Tax Appeal No. 37 of 2013

Key Takeaways

- The court dismissed the Revenue's appeal because the issue had already been settled by previous decisions.

- The court criticized the Revenue for filing appeals on issues that have already been decided, calling it a waste of public resources.

- The court warned that future frivolous appeals could result in heavy costs imposed on the responsible officers.

Issue

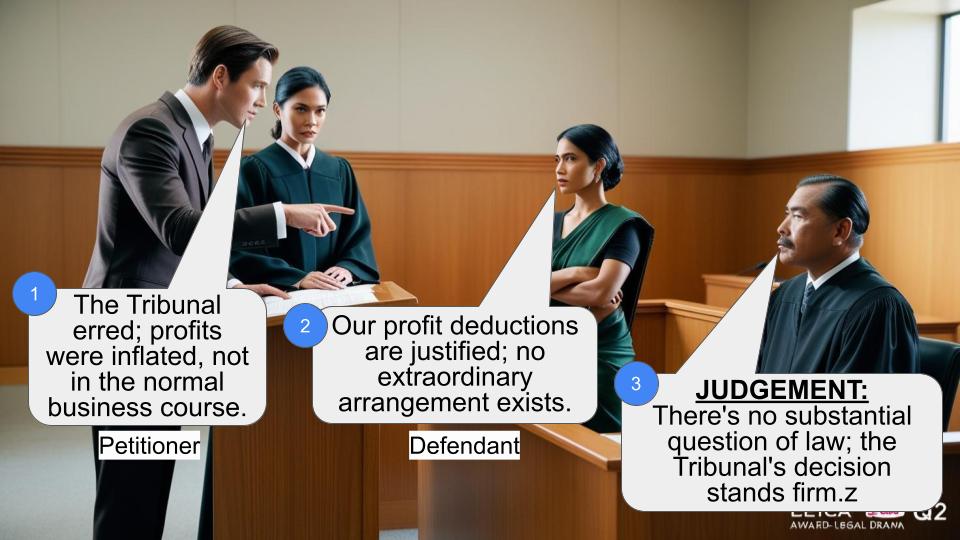

Whether the Tribunal was justified in holding the expenditure for producing TV films and commercials as revenue in nature, despite the Revenue's claim that these are assets reusable over an indefinite period.

Facts

- The Revenue filed an appeal under Section 260A (of Income Tax Act, 1961), challenging the Tribunal's order dated October 5, 2011.

- The Tribunal had dismissed the Revenue's appeal, citing that the issue was already settled by the High Court in "CIT v/s. Geoffrey Manners and Co. Ltd."

- The Revenue persisted with the appeal despite the issue being previously concluded in favor of the Respondent Assessee.

Arguments

- Revenue's Argument:

The expenditure for producing TV films and commercials should be considered as capital expenditure because these are assets reusable over an indefinite period.

- Respondent's Argument:

The issue has already been settled by the High Court in previous cases, and the Tribunal's decision should be upheld.

Key Legal Precedents

- CIT v/s. Geoffrey Manners and Co. Ltd. 315 ITR 134:

This case established that the expenditure for producing TV films and commercials is revenue in nature.

- Income Tax Appeal Nos. 202 of 2011, 1321 of 2011, and 1322 of 2011:

Previous appeals on identical issues were dismissed by the High Court.

Judgement

The court dismissed the Revenue's appeal, stating that no substantial question of law arises as the issue had already been settled by previous decisions. The court also criticized the Revenue for filing appeals on settled issues and warned of imposing costs on responsible officers if such actions continue.

FAQs

Q1: Why was the Revenue's appeal dismissed?

A1: The appeal was dismissed because the issue had already been settled by previous decisions of the High Court.

Q2: What was the main issue in this case?

A2: The main issue was whether the expenditure for producing TV films and commercials should be considered as revenue or capital in nature.

Q3: What did the court say about the Revenue's practice of filing appeals on settled issues?

A3: The court criticized the Revenue for filing appeals on issues that have already been decided, calling it a waste of public resources and warned of imposing costs on responsible officers.

Q4: What are the implications of this judgment for future cases?

A4: The judgment implies that the Revenue should review and withdraw appeals on issues already settled by the High Court to avoid unnecessary expenditure and anxiety for the assessee.

Q5: What should the Revenue do before filing new appeals?

A5: The Revenue should examine whether the decision of the jurisdictional High Court being relied upon by the Tribunal is subject to challenge before the Apex Court or is otherwise distinguishable, and this must be indicated in the appeal memo.

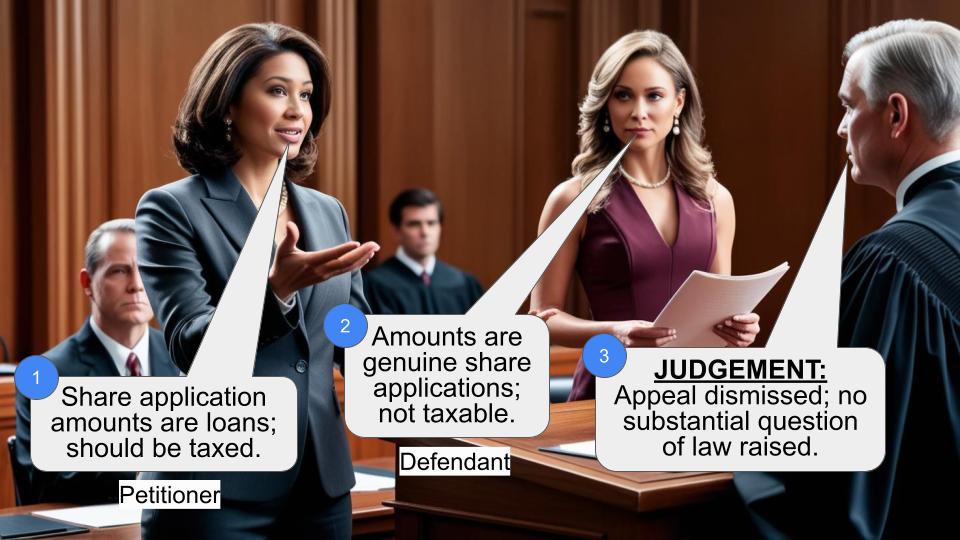

1. This appeal by the Revenue under Section 260 (of Income Tax Act, 1961)A of the Income Tax Act, 1961 (the Act), challenges the order dated 5th October, 2011 passed by the Income Tax Appellate Tribunal (the Tribunal).

2. The following question of law has been raised for our consideration:

“ Whether on the facts and in the circumstances of the case and in law, the Tribunal is justified in holding the expenditure of Rs.6,43,47,284/ incurred for production of T. V. films and commercials as revenue in nature, without appreciating the fact that the advertisement films are assets which are owned by the assessee and are reusable over an indefinite period of time?”

3. The Tribunal by the impugned order dated 5th October, 2011 dismissed the Revenue's appeal on the ground that the issue arising in the present case is covered against the Revenue by the decision of this Court in CIT v/s. Geoffrey Manners and Co. Ltd. 315 ITR 134. We find that even for the earlier Assessment Years 199798, 200203 and 200304, the appeal of the Revenue on an identical issue from the orders of the Tribunal were dismissed by this Court in Income Tax Appeal Nos.202 of 2011 on 4th July, 2012, Income Tax Appeal (L) No.1321 of 2011 and Income Tax Appeal (L) No.1322 of 2011 on 12th March, 2013.

4. In spite of the issue being covered by the decision of this Court in Geoffrey Manners and Co. Ltd. (supra) as well as by the order dated 4th July, 2012 in Income Tax Appeal No.202 of 2011 in respect of Assessment Year 199798, the Revenue has chosen to persist with this Appeal. However, not only the appeal memo does not indicate any reason why the Revenue is seeking to appeal against order which already stands concluded in favour of the RespondentAssessee but even today they are unable to explain.

5. In view of the fact that the issue being challenged in the impugned order stands concluded by the decision of this Court, no substantial question of law arises. Therefore, Appeal is dismissed.

6. However, before parting, it needs to be pointed out that we have noticed that the Revenue has been preferring appeals from the orders of the Tribunal even where the issue stands concluded by the orders of this High Court. These appeals are filed by the Revenue in a very causal manner without indicating the basis of the challenge i.e. some distinction in facts from the order of the High Court or that the order of the jurisdictional High Court is a subject matter of challenge before the Apex Court. In the absence of the above explanation, it follows that there are times when even though the decision of the jurisdictional High Court has been accepted by the Revenue and yet the Revenue chooses to file an appeal on the same issue before this Court. Rule of law implies certainty of law and the State filing appeals on settled issues arbitrarily and/or without any application of mind. This filing of appeal without due application of mind leads to attempting to unsettle settled position without reasons. This casual manner of filing appeals subjects an assessee to unnecessary expenditure and at times anxiety. Even the Revenue incurs substantial expenses in pursuing unwarranted cases,which are a sheer waste of public money. The least that the Revenue should do is to examine whether or not the decision of the jurisdictional High Court being relied upon by the Tribunal, is subject matter of challenge before the Apex Court or is otherwise distinguishable and the same must be indicated in the appeal memo.

7. In the above view, we were contemplating to impose costs on the Revenue. However, we noticed that on earlier occasion when costs were imposed on the Revenue, it seemed to matter little to the Officers, for after all the amount came out of the general pool of tax paid by the tax payers. In the circumstances, we are now putting the Officers of the Revenue to notice, that in all cases including where appeals are filed, the Offices instructing the Counsel would review whether the appeal should at all be pressed in view of the Revenue having accepted the jurisdictional High Court's order on an identical issue and take necessary instructions from the Commissioner of Income Tax to withdraw and/or not press the appeal. Alternatively, in case a conscious decision is taken to press the appeal, then an averment to the effect that either the case is distinguishable or an appeal has been preferred from the decision of this Court to the Apex Court if not averred in the appeal memo, then a further affidavit in support be filed indicating the reasons. In the absence of the above, we will be compelled to impose heavy/exemplary costs to be personally paid by the jurisdictional – Commissioner of Income Tax under whose jurisdiction, the appeal is being filed and pressed in spite of the issue being settled by this Court and the same having been accepted by the Revenue.

8. It is expected of the Revenue that in the light of the above observations it would review all the appeals which are already filed and where the issue stands concluded by virtue of decision of this Court which has been accepted by the Revenue, withdraw such appeals. Needless to state that above examination will also be done in case of new appeals under Section 260A (of Income Tax Act, 1961) before filing them.

9. With the above observations/directions, Appeal is dismissed. No order as to costs.

10. A copy of this order be communicated by the Office and the Counsel for the Revenue to the Chief Commissioner of Income Tax, Mumbai and the Central Board of Direct Taxes for necessary action.

(G.S.KULKARNI,J.) (M.S.SANKLECHA,J.)

×

Similar Ripples

Questions

Court dismisses Revenue's appeal on settled issue, warns against frivolous appeals.

Write your CommentSimilar Posts

Generic

- Reportdata/4105.pdf