Court Dismisses Tax Appeal: No Link Between Assessee and Cash Deposit

Full News

Court Dismisses Tax Appeal: No Link Between Assessee and Cash Deposit

Court Dismisses Tax Appeal: No Link Between Assessee and Cash Deposit

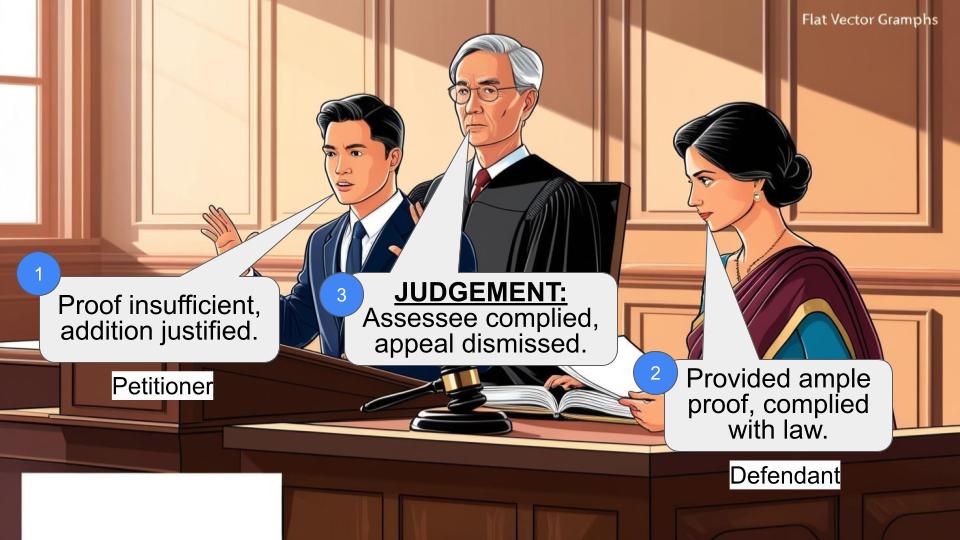

This case involves an appeal by the Revenue (tax authorities) against a decision made by the Income Tax Appellate Tribunal (ITAT) in favor of the assessee, Real Time Marketing (P) Ltd. The dispute centered around an addition made by the Assessing Officer under Section 68 (of Income Tax Act, 1961), treating an unsecured loan as unexplained cash credit. The High Court dismissed the Revenue's appeal, upholding the ITAT's decision that there was no material to link the assessee with the cash deposit in question.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs Real Time Marketing (P) Ltd. (High Court of Delhi)

TA No.551/2007

Date: 7th April 2008

Key Takeaways:

1. The court emphasized the importance of concrete evidence in linking an assessee to unexplained cash deposits.

2. Concurrent findings of fact by lower appellate authorities carry significant weight in higher courts.

3. The burden of proof lies on the assessee to prove the identity, capacity, and genuineness of a transaction, but once discharged, the onus shifts to the tax department to disprove it.

Issue:

Was the Income Tax Appellate Tribunal correct in holding that there was no material to link the assessee (Real Time Marketing (P) Ltd.) with the sum of Rs.29,97,000 deposited in cash in the bank account of M/s. FBSL, thus not justifying an addition under Section 68 (of Income Tax Act, 1961)?

Facts:

Let's break this down in a conversational manner:

1. The assessee, Real Time Marketing (P) Ltd., is a private limited company.

2. During the relevant financial year, they took an unsecured loan of Rs. 25 lacs from Aishwaray Capital Lease Finance Pvt. Ltd. (ACL).

3. The Assessing Officer noticed a series of internal transfers on March 28, 2001:

- Rs. 22,97,000 was deposited in cash into the account of Fair Business Security and Leasing Pvt. Ltd. (FBSL).

- This money was then transferred to Breeze Trade Links Pvt. Ltd. (BTL).

- BTL transferred it to ACL.

- Finally, ACL transferred Rs. 25 lacs to the assessee.

4. Interestingly, all these companies shared the same address in New Delhi.

5. No interest was charged on these transfers.

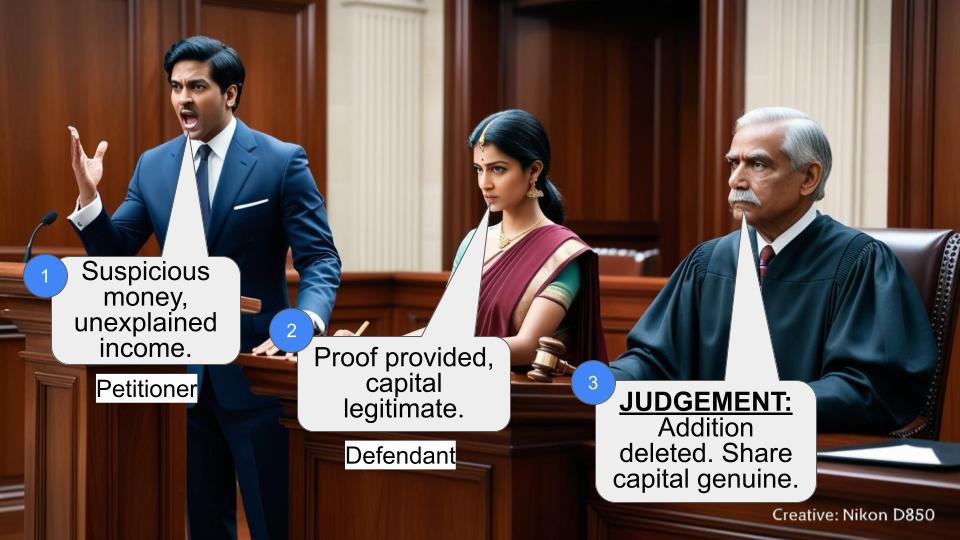

The Assessing Officer smelled something fishy and thought this might be the assessee's own money being routed back as a loan to evade tax.

Arguments:

The Revenue (tax department) argued:

1. The assessee used a circular route to receive its own money as a loan.

2. This was a device to evade tax, and the amount should be taxable under Section 68 (of Income Tax Act, 1961).

The Assessee contended:

1. They had provided confirmation from ACL about the loan.

2. The cash deposited by FBSL was not their money but from FBSL's own books.

3. They had discharged their burden of proving the identity, capacity, and genuineness of the transaction.

Key Legal Precedents:

While no specific legal precedents were cited in this judgment, the court relied on the principle that concurrent findings of fact by lower appellate authorities should not be disturbed unless there's a substantial question of law involved.

Judgement:

The High Court dismissed the Revenue's appeal. Here's why:

1. Both the CIT(A) and the ITAT had concurrently found that there was no material linking the assessee to the cash deposit of Rs. 22,97,000 in FBSL's account.

2. The assessee had discharged its burden of proving the identity, capacity, and genuineness of the transaction.

3. The Assessing Officer hadn't brought any material to show that the funds to ACL were provided by the assessee.

4. The court found no infirmity or perversity in the ITAT's order.

5. As no substantial question of law arose, the appeal was not maintainable.

FAQs:

Q1: What is Section 68 (of Income Tax Act, 1961)?

A1: Section 68 (of Income Tax Act, 1961) deals with unexplained cash credits. If an assessee can't satisfactorily explain the source and nature of a credit in their books, it can be treated as income and taxed.

Q2: Why didn't the court agree with the Assessing Officer's view?

A2: The court relied on the findings of the CIT(A) and ITAT, which both concluded there was no concrete evidence linking the assessee to the cash deposit.

Q3: What's the significance of "concurrent findings of fact"?

A3: When two lower appellate authorities agree on the facts of a case, higher courts generally don't interfere unless there's a clear error or a substantial question of law involved.

Q4: Could the outcome have been different if the Assessing Officer had more evidence?

A4: Possibly. If the Assessing Officer had concrete evidence linking the assessee to the cash deposit, or had investigated further by issuing summons to the involved companies, the outcome might have been different.

Q5: What lesson can taxpayers learn from this case?

A5: It's crucial to maintain proper documentation and be able to prove the genuineness of transactions, especially when dealing with unsecured loans or transactions involving multiple related parties.

The Revenue has filed the present appeal under Section 260A (of Income Tax Act, 1961) (for short as ‘Act’) against order dated 15th September, 2006 passed by the Income Tax Appellate Tribunal (herein after referred as ‘Tribunal’) Delhi Bench ‘A’ in ITA No.2574 (Del)/2004 relevant for the assessment year 2001-02. The Tribunal in its order held that there is absolutely no material to link the Assessee with the sum of Rs.29,97,000/- deposited in cash in the bank account of M/s. FBSL.

2. The facts of this case are that the Assessee is a Private Limited company. During the previous year, it had taken an unsecured loan of Rs. 25 lacs from M/s. Aishwaray Capital Lease Finance Pvt. Ltd. (herein after referred to as ACL). The Assessing Officer asked the Assessee to file a copy of income tax return along with the audited profit and loss account and the balance sheet with annexures and copy of bank statement for the period ending 31st March, 2001 of M/s. ACL. The Assessee furnished the same accordingly. On perusal of the bank statement of M/s. ACL, the Assessing Officer noticed that the funds were transferred through internal transfer on 28th March, 2001 to M/s. ACL and then in the same manner in the bank account of the Assessee company. The Assessing Officer called for information from the bank under section 133(6) (of Income Tax Act, 1961) to locate the true nature of these internal transfer transactions and the exact source of funds. It was revealed on the information furnished by the bank;

(a) that on 28th March, 2001 cash of Rs.22,97,000/- was deposited in account no.4142 pertaining to M/s. Fair Business Security and Leasing Pvt. Ltd. (herein after referred to as FBSL)

(b) from this account no.4142 a sum of Rs.25 lacs was transferred to account no.4016, which stood in the name of M/s. Breeze Trade Links Pvt. Ltd. (herein after referred to as BTL) on the same day

(c) on the same day, Rs.25 lacs were transferred from account no.4016 to M/s. ACL, having account no.4144 and

(d) on same day, i.e. 28th March, 2001, Rs.25 lacs were transferred from account no.4144 from M/s. ACL to the Assessee.

3. The Assessing Officer also noticed that all the three companies referred to above had the same address, i.e. B-258, Naraina Industrial Area, Phase-I, New Delhi. Further, no interest was charged by any of these transferees. The Assessing Officer was thus of the view that the entire transaction was a sham transaction and asked the Assessee to show cause as to why cash deposit of Rs.22,97,000/- made into the account of M/s. FBSL be not added as the taxable income of the Assessee for the year under consideration. The Assessee submitted his reply and filed confirmation from M/s. ACL. The Assessee also submitted that the cash deposited by M/s. FBSL was

not its money and that it was from the books of the said company.

4. The Assessing Officer however, held that it was the Assessee’s money of Rs.22,97,000/- which was deposited in cash into the account of M/s. FBSL and the same was routed through different accounts and received as unsecured loan by the Assessee company and thus made an addition of Rs.25 lacs as unexplained cash credit under Section 68 (of Income Tax Act, 1961).

5. On appeal filed by the Assessee, the Commissioner of Income Tax (Appeals) (for short as ‘CIT[A]’) held that the Assessee had discharged its burden of proving the identity, capacity and genuineness of the transaction and in the circumstances the addition made by the Assessing Officer was not justified. It was also observed by the CIT(A) that the Assessing Officer had not chosen to issue summons to M/s. FBSL, M/s. ACL or M/s. BTL before coming to the conclusion that all the transactions were from and out of the money provided by the Assessee.

6. Being aggrieved by the order of CIT(A), the Revenue preferred an appeal before the Tribunal and vide impugned order the Tribunal dismissed the appeal of the Assessee.

7. It has been contended by learned counsel for the Revenue that the Assessee has used circular route to receive the loan in its account and the same is merely a device being used to evade tax and as such, loan is taxable under Section 68 (of Income Tax Act, 1961).

8. There is a finding of fact given by the two authorities namely CIT(A) and the Tribunal to the effect that:-

“The confirmation of M/s. ACL has been filed by the Assessee. The said company was assessed to tax. The source of ACL had been explained as out of transfer of funds from the accounts of M/s. BTL. Thus, the Assessee discharged its burden of proving identity, capacity and genuineness of the transaction. The Assessing Officer has not brought any material to show that the funds to ACL were provided by the Assessee. Under the circumstances, it cannot be said that the cash credit in question has remained unexplained. There is absolutely no material to link the Assessee with the sum of Rs.22,97,000/- deposited in cash in the bank account of M/s. FBSL.“

9. In view of the concurrent findings of the fact given by the two authorities that there is no material to link the Assessee with a sum of Rs.22,97,000/- deposited in cash in the bank account of M/s. FBSL, as such, no case is made out for making addition under Section 68 (of Income Tax Act, 1961), since there was no material with the Assessing Officer to come to the conclusion regarding any genuineness or fictitious identity of the entries or non capacity of the lender.

10. Under these circumstances, we do not find any infirmity or perversity in the order passed by the Tribunal and in our opinion no substantial question of law arises in this case. With the result, the present appeal is not maintainable and the same is hereby dismissed.

V. B. GUPTA

(JUDGE)

MADAN B. LOKUR

(JUDGE)

×

Questions

Court Dismisses Tax Appeal: No Link Between Assessee and Cash Deposit

Write your CommentSimilar Posts

Generic

- Reportdata/4679.pdf