Court Halts Reassessment Proceedings in Tax Dispute Over External Development C…

Full News

Court Halts Reassessment Proceedings in Tax Dispute Over External Development Charges

Court Halts Reassessment Proceedings in Tax Dispute Over External Development Charges

This case involves BPTP Limited challenging a reassessment notice issued by the Income Tax Department. The Delhi High Court found merit in the petitioner's arguments and ordered a stay on the reassessment proceedings pending the resolution of the case.

Get the full picture - access the original judgement of the court order here

Case Name:

BPTP Limited & Anr. Vs Principal Commissioner of Income Tax & Anr. (High Court of Delhi)

W.P.(C) 13803/2018 & CM Appl. 53873/2018 + W.P.(C) 13812/2018 & CM Appl. 53889/2018

Date: 20th December 2018

Key Takeaways

1. The court found prima facie merit in the assessee's arguments against the reassessment notice.

2. The case highlights the importance of proper application of mind by tax authorities when issuing notices.

3. The court's interim order protects the assessee from immediate adverse action while the case is pending.

Issue

Did the Income Tax Department err in issuing a reassessment notice that cited non-compliance with Section 194 (of Income Tax Act, 1961) (TDS on dividends) but discussed deductions related to external development charges?

Facts

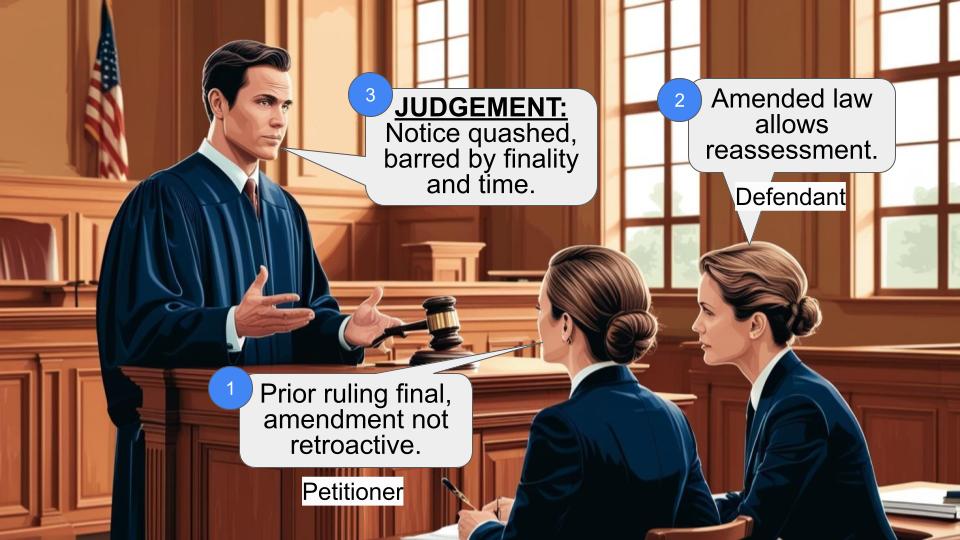

So, here's what happened. BPTP Limited received a reassessment notice from the Income Tax Department. Now, this notice was a bit confusing. It mentioned something about not following Section 194 (of Income Tax Act, 1961), which is all about deducting tax at source (TDS) on dividends. But then, out of nowhere, it started talking about deductions for external development charges.

BPTP Limited was like, "Wait a minute, what's going on here?" They felt that the tax department hadn't really thought this through before sending out the notice. So, they decided to take it to court.

Arguments

BPTP Limited's side of the story:

They said, "Look, this notice doesn't make sense. It's talking about dividend TDS and then suddenly jumps to external development charges. These charges are something we have to pay because of the law. The tax department clearly didn't think this through before sending us this notice."

The Tax Department's response:

Well, they didn't really get a chance to present their side in detail at this stage. The case was just getting started.

Key Legal Precedents

In this particular judgment, there weren't any specific legal precedents mentioned. The court was mainly looking at the facts of the case and the arguments presented by BPTP Limited.

Judgement

So, here's what the judges decided:

1. They thought BPTP Limited had a pretty good point about the reassessment notice not making sense.

2. The court said, "Okay, while we figure this out, let's put a pause on things."

3. They told the tax department, "Don't make any final decisions on this reassessment while we're looking into this case."

It's like the court is saying, "Hold up, let's take a closer look at this before anyone does anything they can't take back."

FAQs

1. Q: What exactly is a reassessment notice?

A: It's a notice sent by the tax department when they think they need to take a second look at someone's tax situation, usually because they suspect some income wasn't properly accounted for.

2. Q: Why did the court think BPTP Limited had a good argument?

A: The court felt that the reassessment notice didn't make much sense. It mentioned one thing (TDS on dividends) but then talked about something completely different (external development charges).

3. Q: What are external development charges?

A: These are charges that developers often have to pay for infrastructure development around their projects. The key point here is that these are required by law, not something optional.

4. Q: What does "prima facie" mean in this context?

A: It's a legal term that means "at first glance" or "based on first impressions." The court is saying that without digging too deep, BPTP's arguments seem to have merit.

5. Q: What happens next in this case?

A: The case will continue, but in the meantime, the tax department can't finalize any reassessment. It's like pressing a pause button on the tax proceedings until the court makes a final decision.

Issue notice. Mr. Ruchir Bhatia, counsel on behalf of the respondents

accepts notice.

The appellant’s grievance is that the impugned re-assessment notice

cites non-compliance of Section 194 (of Income Tax Act, 1961) (which deals with TDS on dividends)

and goes on to discuss deduction in respect of external development charges.

It is submitted that these charges are levied on account of statutory provision and the impugned notice, shows complete non-application of mind.

The Court is of the opinion that prima facie the assessee’s arguments

are sound and valid on the re-opening aspect.

In these circumstances, the respondents are directed not to pass any

final order in the re-assessment proceedings during the pendency of the

present case.

The copy of the order be given Dasti.

S. RAVINDRA BHAT, J

PRATEEK JALAN, J

DECEMBER 20, 2018

×

Similar Ripples

Questions

Court Halts Reassessment Proceedings in Tax Dispute Over External Development Charges

Write your CommentSimilar Posts

Generic

- Reportdata/5323.pdf