Court invalidates order under Section 158BD (of Income Tax Act, 1961) due to la…

Full News

Court invalidates order under Section 158BD (of Income Tax Act, 1961) due to lack of satisfaction note.

Court invalidates order under Section 158BD (of Income Tax Act, 1961) due to lack of satisfaction note.

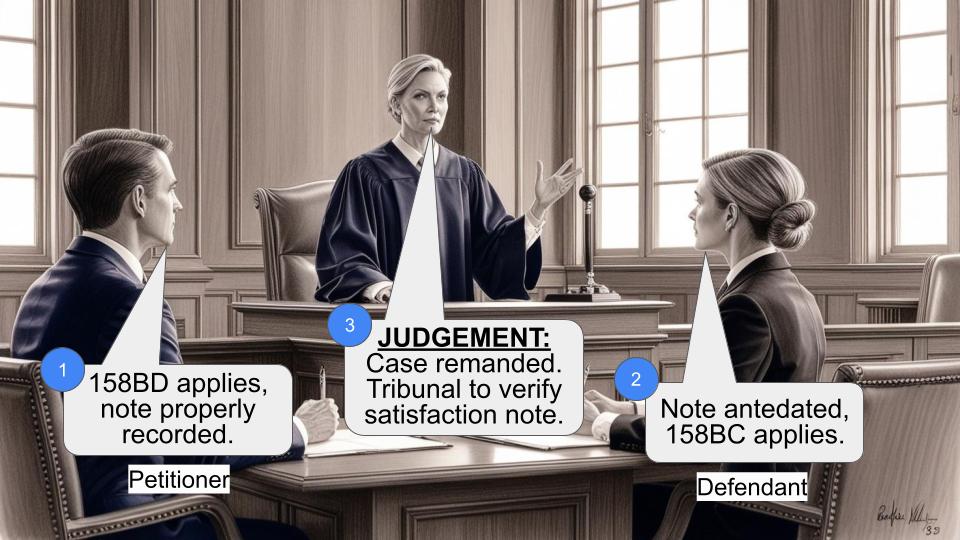

In this case, the court ruled that an order passed under Section 158BD (of Income Tax Act, 1961) is invalid if there is no satisfaction note from the Assessing Officer (AO) of the searched person indicating that any undisclosed income belongs to another person. The court dismissed the revenue's appeal, emphasizing the necessity of a proper satisfaction note.

Get the full picture - access the original judgement of the court order here.

Case Name:

Commissioner of Income Tax vs. Manoj Bansal (High Court of Delhi)

ITA 578/2008

Key Takeaways

- Satisfaction Note Requirement:

The court highlighted that a satisfaction note is essential for initiating proceedings under Section 158BD (of Income Tax Act, 1961).

- Invalidation of Orders:

Without a proper satisfaction note, any order passed under Section 158BD (of Income Tax Act, 1961) is considered invalid.

- Precedent Application:

The court applied the principles from the Supreme Court's judgment in CIT v. Calcutta Knitwear (2014) 362 ITR 673 (SC) and other relevant cases.

Issue

Is an order passed under Section 158BD (of Income Tax Act, 1961) valid without a satisfaction note from the AO of the searched person indicating that any undisclosed income belongs to another person?

Facts

- A search was conducted on Manoj Aggarwal's premises on August 3, 2000, leading to the seizure of various documents and materials.

- The AO of Manoj Aggarwal communicated to the AO of the respondent (Radhey Shayam Bansal) via a letter dated July 15, 2003, indicating that the respondent acted as a mediator for providing accommodation book entries.

- The letter mentioned evidence of cash received by Manoj Aggarwal from the respondent, but the annexures containing this evidence were not filed before the tribunal or produced in court.

Arguments

- Revenue's Argument:

The revenue contended that the letter dated July 15, 2003, constituted a valid satisfaction note under Section 158BD (of Income Tax Act, 1961).

- Respondent's Argument:

The respondent argued that the letter did not meet the requirements of a satisfaction note as it did not provide sufficient evidence or material to support the claim of undisclosed income.

Key Legal Precedents

- CIT v. Calcutta Knitwear (2014) 362 ITR 673 (SC):

This case established that a satisfaction note is a sine qua non for proceedings under Section 158BD (of Income Tax Act, 1961) and must be prepared before transmitting records to another AO.

- Manish Maheswari v. ACIT 2007 289 ITR 341 (SC):

This case was considered by the ITAT and affirmed by the court, emphasizing the necessity of compliance with Section 158BB (of Income Tax Act, 1961) requirements.

Judgement

The court dismissed the revenue's appeal, ruling that the absence of a proper satisfaction note invalidated the order under Section 158BD (of Income Tax Act, 1961). The court emphasized that the revenue failed to provide sufficient evidence or material to support the claim of undisclosed income, and thus, the prerequisite of "satisfaction" was non-existent.

FAQs

Q1: What is a satisfaction note?

A1: A satisfaction note is a written document by the AO of the searched person indicating that there is material evidence of undisclosed income belonging to another person, which is necessary for initiating proceedings under Section 158BD (of Income Tax Act, 1961).

Q2: Why was the order under Section 158BD (of Income Tax Act, 1961) invalidated?

A2: The order was invalidated because there was no proper satisfaction note from the AO of the searched person, which is a mandatory requirement under Section 158BD (of Income Tax Act, 1961).

Q3: What was the main legal precedent applied in this case?

A3: The main legal precedent applied was the Supreme Court's judgment in CIT v. Calcutta Knitwear (2014) 362 ITR 673 (SC), which emphasized the necessity of a satisfaction note for proceedings under Section 158BD (of Income Tax Act, 1961).

Q4: What does this judgment mean for future cases under Section 158BD (of Income Tax Act, 1961)?

A4: This judgment reinforces the requirement of a proper satisfaction note for initiating proceedings under Section 158BD (of Income Tax Act, 1961), ensuring that orders without such a note are considered invalid.

1. The present appeal has been received on limited remit by the Hon’ble

Supreme Court which had by its judgment and order reported as CIT V.

Calcutta Knitwear (2014) 362 ITR 673 (SC) directed examination of the

limited question as to whether opinion formation – in terms of Section

158BB of the Income Tax Act, and the time within which it had to be

recorded was complied with.

2. The facts of the case are that a search was conducted on 3.8.2000 in the premises of Sh. Manoj Aggarwal. This led to the seizure of various documents and other materials; even the statement was recorded under Section 132 (of Income Tax Act, 1961). The present assessees were issued with a notice on 22.03.2004 by his assessing officer. It was alleged by the revenue that the notice was on account of opinion formation in terms of Section 158BB (of Income Tax Act, 1961) of Sh. Manoj Aggarwal’s assessing officer. During the course of proceeding the matter ultimately reached the ITAT which after considering the submissions of the parties as far as the records of assessment, in the assessee’s case, held that the requirement of Section 158BB (of Income Tax Act, 1961) were not complied with in terms of the judgment of the Supreme Court cited as Manish Maheswari V. ACIT 2007 289 ITR 341 (SC). The order of the ITAT became the subject matter of challenge in ITA 582/2008. By judgment and order dated 30.5.2011, this Court affirmed the findings of the ITAT. While doing so, the judgment in Manish Maheswari (supra) was considered, and so too were the other decisions of the Surpeme Court. Thereafter the Court in para 17 discussed the letter/communication dated 15.7.2003, by the assessing officer of Manoj Aggarwal, who wrote to the assessing officer of the present assessee. The relevant extract of the said letter is as follows :

“1) Various diaries have been seized from the possession of

Sh. Manoj Aggarwal which establish that Radhey Shyam

Bansal is a mediator for providing accommodation book

entries by Sh. Manoj Aggarwal. The quantum of transaction

done by him as per these documents is given in Annexure-A.

Photocopies of these paper are enclosed in Annexure-B.

2) There are evidences of cash having been received by Mr.

Manoj Aggarwal from Radhey Shyam Bansal.The summary of

the amounts so received as per various seized documents is

given in Annexure-C. The photocopies of these documents are

provided as per Annexure-D.”

3. The revenue’s contention on that occasion was that the actual

satisfaction had been recorded on the file by the assessing officer of Manoj Aggarwal on 29.8.2002. This Court in para 24 of its judgment (reported as 2011 337 ITR 217) recorded in this regard as follows :

“The last plank of submission of learned counsel appearing for

the revenue was a note that was recorded by the assessing

officer of the Manoj Aggarwal on the date of assessment. It is

contended by Ms. Prem Lata Bansal, learned senior counsel,

Mr.Sanjeev Sabharwal, Ms. Suruchi Aggarwal, Mr.

Chandramani Bhardwaj, learned counsel for the revenue that

though the said note was not filed before the tribunal but the

same should be treated as a part of evidence on record and

dealt with it. Whether that could have been taken as an

additional evidence under Order 41 Rule 27 (of Income Tax Rules, 1962) of the Code of

Civil Procedure though such an application has not been filed.

The same is not necessary in view of the finding recorded by the

tribunal in SMC Share Brokers Ltd.(supra) in. In the said case,

i.e., ITA No.250/Del/2005, the tribunal expressed the view that

a satisfaction note by the assessing officer of the searched

person recording undisclosed income of any person within the

meaning of Section 158BD (of Income Tax Act, 1961) could be validly recorded after

completion of assessment of the searched person. In that

context, the tribunal held the only requirement is that the

satisfaction must be in writing. In the said case, the tribunal

was dealing with the search carried out on the premises of

Manoj Aggarwal on 3.8.2000. The present case also relates to

the said search. It is noteworthy the departmental

representative in the case of SMC Share Brokers Ltd. (supra)

had pressed into service the note dated 29.8.2002 which has

been sought to be pressed into service by the learned counsel

for the revenue herein. The tribunal while dealing with the said

note dated 29.8.2002 expressed their views as follows:

“14.3 As per the Departmental Representative, the

satisfaction for initiating proceedings under Section

158BD was recorded by the AO making assessment in

the case of Shri Manoj Aggarwal and M/s Friends

Portfolio (P) Ltd. on 29th Aug., 2002 also i.e. on the

date of passing assessment order dt. 29th Aug., 2002

itself. However, the learned Counsel for the assessee

has seriously challenged the genuineness and the

authenticity of this note. According to him, this note is

antedated. He tried to substantiate his argument by

demonstrating that if the satisfaction note was recorded

on 29th Aug., 2002 then there would have been no

necessity to further record the satisfaction again on 26th

Nov., 2002. He also pointed out that from the contents

and language of the alleged satisfaction note dt. 29th

Aug., 2002, it is evident that this note is subsequently

prepared. He submitted that if the satisfaction was

recorded on 29th Aug., 2002, the notice should also

have been issued on that date itself or just thereafter.

14.4 The learned Departmental Representative, on the

other hand, maintained that the AO had made this note

on 29th Aug., 2002.

15. We have carefully considered the entire material on

record and the rival submissions. With this note, a list

of beneficiaries has been appended. The name of

assessee appears at item No. 69, which is as under:

69 SMC Sharebrokers Ltd.

17, Netaji

Subhash

Marg,

Daryaganj,

New

Delhi-02

Friends

Portfolio

(P) Ltd.

30000000 The assessee has taken bogus

accommodation entry through

M/s Friends Portfolio (P) Ltd.

and hence satisfaction note in this

regard has been recorded in the

case of this company and

proposal for centralization of this

case in this circle has been

approved for taking up

proceedings u/s 158BD (of Income Tax Act, 1961).

The last sentence in the above note indicates that the

proposal for centralization of this case in this circle has

been approved for taking up proceedings under Section

158BD. The learned Counsel pointed out before us that

no such approval was taken before 29th Aug., 2002.

According to him, the proposal is dt. 19th Sept., 2002,

i.e. after the date of the office note. The office note

cannot, therefore, mention any event, which has

occurred later on, i.e., after 29th Aug., 2002. The fact

that the proposal itself is dt. 19th May, 2002 could not

be controverted by the learned Departmental

Representative.

16. On going through the alleged office note available

on pp. 202 to 226, it is found that the office note has

been allegedly signed on 29th Aug., 2002 that is the date

on which the assessment order in the case of M/s

Friends Portfolio (P) Ltd. was completed. On closer

scrutiny of the facts and circumstances mentioned

above including the fact regarding the mention of

satisfaction note in the case of "this company" and

proposal for centralization of the case in the circle in

which the cases of searched persons fell, as referred to

above, and also in view of the circumstances relating to

this issue, we find force in the submissions of the

learned Counsel for the assessee made before us and

conclude that no satisfaction note was prepared on 29th

Aug., 2002 and this note has been prepared even after

26th Nov., 2002. Our reasons for holding so are as

under:

(i) Had the satisfaction been recorded on 29th Aug.,

2002, there would have been no necessity to record

another satisfaction on 26th Nov., 2002. The note refers

to the "satisfaction recorded in the case of this

company" which reference is to the satisfaction dt. 26th

Nov., 2002 and hence this note has been prepared

subsequent to satisfaction note dt. 26th Nov., 2002.

(ii) Had the satisfaction note been recorded on 29th

Aug., 2002 then the record pertaining to the other

person not searched should have been transferred to the

AO of the present assessee who was a different officer

at that time than the officer of the searched person.

(iii) The alleged satisfaction makes mention of the

proposal and approval regarding centralization of the

case. This proposal is dt. 19th Nov., 2002 and is

subsequent to the alleged note which fact proves the

contention of the learned Counsel for the assessee that

the notice (sic-note) is antedated.

(iv) There is a detailed note by the AO, a copy of which

has been filed at p. 33 of the paper book. The

concluding observations of the AO in this note are as

under:

“In view of the facts mentioned above and

the block assessment orders of Sh. Manoj

Aggarwal and M/s Friends Portfolio (P) Ltd.,

undisclosed income has arisen in the hands of M/s

SMC Share Brokers Ltd. which has been found

during the course of search and seizure operations

in the case of Shri Manoj Aggarwal and his

associate concerns. Thus, proceedings under

Section 158BD (of Income Tax Act, 1961) are applicable in this case.”

The date below the signatures of the AO is not legible

in this copy. Therefore, the learned Departmental

Representative was asked during the curse of hearing

of the case to verify the date of this note. On verification

from the record, she informed that the note is dt. 26th

Nov., 2002. This fact has been recorded by the Bench

on p. 33 itself.

17. In view of the above, it is clear that on or before

29th Aug., 2002, the AO of M/s Friends Portfolio (P)

Limited and that of Shri Manoj Aggarwal did not

record any satisfaction. The note dt. 29th Aug., 2002 is,

therefore, not to be taken for recording satisfaction

required under Section 158BC (of Income Tax Act, 1961)/158BD.”

4. This Court thereafter dealt with the revenue’s contention with respect to the note said to have been made on 26.11.2002. the Court recorded specifically in para 25 that the said note pertaining to the case of SMC Share Brokers V. Dy. CIT which was the subject matter of another appeal decided in a judgment reported as Commissioner of Income Tax v. SMC Share Brokers Ltd. 288 ITR 345. The judgment of the Supreme Court in Calcutta Knitwear (supra) pertinently held as follows :

“44. In the result, we hold that for the purpose of Section

158BD of the Act a satisfaction note is sine qua non and must

be prepared by the assessing officer before he transmits the

records to the other assessing officer who has jurisdiction over

such other person. The satisfaction note could be prepared at

either of the following stages: (a) at the time of or along with

the initiation of proceedings against the searched person under

Section 158BC (of Income Tax Act, 1961); (b) along with the assessment

proceedings under Section 158BC (of Income Tax Act, 1961); and (c)

immediately after the assessment proceedings are completed

under Section 158BC (of Income Tax Act, 1961) of the searched person

45. We are informed by Shri Santosh Krishan, who is

appearing in seven of the appeals that the assessing officer had

not recorded the satisfaction note as required under Section

158BD of the Act, therefore, the Tribunal and the High Court

were justified in setting aside the orders of assessment and the

orders passed by the first appellate authority. We do not intend

to examine the aforesaid contention canvassed by the learned

counsel since we are remanding the matters to the High Court

for consideration of the individual cases herein in light of the

observations made by us on the scope and possible

interpretation of Section 158BD (of Income Tax Act, 1961).”

5. In the present case the revenue’s contention are not different from

what they were in the main appeal, which was decided in the judgment

reported as CIT V. Radhey Shayam Bansal (2011) 337 ITR 217. It is sought

to be reported that the opinion formation contained in the letter dated

15.7.2003 accords with the opinion of Section 158BB (of Income Tax Act, 1961). In this regard the

court recollects and applies its findings in relation to the note (extracted inpara 2 above) on this aspect:

“23. In view of the aforesaid legal position we can now examine

the letter dated 15th July, 2003 which was communicated by the

Assessing Officer of the searched assessee to the assessing officer

of the respondent. The question is whether the aforesaid letter can

be regarded as “satisfaction” as required under Section

158BD, i.e. satisfaction of the Assessing Officer of Manoj

Aggarwal that there is material that the respondent assessee had

undisclosed income. The first paragraph of the aforesaid letter

states that the diary seized from the possession of Manoj

Aggarwal establishes that the respondent assessee had acted as a

mediator for providing accommodation book entries by Manoj

Aggarwal. The second sentence in the first paragraph states that

the quantum of transactions as shown in the documents were

enclosed as Annexure-A and the photocopies of the papers were

enclosed as Annexure-B. The second paragraph states that

there was evidence that cash was received by Manoj Aggarwal

from the respondent and the summary of the amounts received

as per the seized documents was given in Annexure C and the

photocopies of the documents were annexed as Annexure-D. It

is accepted that Annexures A, B, C & D, referred to in this

letter were not filed before the tribunal and have not been

produced before us. It is conceded by the learned counsel for

the revenue that they are also not available on the file of the

Assessing Officer of the respondent. There is no explanation

forthcoming with regard to the aforesaid annexures. It is well

nigh impossible to know their content. The first paragraph of

the letter dated 15th July, 2003 states that the respondent-

assessee had acted as a mediator i.e. they had introduced

Manoj Aggarwal with other persons to whom accommodation

book entries were provided by Manoj Aggarwal. There is no

allegation in the first paragraph that the respondent assessee

was provided with accommodation book entries or the amounts

belong to the respondent assessee. Book entries were provided

to third parties. It is not stated in this “satisfaction note” that

Manoj Aggarwal or third parties had paid any amount towards

commission for acting as a mediator. There is no such

allegation or statement in the “satisfaction note”. The second

paragraph does create some doubt but what is relevant and

important is the fact that in the first paragraph, it is accepted

by the Assessing Officer of Manoj Aggarwal that the

respondent assessee was merely acting as a mediator and

nothing more. The second paragraph of the letter states that

there was evidence that cash was received by Manoj Aggarwal

from the respondent assessees. What was the evidence and

material was not brought on record before the tribunal or even

before us. The said material is not mentioned in the assessment

order. It cannot be ̳ipse dixit„ without material or evidence to

satisfy the concept of requirement as engrafted under Section

158BD. What was the material was neither highlighted before

the tribunal nor before us. Thus, the appellant-revenue has not

discharged the onus that there was valid satisfaction as

required under Section 158 (of Income Tax Act, 1961) BD. Therefore, the irresistible

conclusion is the pre-requisite of “satisfaction” as engrafted

under Section 158B (of Income Tax Act, 1961) for the purpose of initiation of block

assessment proceeding is non-existent or absent.”

6. For the above reasons the revenue’s submission lacks merit.

Accordingly the appeal is dismissed.

S. RAVINDRA BHAT

(JUDGE)

R.K.GAUBA

(JUDGE)

JANUARY 07, 2015

×

Similar Ripples

Questions

Court invalidates order under Section 158BD (of Income Tax Act, 1961) due to lack of satisfaction note.

Write your CommentSimilar Posts

Generic

- Reportdata/4157.pdf