Full News

Court Orders Speedy Refund Processing for Tax Assessee Facing Financial Hardship

Court Orders Speedy Refund Processing for Tax Assessee Facing Financial Hardship

A company called UNITAC ENERGY SOLUTIONS (INDIA) PVT. LTD. is taking on the Principal Chief Commissioner of Income Tax and others. The company was pretty upset because they hadn't received their tax refunds for a couple of years, which was causing them some serious cash flow problems. The court stepped in and told the tax department to hurry up and sort out the refunds. It's a classic case of "time is money" in the business world.

Get the full picture - access the original judgement of the court order here

Case Name:

Unitac Energy Solutions (India) Pvt. Ltd. Vs Principal Chief Commissioner of Income Tax & Ors. (High Court of Kerala)

WP(C).No.26588 OF 2019(W)

Date: 4th February 2020

Key Takeaways:

1. The court recognized the importance of timely tax refunds for businesses facing financial hardship.

2. The judgment emphasizes the need for tax authorities to be proactive and considerate of taxpayers' financial situations.

3. The court set specific timelines for the tax department to process refunds and rectification applications, showing a balance between administrative procedures and taxpayer rights.

Issue:

The main question here is: Should the Income Tax Department be directed to issue pending tax refunds and process returns more quickly when a company is facing severe financial hardship due to delayed refunds?

Facts:

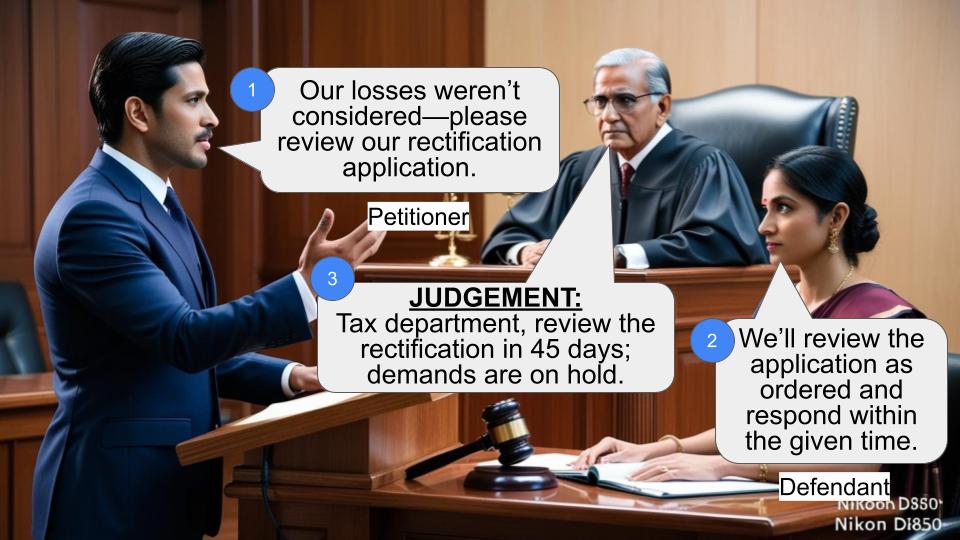

1. UNITAC ENERGY SOLUTIONS filed a writ petition because they were frustrated about not getting their tax refunds.

2. They were waiting on refunds for two assessment years: 2017-18 and 2018-19.

3. The company said they were owed around Rs.8 crores in total refunds (that's a lot of cash!).

4. They argued that without these refunds, their working capital was getting blocked, causing them "grave financial hardship".

5. For the 2017-18 assessment year, a refund of Rs.2,73,03,515 was ordered, but only Rs.1,20,67,181 was left after some adjustments.

6. For 2018-19, there was initially a demand of Rs.1,52,36,334, but the company filed a rectification application claiming they were actually due a refund of Rs.3,34,63,050 .

Arguments:

The petitioner (UNITAC ENERGY SOLUTIONS) argued:

1. They desperately needed the refunds to keep their business afloat.

2. The delay in processing returns and issuing refunds was causing them severe financial stress.

3. For 2018-19, they claimed there were issues with TDS credits that, if corrected, would result in a significant refund.

The respondents (Income Tax Department) countered:

1. They had already processed some refunds and made adjustments as per the law.

2. They needed time to process the rectification application for 2018-19 as per standard procedures.

Key Legal Precedents:

Interestingly, this judgment doesn't cite specific legal precedents. Instead, it focuses on the application of existing tax laws, particularly:

1. Section 143(1) (of Income Tax Act, 1961) for intimation of tax assessment .

2. Section 245 (of Income Tax Act, 1961) for making adjustments to refunds .

3. Section 154 (of Income Tax Act, 1961) for rectification of mistakes .

Judgment:

The court came down on the side of the company, showing some real understanding of their cash flow struggles. Here's what they decided:

1. The tax department should credit the remaining refund of Rs.1,20,67,181 for 2017-18 to the company's bank account within a week .

2. For 2018-19, the court told the Assessing Officer to look at the rectification application ASAP. They should make a decision within 3-4 weeks of getting a copy of this judgment .

3. The court emphasized that while this timeline is tight, it's necessary given the company's financial situation .

FAQs:

1. Q: Why did the court set such a short timeline for the tax department?

A: The court recognized the "extremely precarious nature of the cash liquidity issues" faced by the company and wanted to ensure quick action to prevent further financial hardship.

2. Q: What happens if the company disagrees with the facts stated in the judgment?

A: The court said the company can file a representation to the competent authority in the Income Tax Department to address any factual discrepancies.

3. Q: Does this judgment set a precedent for other companies facing similar issues?

A: While each case is unique, this judgment does highlight the court's willingness to consider the real-world financial impacts of delayed tax refunds on businesses.

4. Q: What's the takeaway for the Income Tax Department from this case?

A: The judgment suggests that tax authorities should be more proactive and considerate of taxpayers' financial situations, especially when dealing with refunds and rectification applications.

1.The factual aspects broadly stated in this writ petition are as follows: That the petitioner company is aggrieved by the non-disbursal of refund for the A.Y. 2017-18 in terms of Ext.P1 intimation under section 143(1) (of Income Tax Act, 1961). Petitioner is also seeking for a direction to process the return for A.Y. 2018-19. Revenues failure to grant refund has resulted in blocking of working capital of petitioner company and has caused grave financial hardship. The aggregate of the eligible refunds if A.Y. 2019-20 is also included, would come to around Rs.8 crores. If legitimate refunds continue to be held back and the processing of return and consequent issuance of refunds are delayed, petitioner company cannot survive due to lack of working capital. Hence aggrieved by the failure of respondents to issue refund for the A.Y. 2017-18 and to process the return for A.Y. 2018- 19, this writ petition is filed with the following prayers. (a) To issue a writ of mandamus or any other appropriate writ, order or direction directing the respondents to issue the refund due to the petitioner in terms of Ext.P1 for the AY 2017-2018. (b) to issue a writ o f mandamus or any other appropriate writ, order or direction directing the respondents to process the return for the A.Y. 2018-19 and issue the refund due to the petitioner without delay.

2. Heard Smt. Nisha John, learned counsel appearing for the petitioners and Sri. Jose Joseph, learned standing counsel for the Income Tax Department, Government of India, appearing for all the respondents.

3. The respondents have initially filed a statement dated 30/11/2019 in this case. Later, Sri.Jose Joseph, learned standing counsel for the Income Tax Department, Government of India appearing for the respondents have submitted that there are some crucial subsequent developments in this case which has occurred after the filing of the statement on 30/11/2019 and that an additional statement in that regard is being filed. Accordingly, it is seen that the additional statement dated 27/01/2020 has been filed on behalf of the respondent before this Court on 29/01/2020. Smt. Nisha John, learned counsel appearing for the petitioner has made submissions mainly in tune with the pleadings in WP(c) as well as the reply affidavit to the first statement.

4. From the submissions made on behalf of the respondents, it appears that the facts stated in this case are in relation to two assessment years for the petitioner assessee, viz, assessment years 2017-18 and the subsequent assessment year, 2018-19. According to the respondents,assessment under Section 142(3) (of Income Tax Act, 1961) for the assessment year 2017-18 in this case was duly completed on 27/12/2020 and that, refund of an amount to the tune of Rs.2,73,03,515/- was duly ordered. Further that, adjustment in that regard was made by the competent authority of the respondent under Section 245 (of Income Tax Act, 1961), whereby the balance refund due to the petitioner to the tune of Rs.1,20,67,181/- for the assessment year 2017-18 and that proceedings are issued, directing the said balance refund amount to be duly released to the petitioner as per proceedings issued on 30/01/2020. Further it is stated by the learned standing counsel for the respondents that steps are to be taken to ensure that the said refund amount of Rs.1,20,67,181/- is duly credited to the bank account of the petitioner through electronic means without much delay and it is expected that process will be completed within a week or so.

5. Further it is pointed out that for the assessment year 2018-19, the demand was to the tune of Rs.1,52,36,334/-, the demand including interest as brought out in the intimation under Section 143(1) (of Income Tax Act, 1961) for the said assessment year 2018-19 comes to Rs.1,52,36,334/-. Further it is pointed out that for the assessment year 2018-19, the petitioner has filed rectification application u/s 154 (of Income Tax Act, 1961), which has now been received by the respondent on 27/01/2020. It is pointed out that under the provisions contained in Section 154(8) (of Income Tax Act, 1961), the Assessment Officer has a time limit up to a period of 6 months from the date of receipt of the application to consider and dispose off the same. It is pointed out that the main issue raised in the rectification application is that due to some apparent problems in the TDS amounts, due credit was not given and that the plea of the petitioner is that if those technical issues are dealt with, then the petitioner is legally entitled to secure the benefit of those TDS credits and therefore, petitioner is entitled for a refund of an amount to the tune of Rs.3,34,63,050/-.

6. Having regard to the facts and circumstances of this case, it is ordered that the Assessment Officer concerned, viz, the 3rd respondent- Assistant Commissioner of Income Tax, who is the assessing officer concerned, may take all reasonable endeavors possible under these circumstances to ensure that the plea made by the petitioner in the above said rectification application filed under section 154 (of Income Tax Act, 1961), for the assessment years 2018-19 may be taken up without any further delay, and after affording reasonable opportunity of being heard to the petitioner,through authorized officials or a counsel if any, will take a considered decision thereon and also take into consideration, the plea of the petitionerthat the petitioner is legally entitled for securing the benefit of claim for TDS credit as afore stated without much delay, going by the case of the petitioner, that the amounts involved in the TDS problems are rectified,which comes to the tune of more than Rs.3.34 crores, and also taking into account, extreme fragility of the liquidity issues now being faced by the petitioner concerned. The 3rd respondent may take a pro-active approach and may understand the fiscal and business problems now faced by the petitioner assessee and may pass orders on the said rectification application for the assessment year 2018-19 within 3 to 4 weeks from the date of production of a certified copy of this judgment. This Court would observe that ordinarily, such a time limit may be short for a decision making process, but having regard to the above said crucial issues and also the fact that the petitioner has been waiting for refund for quiet a long time and also taking into account, the extremely precarious nature of the cash liquidity issues now faced by the petitioner's business concern, it is hoped and expected that the 3rd respondent would rise to the occasion and would take necessary steps to meet the said time deadline, in the interest of justice and fairness.

7. It is further ordered that in case, if the petitioner has a case that any of the facts and figures mentioned herein above does not reflect the correct factual position, then certainly it is open to the petitioner to seek redressal of such grievances by filing appropriate representation before the competent authority concerned of the Income Tax Department, without any further delay, and if so filed, the said competent authority would examine those grievances of the petitioner as well and render a considered decision thereon after affording reasonable opportunity of being heard to the petitioner.

With these observations and directions, the above Writ Petition (Civil) stands finally disposed of.

×

Similar Ripples

Questions

Court Orders Speedy Refund Processing for Tax Assessee Facing Financial Hardship

Write your CommentSimilar Posts

Generic

- Reportdata/6297.pdf