Full News

Court Overturns Tax Recovery Order, Citing Delayed Appeal Process

Court Overturns Tax Recovery Order, Citing Delayed Appeal Process

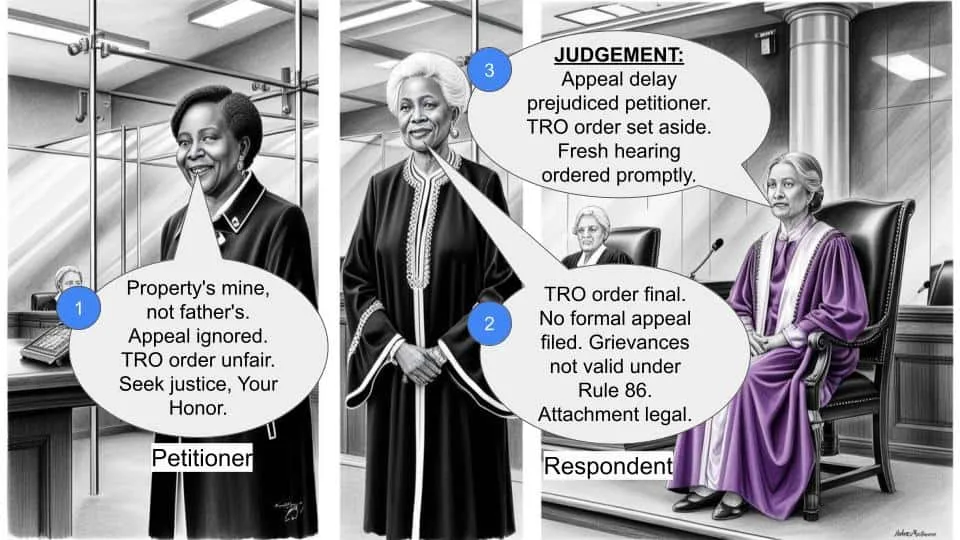

The High Court set aside a Tax Recovery Officer's (TRO) order attaching a petitioner's property for his late father's tax dues. The court criticized the Income Tax department for delays in processing the petitioner's appeal, which led to prejudice against him.

Get the full picture - access the original judgement of the court order here.

Case Name:

Vinod K. Bhagat vs Tax Recovery Officer (High Court of Bombay)

Writ Petition No.2788 of 2014

Key Takeaways:

1. The court emphasized the importance of timely processing of appeals in tax recovery cases.

2. Delay in addressing appeals can lead to prejudice against taxpayers.

3. Tax authorities should not render statutory provisions ineffective through administrative delays.

4. The court restored the petitioner's appeal for fresh disposal by the Jurisdictional Commissioner.

Issue:

Whether the Tax Recovery Officer's order attaching the petitioner's property for his late father's tax dues should be upheld when the petitioner's appeal against the attachment was not promptly addressed by the Income Tax department?

Facts:

1. The petitioner's property and bank accounts were attached for tax dues payable by his late father.

2. The petitioner filed grievances (treated as appeals) against this attachment on 13.4.2012 and 7.5.2012.

3. The Chief Commissioner of Income Tax directed the Jurisdictional Commissioner to treat these grievances as appeals under Rule 86 of the Second Schedule of the Income Tax Act, 1961 on 10.5.2012.

4. Despite this direction, the Jurisdictional Commissioner did not immediately address the appeal.

5. Meanwhile, the Tax Recovery Officer passed an order on 25.9.2012 upholding the attachment of the petitioner's property.

6. The Jurisdictional Commissioner finally disposed of the petitioner's appeal on 15.5.2014, nearly two years after it was filed.

Arguments:

1. Petitioner's Argument:

The petitioner challenged the notices attaching his property and bank accounts, as well as the TRO's order upholding the attachment. He argued that the property belonged to him, not his late father.

2. Tax Department's Argument:

The Jurisdictional Commissioner argued that:

a) The TRO's order was conclusive under Rule 11(6) of the Second Schedule of the Act, and no appeal could be entertained against it.

b) No formal appeal was filed against the TRO's order dated 25.9.2012.

c) The grievances filed by the petitioner were not formal appeals under Rule 86 of the Second Schedule of the Act .

Key Legal Precedents:

The judgment does not explicitly cite any legal precedents. However, it relies on the provisions of Rule 86 of the Second Schedule to the Income Tax Act, 1961, which provides for appeals against certain orders of the Tax Recovery Officer .

Judgement:

1. The court set aside the TRO's order dated 25.9.2012.

2. The court also set aside the Jurisdictional Commissioner's order dated 15.5.2014 and restored the petitioner's appeal for fresh disposal.

3. The court directed the Jurisdictional Commissioner to grant a personal hearing to the petitioner and dispose of the appeals within three months.

4. The court maintained the status quo regarding the attachment of property and bank accounts.

FAQs:

Q1: Why did the court set aside the TRO's order?

A1: The court set aside the order because the petitioner's appeal was not promptly addressed, causing prejudice to his case.

Q2: What was the main issue with the Income Tax department's handling of the case?

A2: The main issue was the significant delay in processing the petitioner's appeal, which the court found unacceptable.

Q3: Did the court completely remove the attachment on the petitioner's property?

A3: No, the court maintained the status quo regarding the attachment but allowed for a fresh hearing of the petitioner's appeal.

Q4: What directive did the court give to the Jurisdictional Commissioner?

A4: The court directed the Commissioner to grant a personal hearing to the petitioner and dispose of the appeals within three months.

Q5: What is the significance of Rule 86 of the Second Schedule to the Income Tax Act in this case?

A5: Rule 86 (of Income Tax Rules, 1962) provides for appeals against certain orders of the Tax Recovery Officer, which the court emphasized should be promptly addressed when filed.

1. At the request and instance of learned Counsel appearing for the parties, this petition is being disposed of finally at the stage of admission.

2. This petition under Article 226 of Constitution of India challenges the notices dated 25.1.2012 and 6.3.2012 attaching the petitioner's property and bank accounts in respect of tax dues payable by the petitioner's late father. The petitioner has also challenged the order dated 25.9.2012 passed by the Tax Recovery Officer holding that the property belonging to the petitioner which has been attached, for the Income Tax dues payable by his late father.

3. Mr. Vipul Joshi. learned Counsel appearing for the petitioner points out that after the property and the bank accounts of the petitioner were attached, the petitioner moved an application by letter dated 13.4.2012 to the Jurisdictional Commissioner of Income Tax making grievance regarding attachment of the petitioner's property and his bank accounts for recovery of income tax dues payable by his late father. The petitioner in the aforesaid communication did not formerly refer to his applications as appeals but set out his grievances with regard to the action of Tax Recovery Officer in attaching the petitioner's property as well as bank accounts. As there was no response, the petitioner by letter dated 7.5.2012 also made a grievance to the Chief Commissioner of Income Tax.

4. On 10.5.2012 the Chief Commissioner of Income Tax addressed a communication to the Jurisdictional Commissioner to dispose of the petitioner's grievance as contained in the letter dated 13.4.2012 and 7.5.2012, which in effect, according to the Chief Commissioner, was nothing but an appeal as contemplated in Rule 86 (of Income Tax Rules, 1962) of II Schedule of the Income Tax Act,1961 (the Act) against the Tax Recovery Officer's (TRO) action of recovery under II Schedule of the Act. Notwithstanding the above directions of the Chief Commissioner of Income Tax, the Jurisdictional Commissioner of Income Tax did not immediately deal with the petitioner's appeal filed in the form of grievances.

5. The petitioner by various communications dated 23.5.2012, 2.7.2012 and 29.1.2014 called upon the Jurisdictional Commissioner of Income Tax to dispose of his appeal (filed as grievances) under Rule 86 of the II Schedule to the Act.

6. In the meantime, pending the petitioner's appeal under Rule 86 of the Second Schedule to the Act, the Tax Recovery Officer passed an order dated 25.9.2012 holding that the attachment of the immovable properties belonging to the petitioner was valid. This was on the ground that the same belonged to the petitioner's late father. The petitioner has challenged the order dated 25.9.2012 as being one without jurisdiction.

7. Thereafter on 15.5.2014, the Jurisdictional Commissioner of Income Tax disposed of the petitioner's appeal (filed as grievances) under Rule 86 of the Second Schedule to the Act by holding as follows:-

(a) The order dated 25.9.2012 of the Tax Recovery Officer having been passed under Rule 11 (of Income Tax Rules, 1962) of Second Schedule of the Act is a conclusive order. Therefore, no appeal under Rule 86 of the Second Schedule to the Act could be entertained;

(b) No appeal has been filed from the order dated 25.9.2012; and

(c) In any case the appeals which were filed in the form of grievance dated 13.4.2012 and 7.5.2012, were not formal appeals filed under Rule 86 of the Second Schedule of the Act and consequently same could not be considered.

8. We find that inspite of specific directions of the Chief Commissioner of Income Tax by his letter dated 10.5.2012 to treat the petitioner's grievance letters as appeals from the orders of attachment of the petitioner's property and bank accounts, the Jurisdictional Commissioner has not entertained the appeal for over two years. Thereafter, he relies upon the order dated 25.9.2012 passed subsequently by TRO to conclude that in view of the order passed by the TRO being a conclusive order under Rule 11(6) of the Second Schedule to the Act, no appeal against such an order is maintainable and in fact no appeal against that order has been filed.

9. We are of the view that in case the Jurisdictional Commissioner of Income Tax had acted upon the directions dated 10.5.2012 of the Chief Commissioner of Income Tax and disposed of the petitioner's appeal immediately, then the petitioner's grievance could have been considered by him on merits before the TRO passed the impugned order dated 25.9.2012. The delay in the Jurisdictional Commissioner of Income Tax taking up the petitioner's grievance which even according to the Chief Commissioner was nothing but an appeal under Rule 86 (of Income Tax Rules, 1962) of Second Schedule to the Act and disposing it of on merits, has caused prejudice to the petitioner as his grievance that the attached property does not belong to his father, has gone unattended leading to the TRO passing order dated 25.9.2012. It is only thereafter on 15.5.2014 the Jurisdictional Commissioner disposed of the petitioner's appeals in the form of grievance dated 13.4.2012 and 7.5.2012, in effect taking the plea of fait accompli by virtue of the order dated 25.9.2012 passed by the TRO. We find that when the appeal provision is provided under Rule 86 (of Income Tax Rules, 1962) of Second Schedule to the Act and the petitioner has filed such an appeal even according to the Chief Commissioner of Income Tax, then the Jurisdictional Commissioner should have decided such an appeal at the earliest. This not having been done in the present case, has resulted in great prejudice to the petitioner as his grievance against the order of attachment passed by TRO is not being considered in appeal even though the Statute provide for the same. The TRO should have in all fairness awaited the disposal of the petitioner's appeal under Rule 86 (of Income Tax Rules, 1962) to the Second Schedule of the Act pending with the Jurisdictional Commissioner of Income Tax before disposing of the attachment proceedings under Rule 11 of the Second Schedule of the Act. It is not expected of officers acting under the Act to render the provisions of the Act a dead letter by gross delay and thereafter pleading helpless in view of subsequent events by his subordinate Officer.

10. In the above view, in the peculiar facts of the case, we set aside the order dated 25.9.2012 passed by the TRO. We do not disturb the attachments of property and the bank accounts. We make it clear that the status quo as of that day would continue. The order dated 15.5.2014 of the Jurisdictional Commissioner of Income Tax though not specifically challenged in the appeal, in the peculiar facts of this case, we set aside the order dated 15.5.2014 and restore the petitioner's appeal before the Jurisdictional Commissioner for fresh disposal. The Jurisdictional Commissioner would grant a personal hearing to the petitioner and dispose of the petitioner's appeals filed as grievances dated 13.4.2012 and 7.5.2012 as expeditiously as possible preferably within a period of three months from today. In the meantime, the petitioner undertakes to maintain status quo.

11. Petition disposed of with the above directions. No order as to costs.

(G.S.KULKARNI, J.) (M.S.SANKLECHA, J.)

×

Similar Ripples

Questions

Court Overturns Tax Recovery Order, Citing Delayed Appeal Process

Write your CommentSimilar Posts

Generic

- Reportdata/3988.pdf