Full News

Court Quashes Income Tax Reassessment Based Solely on Audit Objections

Court Quashes Income Tax Reassessment Based Solely on Audit Objections

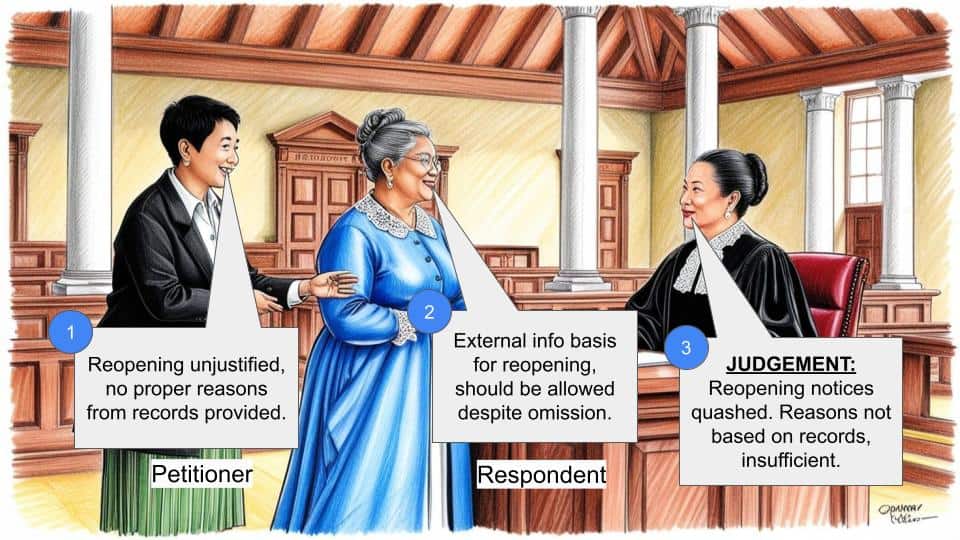

This case involves P.C. Patel and Company challenging a notice issued by the Deputy Commissioner of Income Tax to reopen their assessment for the 2010-11 tax year. The court ruled in favor of P.C. Patel, quashing the reassessment notice and subsequent proceedings, as they were based solely on audit objections without independent reasoning by the Assessing Officer.

Get the full picture - access the original judgement of the court order here

Case Name:

P.C. Patel & Company Vs Deputy Commissioner of Income Tax (High Court of Gujarat)

Special Civil Application No. 3023 of 2015

Date: 6th May 2015

Key Takeaways:

- Reassessment proceedings initiated solely based on audit objections, without independent reasoning by the Assessing Officer, are invalid.

- The Assessing Officer must form an independent opinion that income has escaped assessment for reopening to be valid.

- Courts can intervene under Article 226 of the Constitution when reassessment proceedings are found to be invalid.

Issue:

Was the reopening of the assessment for AY 2010-11 valid when it was based solely on audit objections without independent reasoning by the Assessing Officer?

Facts:

- P.C. Patel and Company filed a tax return for AY 2010-11 on 5.10.2010, declaring a total income of Rs. 6,63,27,750.

- The return was selected for scrutiny, and assessment was completed under section 143(3) (of Income Tax Act, 1961).

- On 13.8.2013, the Deputy Commissioner of Income Tax issued a notice under section 148 (of Income Tax Act, 1961) to reopen the assessment.

- The reopening was based on an audit objection regarding the rate of depreciation claimed on certain vehicles.

- The Assessing Officer initially disagreed with the audit objection but proceeded with reopening to “safeguard the revenue.”

Arguments:

Petitioner (P.C. Patel and Company):

- The reopening was solely based on audit objections without independent reasoning by the Assessing Officer.

- The formation of opinion by the Assessing Officer was vitiated.

Respondent (Revenue):

- The Assessing Officer had formed an independent opinion that income had escaped assessment.

- Reopening based on information from audit objections is permissible.

Key Legal Precedents:

- Commissioner of Income-tax, Ahmedabad-IV vs. Shilp Gravures Ltd. [2013] 40 taxmann.com 309 (Gujarat)

- Rajrtan Metal Industries Ltd vs. Assistant Commissioner of Income Tax [2014] 49 taxmann.com 15 (Gujarat)

- Commissioner of Income Tax v. P.V.S. Beedies Pvt. Ltd. 237 ITR 13 (SC)

- N.K. Industries Ltd. v. Income Tax Officer (OSD) 362 ITR 502 (Guj)

Judgement:

The court ruled in favor of P.C. Patel and Company, quashing the reassessment notice and subsequent proceedings. The court found that:

- The Assessing Officer did not form an independent opinion that income had escaped assessment.

- The reopening was solely based on audit objections, which is not permissible.

- The formation of opinion by the Assessing Officer was vitiated.

The court exercised its power under Article 226 of the Constitution to quash the reassessment proceedings.

FAQs:

Q: Can an assessment be reopened based on audit objections?

A: While information from audit objections can be used, the Assessing Officer must independently form an opinion that income has escaped assessment.

Q: What is the significance of this judgment for taxpayers?

A: It protects taxpayers from arbitrary reassessments based solely on audit objections without proper reasoning by tax authorities.

Q: Does this mean audit objections are irrelevant in reassessment proceedings?

A: No, audit objections can still be considered, but they cannot be the sole basis for reopening an assessment without independent reasoning by the Assessing Officer.

Q: What should taxpayers do if they receive a reassessment notice?

A: They should carefully examine the reasons for reopening and consider challenging it if it appears to be based solely on audit objections without independent reasoning.

Q: Can the tax department appeal this decision?

A: Yes, the tax department can potentially appeal this decision to a higher court if they believe there are grounds to do so.

1. By way of this petition under Article 226 of the Constitution of India to quash and set aside the impugned notice dated 13.8.2013 (Annexure A) issued by the respondent under section 148 (of Income Tax Act, 1961) (for short “the Act”) to reopen the original assessment for AY 2010-11 as well as the order of reassessment passed.

2. That the petitioner filed return of income for AY 2010-11 on 5.10.2010 declaring total income of Rs.6,63,27,750/-. That the said return of income was selected for scrutiny and the Assessing Officer completed the regular assessment under section 143(3) (of Income Tax Act, 1961) after issuing/sending detailed questionnaire with notice under section 142(1) (of Income Tax Act, 1961) and after considering the details submitted by the petitioner in response to the said notice.

2.1 That thereafter, the respondent has issued the impugned notice dated 13.8.2013 under section 148 (of Income Tax Act, 1961) for AY 2010-11 to reassess the total income. That in response to the said notice, the petitioner vide letter dated 22.8.2013 requested the Assessing Officer to treat the original return filed on 5.10.2010 as in response to the impugned notice under section 148 (of Income Tax Act, 1961) and also supplied copy of reasons recorded for reassessment.

2.2 That approximately, after a period of 11 months, vide communication dated 8.7.2014, the Assessing Officer supplied to the petitioner – assessee copy of reasons recorded. That the petitioner submitted the objections against reopening of the concluded and completed assessment, which came to be disposed of by the Assessing Officer vide communication dated 13.1.2015. At this stage, the petitioner has preferred the present Special Civil Application under Article 226 of the Constitution of India challenging the impugned notice under section 148 (of Income Tax Act, 1961) to reopen the completed assessment for AY 2010-11.

2.3 As during the pendendy of the present petition, the Assessing Officer has passed the order of assessment under section 143(3) (of Income Tax Act, 1961) read with section 147 (of Income Tax Act, 1961), the petitioner has also challenged the impugned order of assessment also.

3. Shri Vivek Chavda, for Shri SN Divetia, learned Advocate appearing on behalf of the petitioner has vehemently submitted that the reopening of the assessment for AY 2010-11 is solely on the basis of the audit objection and/or the audit objection by the audit party and therefore, the same is not permissible. It is submitted that therefore, forming opinion by the Assessing Officer that the income has escaped assessment has been vitiated.

3.1 It is vehemently submitted by Shri Chavda, learned Advocate appearing on behalf of the petitioner that though in the objections raised by the petitioner against reopening of the assessment, it was specifically stated that reopening of the assessment is at the instance of the audit party and/or on the audit objections raised by the audit party only, the Assessing Officer while disposing off the objections has not dealt with the same at all.

3.2 It is further submitted that even in the present Special Civil Application though the petitioner has raised the specific ground on the aforesaid, in the affidavit in reply, the respondent has not dealt with the same. Making above submissions and relying upon the decision of the Division Bench in the case of Commissioner of Income-tax, Ahmedabad-IV vs. Shilp Gravures Ltd. reported in [2013]40 taxmann.com 309 (Gujarat) as well as in the case of Rajrtan Metal Industries Ltd vs. Assistant Commissioner of Income Tax reported in [2014]49 taxmann.com 15 (Gujarat), it is requested to allow the present Special Civil Application and quash and set aside the impugned reopening of the assessment for AY 2010-11.

4. Present petition is opposed by Shri Pranav G. Desai, learned Advocate appearing on behalf of the Revenue. He has heavily relied upon the affidavit in reply filed on behalf of the respondent.

4.1 Shri Desai, learned advocate appearing on behalf of the Revenue has vehemently submitted that the impugned reopening proceedings to reopen the assessment for AY 2010- 11 is absolutely just and proper and in consonance with Section 147 (of Income Tax Act, 1961). It is vehemently submitted that in the present case, after forming an independent opinion though the petitioner was entitled for normal rate of depreciation i.e. 15%, the petitioner availed the higher rate of depreciation at 30%. It is submitted that the higher rate of depreciation at 30% is admissible on motor vehicles only if they are used for business of hiring. It is submitted that the petitioner is not engaged in the business of vehicle hiring and therefore, was/is not entitled for depreciation at 30%. It is submitted that therefore, having formed an independent opinion, that an amount of Rs.3,26,65,256/- (depreciation being restricted to 15% as against 30% as claimed) has escaped assessment, the Assessing Officer has rightly reopened the assessment and has rightly issued notice under section 148 (of Income Tax Act, 1961).

4.2 It is further submitted by Shri Desai, learned advocate appearing on behalf of the revenue that now when the reassessment order is already passed under section 143(3) (of Income Tax Act, 1961) r/w section 147 (of Income Tax Act, 1961), it is requested not to entertain the present petition and relegate the petitioner to avail the remedy by way of appeal before the learned CIT (Appeals) and if aggrieved, in that case, before the learned Tribunal.

4.3 Relying upon para 6 of the communication by the Assessing Officer to the higher authority while seeking approval to initiate the reassessment proceedings and relying upon the reasons recorded by the Assessing Officer while issuing the notice under Section 148 (of Income Tax Act, 1961), Shri Desai, learned Advocate appearing on behalf of the petitioner has vehemently submitted that the Assessing Officer had formed an independent opinion that the income of Rs.3,26,65,256/- had escaped assessment. It is submitted that therefore this is not a case where the assessment is reopened solely at the instance of the audit party and/or audit objection raised by the audit party. It is submitted that therefore the decisions upon which the reliance has been placed by the learned advocate appearing on behalf of the petitioner shall not be applicable to the facts of the case on hand and/or shall not be of any assistance to the petitioner.

4.4 Relying upon the decision of the Hon’ble Supreme Court in the case of Commissioner of Income Tax v. P.V.S. Beedies Pvt. Ltd. reported in 237 ITR 13 (SC) and decision of the Division Bench of this Court in the case of N.K. Industries Ltd. v. Income Tax Officer (OSD) reported in 362 ITR 502 (Guj), it is vehemently submitted by Shri Desai, learned Advocate appearing on behalf of the Revenue that as observed by the Hon’ble Supreme Court in the aforesaid decision and the Division Bench of this Court, on the basis of the information given by the audit party and/or the objection raised by the audit party, reopening of the assessment is permissible. It is submitted that therefore even in case where the assessment is reopened on the basis of the objection raised by the audit party and on the information received by the Assessing Officer pursuant to the audit memo and/or the objections raised by the audit party, after forming an opinion, the reopening of assessment proceedings is permissible. Making above submissions and relying upon above decisions it is requested to dismiss the present petition.

5. Heard learned advocates appearing on behalf of respective parties at length. At the outset it is required to be noted that what is challenged in the present Special Civil Application is the impugned notice under section 148 (of Income Tax Act, 1961) by which the assessment for AY 2010-11 has been reopened. The reasons recorded for reopening of the assessment proceedings for the AY 2010-11 reads as under:

“The assessee firm had filed return of income of Rs.6,63,27,750/- for AY 2010-11 on 5.10.2010. The case was selected for scrutiny and the assessment was completed u/s 143(3) (of Income Tax Act, 1961) with total income assessed at Rs.7,88,27,750/-. The assessee firm is engaged in the business of construction and mining contractor. For the AY 2010-11, the assessee firm has claimed depreciation @ 30% on dumpers, lorries etc. amounting to Rs.6,53,30,512/-, the assessee firm is primarily a contractor and income received is towards civil works executed & from contract works. The higher rate of depreciation @ 30% is admissible on motor vehicles only if they are used for the business of hiring. In other cases, normal rate of depreciation i.e. @ 15% only is allowable. The assessee firm being a contractor and income received is from earthwork and contract income, and is not in business of transportation. The above fact was not brought the course of assessment proceedings, therefore, the assessee has failed to disclose fully and truly all material facts necessary for assessment. Consequently, an amount of Rs.3,26,65,256/- (depreciation being restricted to 15% as against 30% as claimed) has escaped assessment.”

5.1 The aforesaid reopening of the assessment/re- assessment proceedings has been challenged mainly on the ground that the reopening of the assessment is solely on the basis of the objection raised by the audit party and/or audit objection and the formation of the opinion by the Assessing Officer that the income of Rs.3,26,65,256/- has escaped assessment has been vitiated inasmuch as there is no independent formation of opinion by the Assessing Officer on the escapement of the income from assessment.

5.2 It is required to be noted that though in the objections raised by the petitioner against reopening of the assessment proceedings, the petitioner specifically raised the above ground, the Assessing Officer while disposing off the objections has not dealt with the same. Even in the petition the said ground is raised, however the same has not been dealt with in the affidavit in reply. In the affidavit in reply it is the case on behalf of the Revenue that while recording the reasons for reopening of the assessment and/or while reopening of the assessment for AY 2010-11, the Assessing Officer has formed an opinion that the income of Rs.3,26,65,256/- had escaped assessment. However, nothing has been mentioned with respect to any objections raised by the audit party and/or any audit objection. Be that as it may, to satisfy ourselves whether the reopening of the assessment proceedings is solely on the basis of the audit objection raised by the audit party and/or at the instance of the audit party only and/or whether there is any independent formation of opinion by the Assessing Officer that the income has escaped assessment, we called upon the Revenue to produce the relevant file/s and Shri Desai, learned Advocate appearing on behalf of the Revenue has produce the file/s before this Court for perusal.

5.3 From the file, it appears that the case was audited by the revenue audit party. The audit party issued LAR 2497, para 3. It also appears that the same was sent to the Assessing Officer and Asst. Commissioner of Income Tax, Gandhidham and audit objection was brought to the notice of the Assessing Officer. However, the Asst. Commissioner of Income Tax, Gandhidham raised objection against audit objection and justified his action of allowing the depreciation at 30% by submitting that the assessee had executed agreement of hiring of heavy earth moving machinery for excavation work with GMDC and Rajasthan Government and therefore, higher depreciation was eligible to the assessee. It appears from the file that the explanation given by the Assessing Officer was not accepted by the audit party.

5.4 From the file, it appears that thereafter, the Commissioner of Income Tax, Rajkot on 8.8.2013 communicated to the Joint Commissioner of Income Tax, Gandhidham that the audit objection raised are acceptable and therefore, proceedings to reopen the cases under section 147 (of Income Tax Act, 1961) may be initiated, in the prescribed manner in view of the CBDT instructions on the matter. From the file, it appears that thereafter, the Deputy Commissioner of Income Tax sent a report in the prescribed proforma to the Commissioner of Income Tax so as to reopen the assessment under section 147 (of Income Tax Act, 1961). Even the proforma report on the draft audit para No.1 LAR 2497, the Deputy Commissioner of Income Tax continued to maintain that audit pointed out are not acceptable, however, the case has been reopened under section 147 (of Income Tax Act, 1961) to safeguards of the revenue. Only thereafter, at the instance of the audit objection raised by the audit party and the instruction given by the Commissioner of Income Tax to reopen the assessment for AY 2010-11, the Assessing Officer has issued the notice under section 148 (of Income Tax Act, 1961) in the proforma report while not allowing that and/or accepting the audit objection, the Deputy Commissioner of Income Tax/ Assessing Officer has stated as under:

“(i)Assessee-firm is engaged in the business of providing equipments, motor Vehicles on hire, the same fact has been duly stated by the auditors in form No.3CD. Further, the claim of the assessee is also supported by Circular No.652 dated 14.06.1993. Since, the basic nature of the business of the assessee itself is providing equipments and motor vehicles on hire, hirer rate of depreciation is admissible.

ii) The fact that the nature of business is that of HIRING OF EQUIPMENTS/ MOTOR VEHICLES is established on the basis of copies of tender for allotment of contract. The reliance is also placed on CIT V. Madan & Co. (2002) 254 ITR 445(MAD) which is applicable to the case under consideration, Here it was held that when the vehicles are not used for the purpose of the owner, it is covered under the word HIRE. In this case vehicles are not used for the purpose of the owner and hence it is appropriate to conclude that the same has been HIRED TO THIRD PARTY. Once the vehicles are established as having been given on hire, the higher Claim of depreciation can be claimed. However, the case was reopened u/ 5.147 of the Act, to safeuards of the revenue.”

5.5 From the aforesaid, it appears that even while sending the proposal/proforma report to the higher authority to grant approval for reopening the assessment, the Assessing Officer continued to maintain that the audit objection raised by the audit party is not acceptable and only with a view to protect the revenue and/or safeguards the interest of the revenue, it was proposed to reopen the assessment under section 147 (of Income Tax Act, 1961). There is no independent formation of opinion by the Assessing Officer that the amount of Rs.3,26,65,256/- has escaped assessment. The complete assessment has been reopened only at the instance of the audit party and/or on the audit objection raised by the audit party, which is not permissible. Therefore, in the facts and circumstances of the case, formation of opinion by the Assessing Officer while reopening the completed assessment and his reason to believe that the income as escaped assessment has been vitiated and therefore, reopening assessment proceedings for AY 2010-11 is not valid and permissible.

5.6 In the case of Shilp Gravures Ltd. (Supra) after considering the decision of the Division Bench of this Court in the case of Adani Exports v. Dy. CIT reported in [1999] 240 ITR 224 (Guj.) and the decision of the Division Bench of this Court in the case of Cadila Healthcare Ltd. v. Asstt. CIT dated 14.12.2011 in Special Civil Application No.15566/2011, it is held that any reassessment proceeding initiated at the instance of the audit party objection without the Assessing Officer himself having reason to believe that the income chargeable to tax has escaped the assessment must fail. Similar view has been taken by the Division Bench of this Court in the case of Raajratna Metal Industries Ltd. (Supra).

5.7 Now, so far as the reliance placed upon the decision of the Hon’ble Supreme Court in the case of P.V.S. Beedies Pvt. Ltd. (Supra) and the decision of the Division Bench of this Court in the case of N.K. Industries Ltd. (Supra) by Shri Desai, learned Advocate appearing on behalf of the Revenue is concerned, it is true that the information given by the audit party and/or on the audit objection, can be used for the purpose of reopening of the assessment. However, for that there must be formation of the opinion by the Assessing Officer and/or Assessing Officer independently has reason to believe that the income chargeable to tax has escaped assessment. Even in a given case it may happen that initially the Assessing Officer might have opposed the audit objection by giving reply to the audit party on the audit objection as normally it is the human tendency to stick to what is held and/or decided. However, subsequently, there can be a formation of the opinion by the Assessing Officer on rethink of the entire issue and even considering the audit objection and may form an independent opinion and/or may have a reason to believe independently that the income chargeable to tax has escaped assessment. However, in a case like this where even while sending the proposal to the higher authority to grant the approval for initiation of the reassessment proceedings, the Assessing Officer still maintain that audit objection raised by the audit party is not valid and/or correct. Therefore, as such it cannot be said that the Assessing Officer had independently formed an opinion and/or had reason to believe independently that the income chargeable to tax has escaped assessment. From the correspondence between the Assessing Officer and the higher authority it appears that though the Assessing Officer maintains that the audit objection raised by the audit party is not correct, however as the amount involved is very high as mentioned by the audit party and to safeguard the interest of the Revenue and the guidelines issued the reassessment proceedings have been initiated. Therefore, as such the formation of the opinion by the Assessing Officer that the income chargeable to tax has escaped assessment has been vitiated and therefore, the impugned reopening of the assessment cannot be sustained and the same deserves to be quashed and set aside.

5.8 Now, so far as the submission of Shri Desai, learned advocate appearing on behalf of the revenue that as now, the order of assessment/reassessment under section 143(3) (of Income Tax Act, 1961) r/w section 147 (of Income Tax Act, 1961) has been passed and therefore, the present petition may not be entertained is concerned, it is required to be noted that as such, the reassessment proceeding has been passed during the pendency of the present petition. Even otherwise, when the reopening of the assessment is found to be invalid and not justifiable and the same is solely based on the audit objection raised by the audit party, this is a fit case to exercise the powers under Article 226 of the Constitution of India.

6. In view of the above and for the reasons stated above, present petition succeeds. Impugned notice dated 13.8.2013 issued under section 148 (of Income Tax Act, 1961) to reopen the assessment for AY 2010-11 is hereby quashed and set aside and consequently the reassessment proceedings for AY 2010- 11 are hereby quashed and set aside and the consequential reassessment order dated 13.1.2015 passed under section 147 (of Income Tax Act, 1961) for AY 2010-11 is hereby quashed and set aside.. Rule is made absolute accordingly. However, in the facts and circumstances of the case, there shall be no order as to costs.

(M.R.SHAH, J.)

(S.H.VORA, J.)

×

Similar Ripples

Questions

Court Quashes Income Tax Reassessment Based Solely on Audit Objections

Write your CommentSimilar Posts

Generic

- Reportdata/3768.pdf