Court Quashes Income Tax Reassessment Notice, Citing Lack of Independent Reason…

Full News

Court Quashes Income Tax Reassessment Notice, Citing Lack of Independent Reasoning

Court Quashes Income Tax Reassessment Notice, Citing Lack of Independent Reasoning

A company called Torrent Power S.E.C. Ltd. challenged a notice from the Income Tax Department. The tax folks wanted to reopen an old assessment, but the company said, "Hold up, you can't do that!" The High Court agreed with the company and cancelled the notice. Pretty big win for Torrent Power.

Get the full picture - access the original judgement of the court order here

Case Name:

Torrent Power S.E.C. Ltd. Vs Commissioner of Income Tax (High Court of Gujarat)

Special Civil Application No. 5692 of 2006

Date: 2nd December 2016

Key Takeaways:

1. Tax authorities can't reopen assessments solely based on audit objections.

2. There must be an independent formation of opinion by the Assessing Officer.

3. The court emphasized the importance of proper reasoning in tax reassessment notices.

4. This case reinforces taxpayer protections against arbitrary reassessments.

Issue:

The main question here was: Can the Income Tax Department reopen an assessment based solely on an audit objection without forming an independent opinion that income has escaped assessment?

Facts:

1. Torrent Power filed its income tax return for the assessment year 2000-01.

2. The return was processed and accepted under Section 143(1) (of Income Tax Act, 1961) on 28.02.2001.

3. Later, an audit party raised objections about a subsidy amount of Rs. 30.66 crores.

4. The company provided explanations and details to the tax department.

5. About 18 months later, on 03.09.2004, the Assessing Officer issued a notice under Section 148 (of Income Tax Act, 1961) to reopen the assessment.

6. The company objected, saying the reopening was based solely on the audit objection.

Arguments:

Torrent Power's side:

- The reopening was based only on the audit objection, not on the Assessing Officer's independent opinion.

- The subsidy was properly accounted for in their books.

- The Additional Commissioner had already clarified that no action was needed on the audit objections.

Tax Department's side:

- The original assessment was under Section 143(1) (of Income Tax Act, 1961), so they didn't get to examine the accounts in detail.

- They needed to verify if the subsidy was properly accounted for.

- The subsidy wasn't reflected in the balance sheet.

Key Legal Precedents:

The court relied on two important cases:

1. Raajratna Metal Industries Ltd vs. Assistant Commissioner of Income Tax (2014) 49 Taxmann.com 15 (Gujarat)

2. National Construction Co vs. Joint Commissioner of Income Tax, Gandhidham Range (2015) 60 Taxmann.com 29 (Gujarat)

These cases established that reassessments can't be based solely on audit objections without independent reasoning.

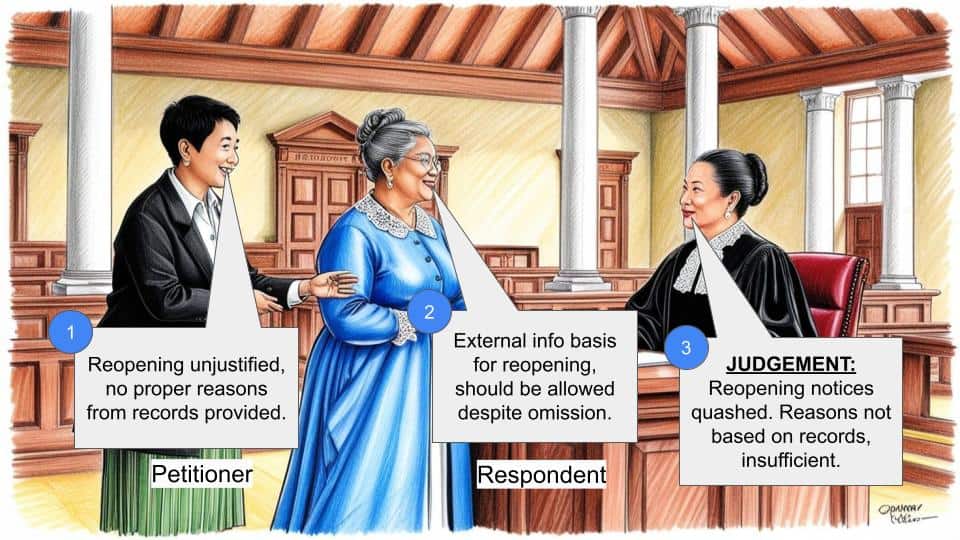

Judgement:

The court sided with Torrent Power. They said:

1. The reopening notice was based on the same grounds as the audit objection.

2. There was no evidence of independent reasoning by the Assessing Officer.

3. The tax department didn't deny or dispute these points in court.

4. Based on this, the court quashed (cancelled) the reassessment notice under Section 148 (of Income Tax Act, 1961).

FAQs:

1. Q: What does this mean for other taxpayers?

A: It reinforces that tax authorities need solid, independent reasons to reopen old assessments, not just audit objections.

2. Q: Can the tax department never act on audit objections?

A: They can, but they need to form their own independent opinion based on the objections, not just repeat them.

3. Q: Why is this case important?

A: It protects taxpayers from arbitrary reassessments and ensures tax authorities do their due diligence.

4. Q: Could the tax department have won if they had better evidence?

A: Possibly, if they could show they had formed an independent opinion beyond the audit objections.

5. Q: Does this mean the company didn't have to pay the tax on the subsidy?

A: Not necessarily. It just means the reassessment process was invalid. The original assessment stands.

1.0. By way of this petition under Article 226 of the Constitution of India, the petitioner has prayed for an appropriate writ, direction and order to quash and set aside the impugned notice issued under Section 148 (of Income Tax Act, 1961) dated 03.09.2004, by which, the Assessing Officer has sought to reopen the assessment for AY 200001 under Section 147 (of Income Tax Act, 1961).

2.0. The facts leading to the present Special Civil Application in nutshell are as under:

2.1. That the petitioner company incorporated under the Companies Act (hereinafter referred to as the “assessee”) filed its return of income declaring total income of Rs.8,41,95,356/. The said return was processed and accepted under Section 143(1) (of Income Tax Act, 1961) on 28.02.2001. It appears that thereafter the audit party raised audit objection with respect to the gross receipt shown in P & L account with respect to subsidy amount received from the Government. That having received the remarks from the audit party, the Assessing Officer vide communication dated 2.05.2002 called for various details from the Assessee regarding subsidy showing nature, amount payable by government, amount payable to the government, amount sanctioned and received and the treatment given to the transaction in the books of accounts of the assessee, liability on account of the government duty and the tax on sale of electricity, details of gross earning and adjustments of subsidy etc. in response to certain queries raised by the auditors from the office of the Accountant General. That the assessee furnished all the details called for by the Assessing Officer. That the Additional Commissioner of Income Tax, Range4, Surat immediate superior of the Assessing Officer vide his communication / letter dated 2.12.2002 addressed to the Commissioner of Income Tax,II, Surat clarifying that on examination of books of accounts of the assessee it was found that (1) the gross sales of electricity, including the amount of subsidy had been credited in the books of accounts of the assessee and therefore, the sales includes subsidy and there is no need to add it further to the sales and in P & L account of the assessee;(2) No such subsidy was borne by the Government in FY 199900 and hence the objections of the audit for FY 199900 (AY 200001) stands infructuous. That the subsidy on the account of equalization of tariff was discontinued w.e.f. 1.4.1999. The amount of Rs. 30.66 crores was only a release of outstanding subsidy during AY 200001 pertaining to earlier years; (3) Therefore, the objections raised by the Audit Party cannot survive more so when there was no discrepancy in the accounting system of the assessee with regard to the accounting of subsidy. It was stated that therefore, the observation of the audit report may be treated as complied with and no remedial action was called for on the merits of the case.

2.2. That after a period of approximately 18 months, Assessing Officer issued the impugned notice dated 03.09.2004 under Section 148 (of Income Tax Act, 1961), reopening the assessment for AY 200001. That in reply to the aforesaid notice, the assessee vide letter dated 28.09.2004, asked the Assessing Officer to treat the original return filed as return filed in response to the notice under Section 148 (of Income Tax Act, 1961). At the request of the assessee, Assessing Officer supplied the reasons recorded to reopen the assessment for AY 200001 vide communication dated 23.02.2005. The reasons recorded to reopen the assessment is as under:

“The reasons to believe that income chargeable to tax has escaped assessment:

The power tariff of the assessee company was higher than the power tariff of the Gujarat Electricity Board (GEB). As a result of the agitation of the consumers of the assessee company, the Government of Gujarat asked the assessee company to charge the consumers at par with the rate of GEB and the Government of Gujarat agreed to reimburse the difference to the assessee company by way of subsidy. From the records, it is seen that the assessee had received the subsidy from the Government of Gujarat during the previous year amounting to Rs.3066 lakhs.

The subsidy amounts have not been distinctly shown in the profit and loss account of the assessee company. The records neither reveal that the amount of subsidy had really passed on to the assessee nor reveal that the consumers were charged at lower rate and the gross receipt was inclusive of subsidy amount. Thus, the subsidy amount has not been offered as income of the assessee. In the given position of facts, I have reason to believe that income to the extent of Rs.3066 lakhs has escaped assessment.

Issue notice u/s 148 (of Income Tax Act, 1961).”

2.3. That thereafter, the assessee through its authorized representative raised various objections both on jurisdiction and on merits against the reopening of the assessment, vide communication / letter dated 09.03.2005. It was the specific case on behalf of the assessee that assessment is reopened solely on the objection raised by the audit party and that there is no independent satisfaction of the Assessing Officer that income has escaped assessment. The detailed objections were also made on merits. Therefore, it was requested to drop the reassessment proceedings. That vide letter dated 08.09.2005, the Assessing Officer disposed of the objection raised by the assessee and inter alia held that reopening is valid and within the jurisdiction. That thereafter, vide letter dated 30.09.2005, the assessee once again pointed out reopening is bad in both on law as well as on facts relying upon the chronology of events for various earlier assessment years and inter alia pointed that Assessing Officer has made some factually erroneous statement and observations contrary to the evidences placed on record. It was also submitted that subsidy received from the government has been properly accounted in the books of account. Therefore, it was requested that reopening proceedings be dropped. However, reassessment proceedings have not been dropped. Hence, the petitioner has preferred present Special Civil Application challenging the impugned notice under Section 148 (of Income Tax Act, 1961).

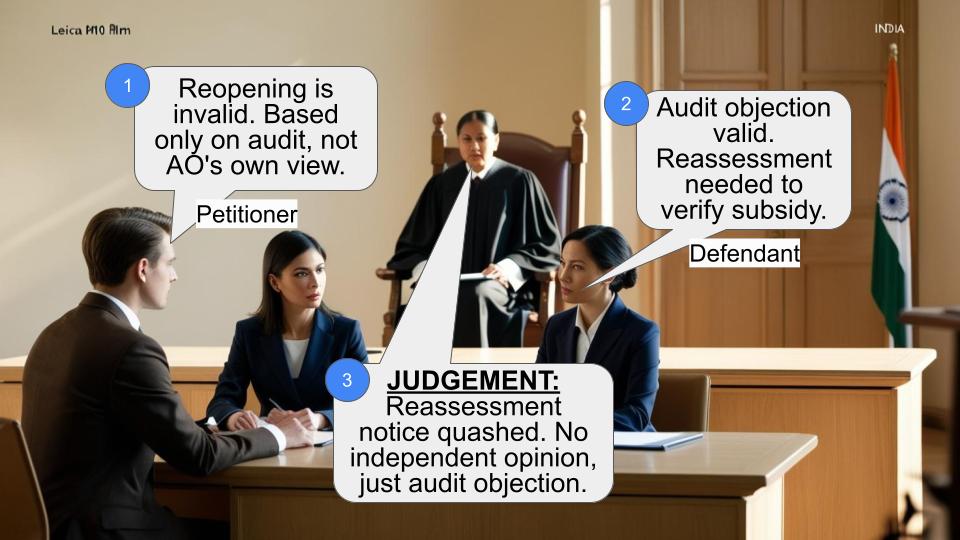

3.0. Shri S.N. Soparkar, learned counsel for the petitioner has vehemently submitted that the impugned notice under Section 148 (of Income Tax Act, 1961) to reopen the assessment for AY 200001 is bad in law both on jurisdiction as well as on merits. It is vehemently submitted by Shri Soparkar, learned counsel for the petitioner that as such impugned notice under Section 148 (of Income Tax Act, 1961) is not sustainable under law as the same is on the audit objection raised by the audit party only and that there is no independent opinion by the Assessing Officer income has escaped assessment. It is submitted that on the contrary after considering the material on record it was submitted by the assessee to the Additional Commissioner of Income Tax, Range 4 Surat, communicated to the Commissioner of Income Tax, II, Surat that the objections raised by the Audit Party do not survive more so when there is no discrepancy in the accounting system of the assessee with regard to the accounting of subsidy. It is submitted that no remedial action was called for on the merits of the case. It is submitted that despite in the objections, it was specifically pointed out that solely relying upon the audit objection raised by the audit party and without any independent opinion formed by the AO that the income has escaped assessment, by disposing of the objection, the Assessing Officer has not deliberately not dealt with the same.

3.1. It is further submitted by Shri Soparkar, learned counsel for the petitioner that notice can be issued under Section 148 (of Income Tax Act, 1961) if the Assessing Officer has reason to believe that the income chargeable to tax has escaped assessment. It is submitted that belief must be that of honest and reasonable based on reasonable ground but not a mere change of opinion or suspicion. It is submitted that belief must lead to a conclusion that income has escaped assessment. It is submitted that in the present case there cannot be any reason to believe that some income has escaped assessment for the simple reason that there is nothing on record to suggest that the assessee has not reflected the subsidy from the Government of Gujarat in its books of accounts and / or hidden the particulars of subsidy so as not to reflect the same in its gross sales. On the contrary, as per the audited accounts the subsidy outstanding for recovery from Government of Gujarat was shown separately under the schedule of “Sudry Debtors”. It is submitted that as such the subsidy from the income was shown in the total income, in the books of account, however the same was adjusted against the dues of the State Government such as electricity dues etc. It is submitted that therefore, there cannot be any reason to believe that the same income has escaped assessment.

Making above submissions and relying upon the decisions of this Court in the case of Raajratna Metal Industries Ltd vs. Assistant Commissioner of Income Tax reported in (2014) 49 Taxmann.com 15(Gujarat) as well as in the case of National Construction Co vs. Joint Commissioner of Income Tax, Gandhidham Range reported in (2015) 60 Taxmann. Com 29(Gujarat), it is requested to allow the present Special Civil Application by quashing and setting a side the impugned notice.

4.0. Shri Nitin Mehta, learned counsel has appeared on behalf of the Revenue. At the outset, it is required to be noted that though the present Special Civil Application is of the year 2006 till date no reply has been filed either opposing the present petition and / or disputing the averments made in petition. Shri Mehta, learned counsel for the revenue has vehemently submitted that the original assessment order was under Section 143(1) (of Income Tax Act, 1961) and therefore, the Assessing Officer had no occasion to consider and / or go through in detailed the books of account / P & L account. It is submitted that therefore, the case on behalf of the assessee that amount of subsidy / repaid to the extent of Rs. 30.66 crores has been duly accounted for any gross receipt was required to be verified. It is submitted that on verification of the details filed along with submissions / objection it has been found that subsidy / repaid receivable is nowhere reflected in the balance sheet. It is submitted that therefore, reopening of the assessment for 200001 is just and proper.

Making above submissions, it is requested to dismiss the present Special Civil Application.

5.0. Heard the learned advocates for the respective parties at length. At the outset, it is required to be noted that assessment for AY 200001 is reopened by impugned notice. From the reasons recorded, it appears that the assessment is reopened with respect to assessee received subsidy from the income during the previous year amounting to Rs.30.66 crores on the ground that the said subsidy amount has not been distinctly shown in the profit and loss account of assessee company. However, it is required to be noted that according to the assessee reopening is solely on the audit objection raised by the audit party and there is no independent formation of opinion by the Assessing Officer that the income had escaped the assessment. The said objection was raised against the reasons recorded in the notice and averments in the present petition, however the aforesaid has not been denied or disputed. From the material on record, it appears that after audit objections were received, the Additional Commissioner of Income Tax, Range4, Surat asked the necessary particulars / documentary evidence on the objection raised by the audit party. The assessee furnished necessary documentary evidence including books of accounts etc. and after having satisfied with respect to the accounting system of the assessee with regard to the accounting of the subsidy, Additional Commissioner of Income Tax, Range 4 Surat, communicated to the Commissioner of Income Tax, II, Surat that the objections raised by the Audit Party do not survive and / or observation made by the audit party may be treated as complied with and no remedial action was called for on the merits of the case. It is required to be noted that the assessment is reopened on the very ground on which the objections raised by the audit party. Under the circumstances and more particularly the allegations that the assessment is reopened solely on the objection raised by the audit party and there is no independent formation of opinion by the Assessing Officer that the income has escaped assessment, have not been denied or disputed, the impugned notice under Section 148 (of Income Tax Act, 1961) cannot be sustained. The decisions of this Court in the case of Raajratna Metal Industries Ltd (supra) and National Insurance Co (supra) shall be squarely applicable to the facts of the case on hand. Under the circumstances on the aforesaid ground alone, the impugned notice deserves to be quashed and set aside.

6.0. In view of the above and for the reasons stated above, present petition succeeds. The impugned notice issued under Section 148 (of Income Tax Act, 1961) dated 03.09.2004 to reopen the assessment proceedings deserves to be quashed and set aside and is hereby quashed and set aside. Rule is made absolute to the aforesaid extent. No costs.

sd/

(M.R. SHAH, J.)

sd/

(B.N. KARIA, J.)

×