Court Quashes Income Tax Reassessment Notice, Citing Improper Reopening Procedu…

Full News

Court Quashes Income Tax Reassessment Notice, Citing Improper Reopening Procedure

Court Quashes Income Tax Reassessment Notice, Citing Improper Reopening Procedure

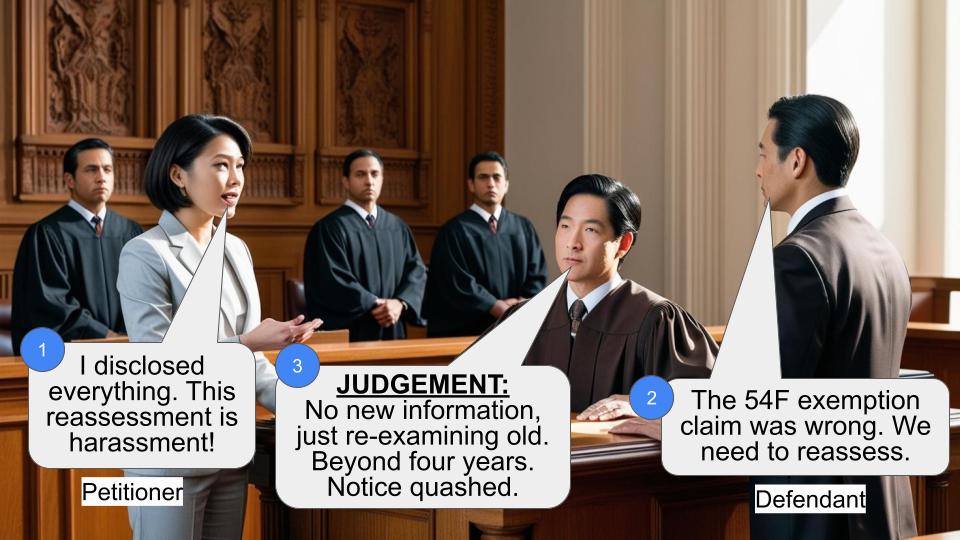

This case involves Sahjanand Medical Technologies Pvt. Ltd. challenging a notice issued by the Assistant Commissioner of Income Tax to reopen their assessment for the 2010-11 tax year. The High Court ruled in favor of the company, quashing the reassessment notice due to improper reopening procedures and lack of independent belief by the Assessing Officer that income had escaped assessment.

Get the full picture - access the original judgement of the court order here

Case Name:

Sahjanand Medical Technologies Pvt. Ltd. Vs Assistant Commissioner of Income Tax & Another (High Court of Gujarat)

Special Civil Application No. 3399 of 2016

Date: 15th June 2016

Key Takeaways:

1. Reopening of assessment cannot be based on a mere change of opinion.

2. The Assessing Officer must have an independent belief that income has escaped assessment.

3. Audit objections alone cannot be the basis for reopening an assessment.

4. Detailed scrutiny during original assessment prevents reopening on the same grounds.

Issue:

Was the notice for reopening the assessment of Sahjanand Medical Technologies Pvt. Ltd. for the Assessment Year 2010-11 valid and justified?

Facts:

- Sahjanand Medical Technologies Pvt. Ltd. filed their income tax return for the 2010-11 assessment year.

- The Assessing Officer conducted a scrutiny assessment and passed an order on 26.03.2013.

- On 24.12.2014, the Assessing Officer issued a notice to reopen the assessment.

- The reopening was based on three main grounds related to sales returns, bad debts, and provisions for doubtful debts.

- The company challenged this notice through a petition to the High Court.

Arguments:

Petitioner (Sahjanand Medical Technologies):

- The notice was issued at the instance of the Audit Party, not based on the Assessing Officer's independent decision.

- All claims were scrutinized in detail during the original assessment proceedings.

- Reopening within four years based on a mere change of opinion is not permissible.

Revenue:

- The Assessing Officer recorded valid reasons for issuing the notice for reopening.

- The notice was issued within four years from the end of the Assessment Year.

Key Legal Precedents:

1. Cadila Healthcare Ltd. v. Deputy CIT (334 ITR 420)

2. Adani Exports v. Dy. CIT (240 ITR 224)

3. Indian & Eastern Newspaper Society v. CIT (119 ITR 996)

These cases establish that reopening cannot be based on a mere change of opinion or solely on audit objections.

Judgement:

The High Court ruled in favor of Sahjanand Medical Technologies, quashing the reassessment notice. The court found that:

1. The Assessing Officer had thoroughly examined the claims during the original assessment.

2. The Assessing Officer did not have an independent belief that income had escaped assessment.

3. The notice was issued under pressure from the Audit Party, against the Assessing Officer's own judgment.

FAQs:

1. Q: Why did the court quash the reassessment notice?

A: The court found that the Assessing Officer didn't have an independent belief that income had escaped assessment and was acting under pressure from the Audit Party.

2. Q: Can an assessment be reopened based on audit objections alone?

A: No, as per this judgment and previous precedents, reopening cannot be solely based on audit objections.

3. Q: What is the significance of the four-year time limit mentioned in the case?

A: Generally, assessments can be reopened within four years more easily. However, even within this period, reopening cannot be based on a mere change of opinion.

4. Q: How does this judgment impact future tax assessments?

A: It reinforces the principle that Assessing Officers must have independent reasons to believe income has escaped assessment before issuing reopening notices.

5. Q: What sections of the Income Tax Act were relevant in this case?

A: The case primarily dealt with Section 147 (of Income Tax Act, 1961), which pertains to income escaping assessment and the procedure for reassessment.

1. In this petition, the petitioner has challenged a Notice dated 24.12.2014 issued by respondent no. 1 – Assessing Officer seeking to reopen the assessment of the petitioner for the Assessment Year 2010-11.

1.1. The brief facts are as under :

1.2. The petitioner is a Company registered under the Companies Act and is engaged in the business of manufacturing specialized medical equipments. For the Assessment Year 201011, the petitioner had filed return of income, which was taken by the Assessing Officer for scrutiny. In the Assessment Order dated 26.03.2013, the Assessing Officer made several additions and disallowances. In order to reopen such assessment, impugned notice came to be issued. The Assessing Officer had recorded reasons for issuance of such notice, which reads as under:

“The assessee company is engaged in manufacturing of medical equipments, especially manufacturing of cardio vascular stent. Filed his return of income for the A.Y. 2010 11 on 02.09.2010 declaring income of Rs.3,97,37,491/. Assessment u/s. 143(3) (of Income Tax Act, 1961) was completed on 26.03.2013 by determining total income of Rs.5,26,15,210/.

1. It was noticed from Profit & Loss a/c that net sales of Rs.42,12,62,060/ was shown after deducting the provisions of sales return of Rs.1,63,80,000/ from sales. As per I.T. Act, provision made in the accounts only for an accrued or known liability is admissible deduction. Thus, deduction allowed for provision of sales return was irregular. The same was required to be disallowed and added back in the assesse's total income. By not doing so, resulted in underassessment of income of Rs.1,63,80,000/.

2. As per Section 36(1)(vii) (of Income Tax Act, 1961), the amount of any bad debt or part thereof which is written off as irrecoverable in the accounts of assessee for the previous year is admissible deduction. Further as per explanation below of Section 36(1)(viii) (of Income Tax Act, 1961), for the purpose of this clause, any bad debt or part thereof written off as irrecoverable in the accounts of the assessee shall not include any provision for bad and doubtful debts made in the accounts of the assessee. Scrutiny of records revealed from the computation of income that the assessee had claimed and allowed bad debt of Rs.3,37,34,810/. However, the assessee had written off bad debt from the provision of bad debt and doubtful debts made for earlier years i.e. instead of credit of debtor's account and assessee had credited it from provision of bad and doubt debts. Thus, the bad and debt written off of Rs.3,37,24,810/ from provision of bad and doubtful debts was irregular. This has resulted into under assessment of Rs.3,37,24,810/.

3. Scrutiny of records revealed that the assessee had claimed and allowed provision for doubtful debts/ written back/ transfer to bad debts of Rs.2,78,47,717/ and provision for doubtful loan, advances and deposits of Rs.73,77,830/ totalling Rs.3,52,25,547/. As per the IT Act no such provisions were admissible. This has resulted into under assessment of Rs.3,52,25,547/.

4. In view of the above, I have reason to believe that the income to the tune of Rs.8,53,30,357/ chargeable to tax has escaped assessment within the meaning of Section 147 (of Income Tax Act, 1961) for A.Y. 201011.”

2. Upon receipt of the reasons recorded by the Assessing Officer, the petitioner raised objections to the process of reopening under a communication dated 09.01.2016. Such objections, were however, rejected by the Assessing Officer by order dated 05.02.2016. Hence, the petition.

3. From the reasons recorded by the Assessing Officer, it could be gathered that he had pressed in service three grounds in order to resort to the process of reopening of the assessment. Briefly stated, these grounds were (1) that the assessee had claim deduction of Rs.1.63 crores (rounded off) under the provision of sales return. According to the Assessing Officer, the liability was not known nor accrued and the same therefore could not be claimed as deduction; (2) that the assessee had wrongly claimed bad debt of Rs.3.37 crores (rounded off), which claim was not eligible in terms of Section 36(1)(viii) (of Income Tax Act, 1961) (the “Act” for short) and (3) that the assessee had claimed doubtful debts, doubtful loans, advances etc., totalling into 3.52 crores which was not a valid claim.

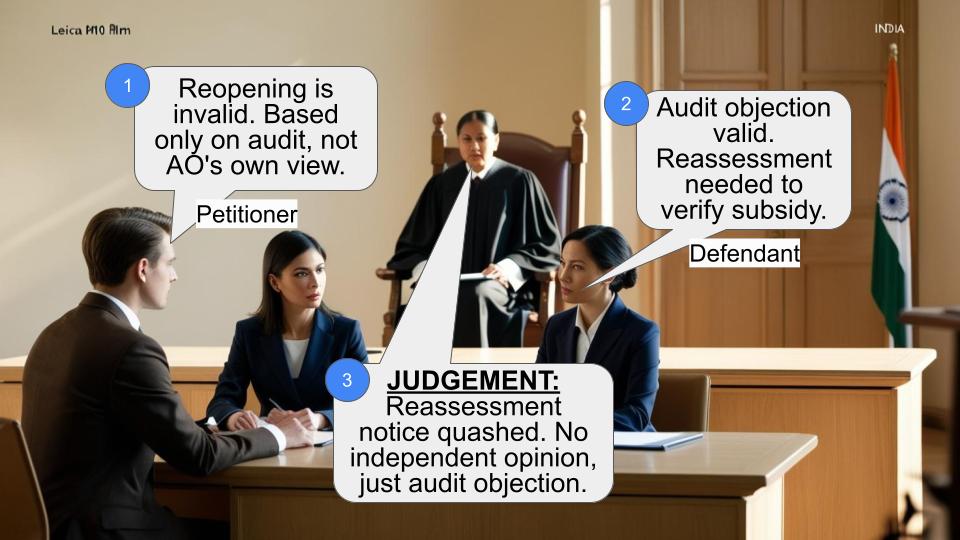

3.1. On the basis of materials on record, learned counsel Shri R.K. Patel for the petitioner raised mainly two contentions; firstly, that the notice for reopening was issued under the instance of Audit Party and that therefore, there was no independent decision of the Assessing Officer that income chargeable to tax had escaped assessment. His second contention was that all three claims were scrutinized in detail during the original assessment proceedings and, therefore, re- examination of such claims even within four years from the end of the relevant assessment year, would not be permissible, on the mere change of opinion.

4. On the other hand, learned counsel Shri Sudhir Mehta for the Revenue opposed this petition contending that the Assessing Officer has recorded valid reasons for issuing notice for reopening. Notice has been issued within a period of four years from the end of Assessment Year.

5. We may advert to second and third grounds recorded by the Assessing Officer in his reasons. In so far as claim of bad debts to the extent of 3.37 crores in terms of Section 36(1)(vii) (of Income Tax Act, 1961) is concerned, we may notice that during the original scrutiny of the assessment proceedings, the Assessing Officer had required the assessee to provide multiple details. In a communication dated 10.12.2011, the assessee had conveyed to the Assessing Officer, as under :

“8. The party wise details of bad debts written off are separately enclosed. We are also enclosing the copy of ledger account of the parties for the period when actual transactions were made.

10. Details of provision for debts, provisions for doubtful loans and advances and provision are separately enclosed. The provision for deposits, provisions for insurance claim receivable are made adhoc on the basis of past experience. However, all the provisions are added back to total income in computation of total income.”

5.1. In a further communication dated 07.12.2012 with respect to this claim, the Assessing Officer called upon the assessee to provide the following details :

“2. In this connection, you are requested to furnish the following details/ information/ explanation, which are required for completion of assessment proceedings:

(i) Furnish details of bad debts written off in the previous year relevant to A.Y. 201011, i.e. name and address of the parties and nature of transaction made by you with the said party along with documentary evidence in A.Y. 200910.

(ii) During the year under consideration, you had debited an amount of Rs.4,50,32,315/ as Bad Debt Expenses for which you have submitted name and amount of bad debt written off. From the said details it is found that during the year you have written off bad debt only Rs.3,37,24,816/. You are, therefore, requested to showcause as to why the differential amount of Rs.1,13,07,499/ should not be disallowed and added to your total income.”

5.2. In response to such a query, the petitioner on 18.12.2012 wrote to the Assessing Officer as under :

“1. The details of bad debts written off during the year under consideration are as under :

Name and address of the Party Amount (in Rs.) Medline Surgicals, Kolkata 1, Basanta Bose Road, Kolkata – 700 026 (India) 152,100

Ruby General Hospital, Kolkata KasbaGolpark, E.M. Bypass, Kolkata, West Bengal – 700 107 (India)

77,310

Nayyar Heart Institute, Amritsar 3 Dasunda Singh Road, Lawrence Road Extension, Amritsar, 143001

402,000

Indraprastha Apolla Hospital, Delhi DelhiMathura Road, National Highway2, SaritaVihar, JasolaVihar New Delhi 10076

400,000

Maya Hospital, Lucknow Gomti Nagar, Lucknow, Uttar Pradesh

138,000

Bangalore Hospital, Bangalore 11, 17th A Cross Btwn 11th & 12th Main, Malleshwaram Malleshwaram, Bangalore, KarnatakaIndia.

35,000

K.L.E.S. Heart Found, (Belgaum) Bangalore Nehru Nagar, Belgaum, Karnataka – India.

704,750

Manipal Heart Foundation, Bangalore 98, HAL Airport Road, Bangalore, KA560017

50,500

NarayanaHrudalaya, Bangalore No.258/A, Bommasandra Industrial Area, Anekaltaluk Bangalore, Karnataka560099

157,000

Omega Pharmacy (Mangalore), Bangalore MAHAVERR CIRCLE, Mangalore, Karnataka

599,500

Shree Jayadeva Institute of Cardiology, Bangalore K.R. Hospital Campus, Mysore, Karnataka, India

464,000

Trinity Heart Foundation, Bangalore 27, Srerammandira Road, Near RV Teacher College Circle, 560004, Basavanagudi, Bangalore, Karnataka

1,163,000

Sigma Hospital, Hyderabad Aplic Colony Ida,234/1, Jeedimetla,

950,000 Jeedimetla PIIC Colony, Jeedimetla, Hyderabad.

Usha Cardiac Centre (Vijayawada) Hyderabad Rhoda Mistri Nagar, Hyderabad, Andhra Pradesh

26,909

Cardio Medical Co. Syria SalhiaShahadastr, P.O. Box 10255, SouqAlmarad Al Nahhas Bldg., Damascus, Syria

6,758,008

Fereydooni Medical Supplies Iran Apt. 4, No.35, MohajerAlley, Irashahr Street, Tehran – Iran

8,608,614

Scitech Medical Products, Brazil Rua 53, No220,QdB17,Lt.22, JardimGoias Goiania Go – Brail Zip Code 74,810210.

11,984,460

SAL Hospital, Ahmedabad Opp. Doordarshan,DriveinRoad, Ahmedabad380 054 Gujarat, India.

525,665

Balaji Hospital, Mumbai Victoria Road, Cross Lane III, Byculla (E) Mumbai, MH 400 027

65,000

K.E.M. Hospital, Mumbai Acharya Donde Marge, Parel East, Mumbai, Maharashtra 400012

58,000

Reliance (H.N.Hospital) Mumbai Padmashri Gordhan Bapa Chowk, Rajaram Mohan Roy Road, Charni Road, Mumbai

405,000

Total > 33,724,816

5.3. Once again, under communication dated 15.03.2013, the petitioner justified this claim as under :

“The allowable expenses in respect of business incomes are covered under Section 30 (of Income Tax Act, 1961) to 37 of the Act, Section 36(1)(vii) (of Income Tax Act, 1961), specifically dealt with allowable expenses for bad debts or in other words the bad debts are allowable if the assessee comply with the conditions laid down in said Section. The Section 36(1)(vii) (of Income Tax Act, 1961), states as under :

“(vii) subject to the provision of subsection (2), the amount of (any bad debt or part thereof which is written off or irrecoverable in the accounts of the assessee for the previous year)”.

The proviso is not applicable as the same is dealt with bad debts claimed under Section 36(1)(vii) (of Income Tax Act, 1961). The assessee is also not covered under Section 36(2) (of Income Tax Act, 1961).

Hence, for claiming expenses under bad debts u/s. 36(1) (of Income Tax Act, 1961) (vii) the assessee has to written off the debts as recoverable in the accounts for the previous year. The assessee has written off the debts as irrecoverable in the books of accounts and eligible for claiming deduction u/s. 36(1) (of Income Tax Act, 1961) (vii) of the Act, It is immaterial under income tax, whether the assessee has taken necessary permission from RBI or not, however, the assessee has followed the procedure prescribed by RBI and the same is dealt in next para.

2. In case of written off any debts, the assessee has to inform to bank (authorised dealer) and bank inform to the RBI. In case RBI requires any clarification it also calls through bank. The assessee company has submitted the letters to the bank for writing off the debts in due course. We have also informed the bank for writing off loans and advance through letter dated June 15, 2009. The assessee company has received letter from Reserve Bank of India dated August 18, 2009 through bank. The assessee has replied the same. The copy of all correspondence regarding this is enclosed here with for your ready reference. We are also enclosing the copy of letter for writing off debts given to bank and the assessee company has not received any communications from bank or RBI in this matter.”

5.4. It was only after such detailed, minute scrutiny that the Assessing Officer, in the order of assessment, had made partial dis- allowance of the petitioner's claim of deduction of bad and doubtful debts. For all these reasons, therefore, the Assessing Officer cannot be permitted to reopen the assessment, on this very ground, since any such reopening, would be based on mere change of opinion.

5.5. Regarding the third ground recorded in the reasons by the Assessing Officer, we may recall, it pertains to assessee's claim of bad debt and of doubtful loans and advances. In this context, the assessee in the letter dated 10.12.2011 to the Assessing Officer had conveyed as under :

10. Details of provision for debts, provisions for doubtful loans and advances and provision are separately enclosed. The provision for deposits, provisions for insurance claim receivable are made adhoc on the basis of past experience. However, all the provisions are added back to total income in computation of total income.”

5.6. Thus, even this claim of the assessee came up for consideration before the Assessing Officer in the original assessment proceedings. Here again, the Assessing Officer in the final order of assessment had made partial disallowances. Thus, this claim was also scrutinized by the Assessing Officer in the original assessment proceedings.

6. Coming to the first ground mentioned in the reasons, we may recall, it pertains to deduction of the provision of sales return of Rs.1.63 crores claimed by the assessee. According to the Assessing Officer, this was neither accrued nor a known liability and was therefore, not an admissible deduction. In this context, the assessee contends that even this claim had come up for consideration before the Assessing Officer and only upon being satisfied about the validity of the claim, no adjustment was made. The learned counsel for the petitioner drew our attention to objections raised by the assessee to the notice of reopening issued by the Assessing Officer. In the objections, the assessee had made detailed reference to the materials on record of the original assessment proceedings and also pointed out the documents under which such claim was made and not rejected by the Assessing Officer.

It was pointed out that the company was maintaining batch wise complete record of its products and also kept track record of the goods lying with various distributors. Upon coming to know that the material in some products was defective and was causing problem for the user, it had recalled the material on 22.03.2010 from the market. Thus, the company knew the exact quantity of the material recalled. This was thus, not estimated but known ascertained liability. Since the distributors would return the goods, the assessee company would receive no payments for the same. The assessee had, therefore, not made any adhoc provision of sale return, but had made specific provision on the basis of goods recalled.

6.1. In this context, the learned counsel for the petitioner had also argued that the Assessing Officer had not acted independently, but at the behest and at the instance of Audit Party.

7. We notice that there is no direct evidence to demonstrate before us that this claim of the provision of sale return of Rs.1.63 crores came up for direct discussion before the Assessing Officer during the original assessment proceedings. However, in the context of the petitioner's contention regarding audit objections, we had summoned the original file of the Department. Perusal of the file would show that on 24.09.2014, the Audit Party had discussed this claim of the assesse and had referred it as a major irregularity in granting the same. In this note prepared by the Audit Party, we notice that this issue was taken up by the Audit Party with the Assessing Officer, who had replied that the assessee company is engaged in manufacturing stent and had imported certain parts, which were used in manufacturing the final product which was supplied to the distributors. There were huge product complaints from the hospitals using the product. The company, therefore, stopped using the catheters which were found to be defective and returned unused catheters imported from abroad and also recalled the defective material from the market. Such material was received and destroyed because it was not safe for human use and that therefore, the liability was ascertained.

7.1. The Assessing Officer, thus, clearly did not agree to the view point of the Audit Party that the claim was irregularly granted. In fact,in his opinion, after going through the detailed explanation, the same was correctly allowed. Despite this, it appears that the Audit Party insisted upon corrective measures being taken by the Assessing Officer.

The Assessing Officer, therefore, on 30.12.2013 wrote to the Director, Principal Director, Audit (Central) and once again gave detailed reasons why, in his opinion, when the company had recalled the material, it was ascertained liability or known liability and the same therefore, cannot be added back to the profit of the company. It was, in this background, that the Assessing Officer once again wrote to the Commissioner of IncomeTax on 28.02.2014 completely disagreeing with the Audit Party and after giving detailed reasons, stated as under:

“When company recall the material, it is certain liability or known liability for which provision is made and as per the explanation [1] (c ) of Section 115JB (of Income Tax Act, 1961) “the amount or amounts set aside to provisions made for meeting liabilities, other than ascertained liabilities;”, need to be added in book profit. However, the provisions made for sales return are ascertained liabilities, Therefore, the same cannot be added back to book profit while calculating MAT.

4. In view of the facts and circumstances of the case, the objection raised by the Revenue Audit is not acceptable. However, as per the Instruction No. 16 dated 31.10.2013 any remedial action under the IncomeTax Act is to be taken within six months of the receipt of LAR of the Audit Party. The remedial action in this case is possible u/s.154 (of Income Tax Act, 1961)/147/263. However, the most suitable remedial action would be reopening u/s.147 (of Income Tax Act, 1961).”

8. It can thus, be clearly seen that the Assessing Officer was completely against the principle of taxing these receipts. The Audit Party was of the opinion that the deduction for provision of sale return was claimed for liability which had not yet arisen nor ascertained. The Assessing Officer was steadfast in his belief that the liability had accrued and it was also ascertained.

9. Under the circumstances, as per the settled law, Notice for reopening could not have been issued. It was not the belief of the Assessing Officer that income had escaped assessment. In fact, he was compelled to go against his own legal belief and issue notice, which was wholly impermissible under law. This issue has come up before this Court on several occasions in the past, including in the case of Cadila Healthcare Ltd. v. Deputy CIT reported in 334 ITR 420 and in the case of Adani Exports v. Dy. CIT reported in 240 ITR 224. The question was also considered by the Supreme Court in the case of Indian & Eastern Newspaper Society v. CIT reported in 119 ITR 996. It is not necessary to make detailed mention of long line of judgments in this regard. In fact, the spirited defence put forward by the Assessing Officer before the Audit Party gives credence to the petitioner's contention that his entire claim was minutely examined by the Assessing Officer during the original assessment proceedings.

10. On all the grounds thus, the impugned notice must fail and the same is, therefore, quashed. The petition is allowed and disposed of.

(AKIL KURESHI, J.)

(A.J. SHASTRI, J.)

×