Court Quashes Income Tax Reassessment Notice, Citing Flawed Reasoning

Full News

Court Quashes Income Tax Reassessment Notice, Citing Flawed Reasoning

Court Quashes Income Tax Reassessment Notice, Citing Flawed Reasoning

In this case, the Gujarat High Court quashed a notice issued under Section 148 (of Income Tax Act, 1961) for reopening the assessment of Mitul Gems (the petitioner) for the Assessment Year 2007-2008. The court found that the Assessing Officer’s reasons for reopening the assessment were factually incorrect and based on a misunderstanding of the petitioner’s financial statements.

Get the full picture - access the original judgement of the court order here

Case Name:

Mitul Gems vs Assistant Commissioner of Income Tax (High Court of Gujarat)

Special Civil Application No. 17728 of 2014

Date: 28th April 2015

Key Takeaways:

- Reassessment notices must be based on accurate facts and proper reasoning.

- The Assessing Officer cannot change the grounds for reassessment after issuing the initial notice.

- Examining a new issue is not a valid reason for reopening an assessment, especially beyond the 4-year limitation period.

- The court emphasized the importance of forming a proper opinion before initiating reassessment proceedings.

Issue:

Was the Income Tax Department’s notice to reopen the assessment for A.Y. 2007-2008 valid and justified under Section 148 (of Income Tax Act, 1961)?

Facts:

- The case concerns Mitul Gems, an assessee firm, for the Assessment Year 2007-2008.

- The Income Tax Department issued a notice under Section 148 (of Income Tax Act, 1961) to reopen the assessment beyond the 4-year limitation period.

- The department claimed that the assessee had incurred labour expenses of Rs.1,38,26,488/- during the financial year 2006-2007.

- The department alleged that no TDS was deducted from a payment of Rs.22,65,048/- made to Mitul Gems/SSI unit.

- The Assessing Officer initially claimed this resulted in an under-assessment of income due to the assessee’s failure to disclose material facts.

- When the assessee objected, the Assessing Officer shifted focus to examining the assessee’s status as an SSI unit.

Arguments:

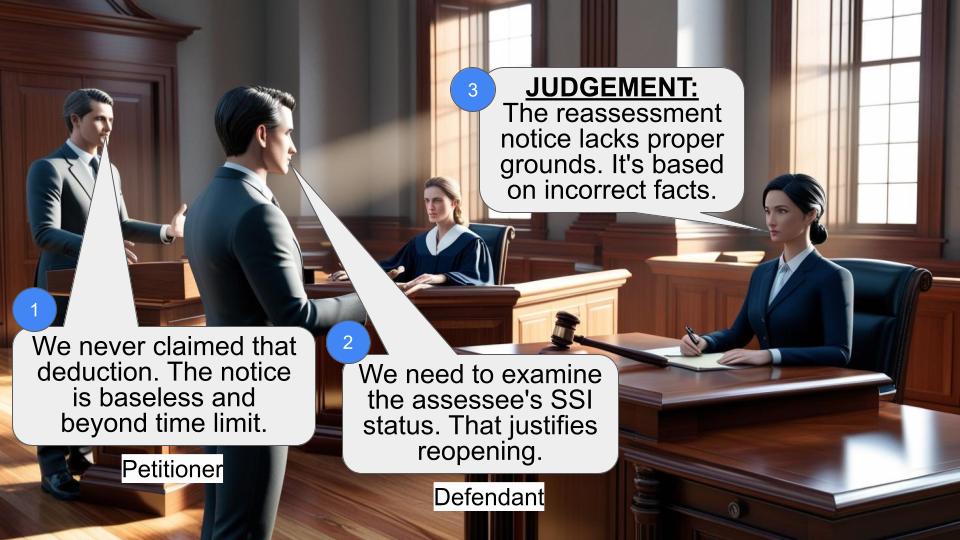

Petitioner (Mitul Gems):

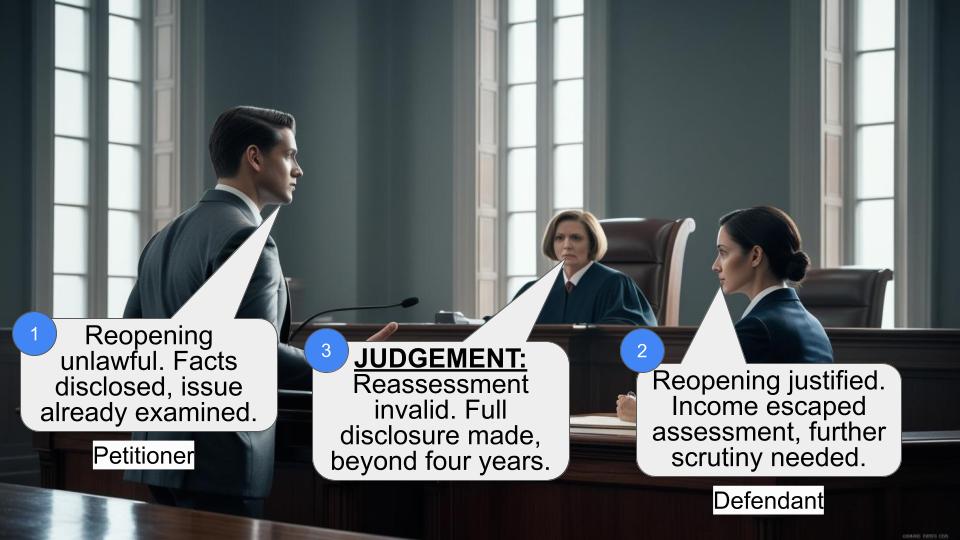

- Objected to the reopening of the assessment beyond the 4-year limitation period.

- Argued that they never claimed any deduction for the payment of Rs. 22,65,048/-.

- Contended that the Assessing Officer’s reasons for reopening were factually incorrect.

Respondent (Income Tax Department):

- Initially claimed that the assessee had not deducted TDS on certain payments, leading to under-assessment.

- Later shifted focus to examining the assessee’s status as an SSI unit.

- Argued that reopening was necessary to examine this issue.

Key Legal Precedents:

The judgment doesn’t explicitly cite any specific legal precedents. However, it refers to general principles regarding reopening of assessments under Section 147 (of Income Tax Act, 1961) and Section 148 (of Income Tax Act, 1961).

Judgement:

- The High Court quashed the notice dated 17.03.2014 issued under Section 148 (of Income Tax Act, 1961) for A.Y. 2007-2008.

- The court found that the Assessing Officer’s reasons for reopening were factually incorrect, as the assessee had never claimed the alleged deduction.

- The court criticized the Assessing Officer for changing the grounds for reassessment after issuing the initial notice.

- The judgment emphasized that an assessment cannot be reopened merely to examine a particular issue, especially beyond the 4-year limitation period.

- The court concluded that the formation of opinion by the Assessing Officer while reopening the assessment was vitiated.

FAQs:

Q: Why did the court quash the reassessment notice?

A: The court found that the Assessing Officer’s reasons for reopening were factually incorrect and the grounds were changed after issuing the initial notice.

Q: What is the significance of the 4-year limitation period mentioned in the judgment?

A: Reopening an assessment beyond 4 years requires stricter conditions, including failure by the assessee to disclose material facts fully and truly.

Q: Can the Income Tax Department reissue a notice for the same assessment year?

A: The judgment doesn’t address this directly, but generally, the department would need new and valid reasons to issue a fresh notice.

Q: What lesson can tax authorities learn from this case?

A: Tax authorities should ensure their reasons for reopening assessments are factually correct and based on proper examination of records before issuing notices.

Q: Does this judgment set a precedent for similar cases?

A: While each case is unique, this judgment emphasizes the importance of proper reasoning and adherence to procedural norms in reopening tax assessments.

1. By way of this petition under Article 226 of the Constitution of India, the petitioner – assessee has prayed for an appropriate writ, order or direction to quash and set aside the impugned notice dated 17.03.2014 issued under Section 148 (of Income Tax Act, 1961) (hereinafter referred to as the ‘Act’) for A.Y.2007-2008 by which, in exercise of powers under Section 147 (of Income Tax Act, 1961), the assessment for A.Y.2007-2008 is sought to be reopened.

2. At the outset, it is required to be noted that the assessment for A.Y.2007-2008 is sought to be reopened beyond the period of 4 years from the relevant assessment year on the following reasons recorded under Section 148(2) (of Income Tax Act, 1961):-

“As per section 40(a) (of Income Tax Act, 1961) any interest, commission or brokerage, fees or any amount payable to resident contractor or sub-contractor for carrying out any work (including labour supply) on which tax is deductible at source under chapter XVII-B and such tax has not been deducted of after deducted or after deduction has not paid into Central Government’s account during the previous year or in subsequent year before expiry of the time prescribed u/s 200(1) (of Income Tax Act, 1961), will not be allowed for computing the income chargeable under the head “profits and gains of the business or profession”.

During the financial year 2006-07 relevant to A.Y.2006-07 relevant to A.Y.2007-08, the assessee firm had incurred labour expenses (outside labour) amounting to Rs.1,38,26,488/- (Total Mfg.&Labour expenses: Rs.1,60,13,090/-). The work was done by six outside parties. However, no TDS was deducted from payment of Rs.22,65,048/- made to one party-Mitul Gems/SSI unit, 28, Saurashtra Diamond, B/H Gitanjali Cenema, Varachha road, Surat. Since, no TDS was deducted from the payment, the amount of Rs.22,65,048/- in not an allowable deduction in terms of section 40(a)(ia) (of Income Tax Act, 1961) above, however the assessee had claimed this expenditure and this resulted under assessment of income to the tune of Rs.22,65,048/- in the case of assessee due to the failure on the part of the assessee the disclose truly all material facts necessary for his assessment.”

2.1. It is required to be noted that when the petitioner raised the objections against the reopening of the assessment for A.Y.2007-2008, by communication dated 19.09.2014, the Assessing Officer has disposed of/overruled the said objections by observing in paragraph Nos.7.2 and 7.3 as under:-

“7.2.During the period under consideration, the assessee firm had incurred labour expenses (outside) amounting to Rs.1,38,26,488/- out of total manufacturing and labour expenses of Rs.1,60,13,090/-. However, no Tds was deducted from payment of Rs.22,65,048/- made to M/s.Mithul Gems(SSI Unit), 28, Saurashtra Diamond, B/h.Gitanjali cinema, Varachha road, Surat on grounds that the said unit is a division of the main firm M/s.Mithul Gems and hence, no TDS is deductible on inter divisional transfer of payments. However, this argument of the assessee is found not acceptable, since, a SSI unit is a separate entity and requires separate registration and cannot be a part of another business concern. The assessee firm has a turnover of Rs.23.64 crore and even if the assessee firm claims the SSI unit is a division of the firm, it has no legal backing. SSI benefits will be available to a SSI unit when it is a separate entity and registered as an independent unit. A SSI unit ceases to be a SSI unit when it exceeds certain prescribed limits like turnover, plant & machinery, location etc., Even if the firm controls the SSI unit, the SSI unit being a distinct entity, separate identity in regards to PAN/TAN are required to be obtained.

7.3. It would also be pertinent to mention here that it was only for examining the said issue notice u/s.148 (of Income Tax Act, 1961) has been issued and this should not cause any grievance or hardship to the assessee. In light of the above, if the assessee is confident that, his business activities have been genuine and onboard, no grounds for raising a objection against such examination should arise with the assessee.”

3. Under the circumstances, while dealing with the objections raised by the petitioner and disposing of the same, the Assessing Officer has considered altogether a different issue than the reasons for which, the reassessment proceedings are initiated. From the reasons recorded, it appears that the assessment for A.Y.2007-2008 was sought to be reopened on the ground that during the financial year 2006- 2007 relevant to A.Y.2007-2008, the assessee firm had incurred labour expenses (outside labour) amounting to Rs.1,38,26,488/- (Total Manufacturing-Labour expenses: Rs.1,60,13,090/-). The work was done by six outside parties, however, no tax was deducted from payment of Rs.22,65,048/- made to one party - Mitul Gems/SSI unit and, therefore, since, no TDS was deducted from the payment, the amount of Rs.22,65,048/- is not an allowable deduction in terms of Section 40(a)(ia) (of Income Tax Act, 1961). The assessee has claimed the said expenditure and said had resulted under assessment of income to the tune of Rs.22,65,048/- in the case of assessee due to the failure on the part of the assessee to disclose truly all material facts necessary for his assessment. However, from the communication dated 19.09.2014 disposing of the objections raised by the petitioner – assesseee, it appears that the Assessing Officer had considered altogether a different and new issue with respect to the status of the petitioner-assessee as SSI unit. It is also required to be noted at this stage and from the profit and loss accounts, it appears that as such, the petitioner–assessee never claimed any deduction with respect to the payment of Rs.22,65,048/-. Therefore, the ground on which, the Assessing Officer has tried to reopen the assessment i.e. the assessee had claimed Rs.22,65,048/- as expenditure which was not allowable and, therefore, the said has resulted under assessment, is absolutely and factually incorrect. Therefore, as such, the formation of opinion by the Assessing Officer while reopening the assessment has been vitiated.

3.1. Even otherwise, it is required to be noted that while disposing of the objections raised by the petitioner raised against the reopening of the assessment, the Assessing Officer in paragraph No.7.3 has specifically stated that it was only for examining the issue mentioned in paragraph No.7.2 with respect to the petitioner's claim/status as SSI unit, the notice under Section 148 (of Income Tax Act, 1961) has been issued. For examining the particular issue, the assessment cannot be reopened and that too beyond the period of 4 years. An assessment can be reopened on the reasons recorded and after the detailed examination, the Assessing Officer forms an opinion that there is any under assessment of the income and that too, due to failure on the part of the assessee to disclose truly and fully all the material facts necessary for the assessment, in case, the assessment proceedings are initiated beyond the period of 4 years.

4. Under the circumstances, the formation of opinion without examining the issue (as according to the Assessing Officer, the issue is yet to be examined and the notice under Section 148 (of Income Tax Act, 1961) has been issued for examining the issue mentioned in paragraph No.7.2.) has been vitiated. Under the circumstances also, the impugned notice under Section 148 (of Income Tax Act, 1961) and opening of the assessment for A.Y.2007-2008 deserve to be quashed and set aside.

5. In view of the above and for the reasons stated above, the present petition succeeds. The impugned notice dated 17.03.2014 (at Annexure-C) issued under Section 148 (of Income Tax Act, 1961) for A.Y.2007-2008 is hereby quashed and set aside. Consequently, reassessment proceedings for A.Y.2007-2008 are hereby quashed and set aside on the aforesaid ground.

6. With the above, the present petition is allowed. Rule is made absolute accordingly. However, in the facts and circumstances of the case, there shall be no order as to costs.

(M.R.SHAH, J.)

(S.H.VORA, J.)

×

Similar Ripples

Questions

Court Quashes Income Tax Reassessment Notice, Citing Flawed Reasoning

Write your CommentSimilar Posts

Generic

- Reportdata/3801.pdf