Court Quashes Reassessment Notice, Upholds 4-Year Time Limit for Tax Cases

Full News

Court Quashes Reassessment Notice, Upholds 4-Year Time Limit for Tax Cases

Court Quashes Reassessment Notice, Upholds 4-Year Time Limit for Tax Cases

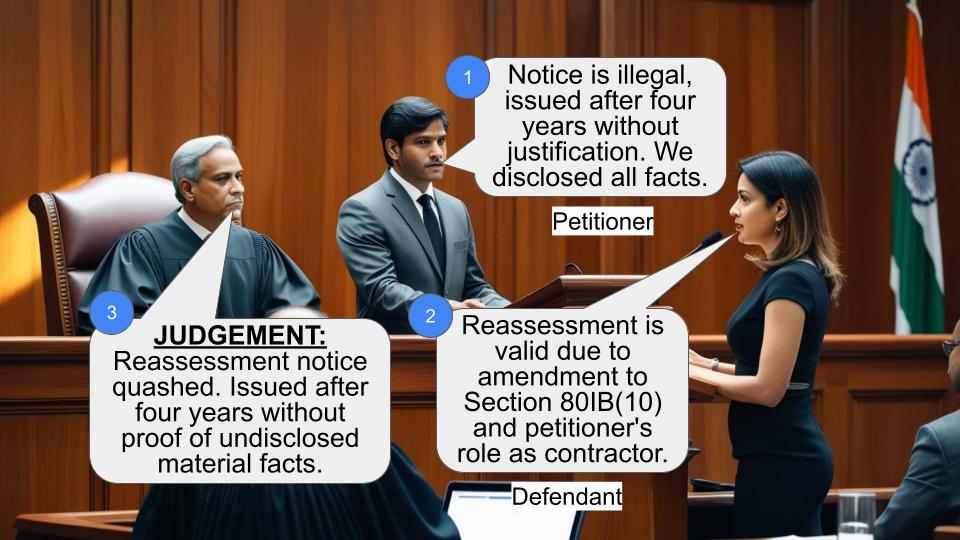

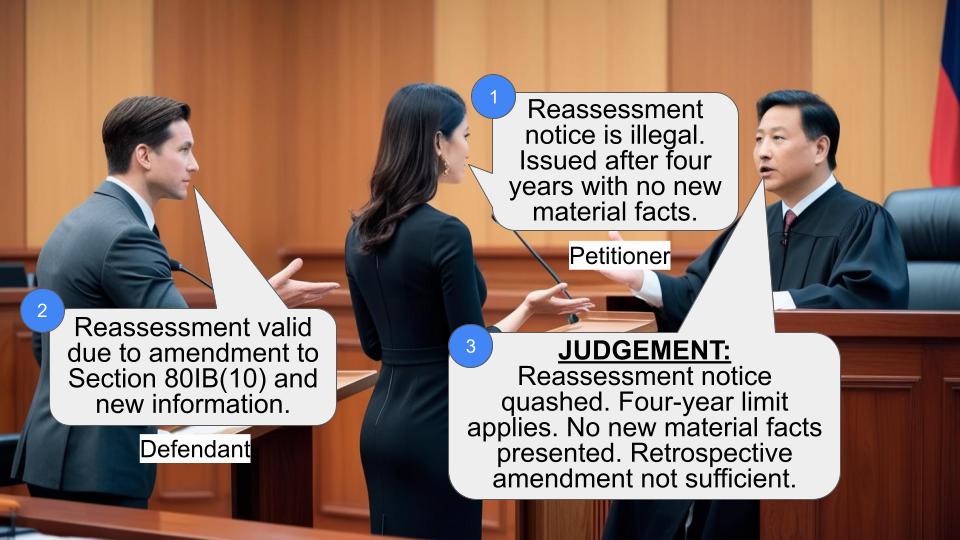

This case involves Arun Excello Foundations Private Ltd. challenging a reassessment notice issued by the Deputy Commissioner of Income Tax (DCIT) for the assessment year 2004-2005. The High Court ruled in favor of the company, quashing the reassessment notice as it was issued after the 4-year time limit without proving any failure on the part of the assessee to disclose material facts.

Get the full picture - access the original judgement of the court order here

Case Name:

Arun Excello Foundations Private Ltd. VS The Deputy Commissioner of Income Tax (High Court of Madras)

W.P.No.23899 of 2011 and M.P.No.1 of 2011

Date: 27th April 2012

Key Takeaways:

1. Reassessment notices issued after 4 years must prove failure to disclose material facts.

2. Mere change of opinion or retrospective amendments don't justify reopening assessments.

3. The court emphasized the importance of following proper procedures in tax reassessments.

Issue:

Can the Income Tax Department reopen an assessment after 4 years without proving failure on the part of the assessee to disclose material facts fully and truly?

Facts:

- Arun Excello Foundations Private Ltd. filed its income tax return for 2004-2005.

- The original assessment was completed on 27.3.2006 under Section 143(3) (of Income Tax Act, 1961).

- On 25.3.2011, the DCIT issued a notice under Section 148 (of Income Tax Act, 1961) to reopen the assessment.

- The company challenged this notice through a writ petition.

Arguments:

Petitioner (Arun Excello Foundations):

- The reassessment notice was issued after 4 years without proving any failure to disclose material facts.

- All relevant documents were provided during the original assessment.

- The reopening is based on a mere change of opinion, which is not allowed.

Respondent (DCIT):

- The reassessment was initiated based on the retrospective amendment to Section 80IB(10) (of Income Tax Act, 1961).

- The company operated as a contractor, not a developer, making it ineligible for certain deductions.

- The original assessment didn't consider the role played by the petitioner in executing the project.

Key Legal Precedents:

1. Commissioner of Income Tax, Delhi Vs. Kelvinator of India Ltd. [2010] 320 ITR 561 (SC): Change of opinion on concluded scrutiny assessment is not allowed.

2. Fenner (India) Ltd. Vs. Deputy Commissioner of Income Tax (2000) 241 ITR (Mad.) 672: Mere escapement of income is not sufficient to justify reassessment after 4 years.

3. GKN Driveshafts (India) Ltd. Vs. Income-Tax Officer (2003) 259 ITR 19: Procedures for handling reassessment notices.

Judgement:

The High Court allowed the writ petition and quashed the reassessment notice. Key points:

- The notice didn't mention any failure by the petitioner to disclose material facts fully and truly.

- All relevant records were provided during the original assessment.

- Reopening the assessment after 4 years without proving failure to disclose material facts is illegal and invalid.

FAQs:

1. Q: What is the time limit for issuing a reassessment notice?

A: Generally, it's 4 years from the end of the relevant assessment year. After 4 years, the department must prove failure to disclose material facts.

2. Q: Can a retrospective amendment justify reopening an assessment?

A: Not by itself. The court emphasized that mere retrospective amendments don't justify reopening without proving failure to disclose material facts.

3. Q: What's the significance of this judgment for taxpayers?

A: It reinforces taxpayers' rights against arbitrary reassessments and emphasizes the importance of full disclosure during original assessments.

4. Q: Does this judgment apply to all tax reassessment cases?

A: While it sets a precedent, each case is unique. However, it strengthens the position against reassessments after 4 years without proper grounds.

5. Q: What should taxpayers do if they receive a similar reassessment notice?

A: They should carefully review the notice, check if it's within the time limit, and consult a tax professional to understand their rights and options.

1. Heard the learned counsel appearing for the petitioner and the learned counsel appearing for the respondent.

2. This writ petition has been filed praying that this Court may be pleased to issue a Writ of Certiorari to call for and quash the impugned notice, dated 25.3.2011, issued under Section 148 (of Income Tax Act, 1961), (hereinafter referred to as `the Act') and the consequential proceedings, dated 28.9.2011, issued by the respondent, rejecting the objections raised by the petitioner, against the re-opening of the assessment, in respect of the assessment year 2004-2005, under Section 147 (of Income Tax Act, 1961).

3. It has been stated that the petitioner is a domestic private limited company, engaged in the business of engineering works, building and developing of residential properties. The petitioner company had filed its return of income for the assessment year 2004-2005, admitting a total income of Rs.38,16,748/-. The return of income, filed by the petitioner company, had been processed, under Section 143(1) (of Income Tax Act, 1961), on 18.5.2005. The revised return had been filed, on 29.4.2005, admitting a total income of Rs.46,13,030/-. The said return was processed, under Section 143(1) (of Income Tax Act, 1961), on 25.11.2005. The case of the petitioner company was selected for scrutiny and a notice, under Section 143(2) (of Income Tax Act, 1961) had been issued, on 7.6.2005.

4. It had been further stated that the respondent, after scrutinizing the entire records, including the agreement, had completed the assessment, by an order, dated 27.3.2006, issued under Section 143(3) (of Income Tax Act, 1961), disallowing the entire exemption relating to the deduction, under Section 80IB(10) (of Income Tax Act, 1961). Aggrieved by the said order, the petitioner company had filed a first appeal, before the Commissioner of Income Tax (Appeals), who had confirmed the order of the respondent. Thereafter, the petitioner company had filed a further appeal, before the Income Tax Appellate Tribunal. The Income Tax Appellate Tribunal had passed an order, dated 16.2.2007, in ITA No.2091/Mds/2006, partly allowing the appeal. The Commissioner of Income Tax had filed an appeal against the said order, under Section 260A (of Income Tax Act, 1961), before this Court, in T.C.No.1349 of 2007, and the said case is still pending on the file of this Court. As such, the question as to whether the petitioner company is entitled to claim deduction, under Section 80IB(10) (of Income Tax Act, 1961), is to be decided by a Division Bench of this Court. While so, the respondent had issued a notice, under Section 148 (of Income Tax Act, 1961), to the petitioner company, in respect of the assessment year 2004-2005. The said notice, dated 25.3.2011, had been received by the petitioner company, on 5.4.2011.

5. It has been further stated that, in response to the notice, dated 25.3.2011, issued by the respondent, under Section 148 (of Income Tax Act, 1961), the petitioner company had filed a letter, dated 7.4.2011, requesting the respondent to treat the revised return filed by it, on 29.4.2005, as the return filed in response to the notice, dated 25.3.2011. By the same letter, the petitioner company had requested the respondent to furnish the reasons to believe that the income of the petitioner liable to tax, had escaped assessment, within the meaning of Section 147 (of Income Tax Act, 1961).

6. It has been further stated that the respondent, by a letter, dated 21.4.2011, had furnished the reasons for the re-opening of the assessment, in respect of the assessment year 2004-2005. From the reasons given by the respondent it is clear that there is no fresh tangible material that had come into the possession of the respondent, warranting the re-opening of the concluded assessment. Thereafter, the petitioner company had submitted a detailed reply, dated 23.5.2011, requesting the respondent to drop the proceedings, as there was no reason to believe that the income liable to tax had escaped assessment.

7. The petitioner company had requested the respondent to decide the preliminary issue relating to the aspect of jurisdiction of the respondent to re-open the concluded assessment, under Section 148 (of Income Tax Act, 1961). However, the respondent, without dealing with the issue relating to the jurisdiction, had passed the impugned order, dated 28.9.2011, holding that the proceedings, under Section 147 (of Income Tax Act, 1961), had been initiated correctly and properly, and had issued a notice, under Section 143(2) (of Income Tax Act, 1961), dated 27.9.2011, fixing the date of hearing as 7.10.2011. In such circumstances, the petitioner has preferred the present writ petition, before this Court, under Article 226 of the Constitution of India.

8. The learned Senior Counsel appearing on behalf of the petitioner had submitted that the notice, dated 25.3.2011, issued by the respondent, under Section 148 (of Income Tax Act, 1961), and the consequential order, dated 28.9.2011, rejecting the objections made by the petitioner company, is arbitrary, illegal and void. He had further submitted that the assessment, for the assessment year 2004-2005, had been completed, by an order, dated 27.3.2006, under Section 143(3) (of Income Tax Act, 1961), after considering all the issues relevant to such assessment. Therefore, the re-opening of the assessment, by the respondent, under Section 147 (of Income Tax Act, 1961), is a case of `change of opinion, on a concluded scrutiny assessment, on the same set of facts, contrary to the decision of the Supreme Court, in Commissioner of Income Tax, Delhi Vs. Kelvinator of India Ltd. [2010] 320 ITR 561 (SC).

9. It had been further submitted that, for the purpose of invoking Section 147 (of Income Tax Act, 1961), after the expiry of four years, from the end of the relevant assessment year, the income chargeable to tax should have escaped assessment, by a reason of the failure on the part of the assessee to disclose, fully and truly, all the material facts necessary for the assessment, in respect of the relevant assessment year. From the reasons recorded it is apparent that the reassessment is sought to be re-opened only on the ground of the explanation to Section 80IB(10) (of Income Tax Act, 1961), which has been substituted by the Finance (No.2) Act, 2009, with retrospective effect, from 1.4.2001.

10. In the communication dated 21.4.2011, issued by the respondent it had been stated, in response to the letter submitted by the petitioner, dated 7.4.2011, that the case had been re-opened for the reason that the assessee had sold undivided share of land through a regular sale deed and the building component had been transferred by a construction agreement.

11. It had been further stated that from the contents of the agreement it was gathered that the assessee operates only as a contractor and not as a builder. Therefore, in the light of the explanation introduced to sub-Section 10 (of Income Tax Act, 1961) of Section 80IB (of Income Tax Act, 1961), by the Finance Act, 2009, with retrospective effect, from 1.4.2001, the assessee is not eligible to claim deduction under Section 80IB(10) (of Income Tax Act, 1961).

12. It had also been submitted that in the absence of any failure on the part of the petitioner to disclose, fully and truly, all material facts necessary for the assessment, the notice issued under Section 148 (of Income Tax Act, 1961), after the expiry of a period of four years from the end of the relevant assessment year, cannot be held to be valid in the eye of law.

13. The learned counsel had further submitted that the respondent would have jurisdiction to re-open the concluded assessment, only on obtaining tangible materials. If all the facts had been stated in the original assessment proceedings, a concluded assessment cannot be re-opened, without fresh facts having been brought to the knowledge of the assessing authority.

14. Further, the power to re-open an assessment is conditional on the formation of a reason to believe that income chargeable to tax had escaped assessment. In the present case, the petitioner had submitted all the relevant materials to the respondent, at the time of scrutiny of assessment, under Section 143(3) (of Income Tax Act, 1961). It had also been submitted that the respondent, without deciding the issue relating to jurisdiction, as a preliminary issue, had rejected the objections raised by the petitioner, without adducing proper reasons for such rejection.

15. The learned counsel appearing on behalf of the petitioner had relied on the decision of the High Court of Gujarat in Aayojan Developers Vs. Income Tax Officer 2011 (335) ITR 234. It has been stated that the facts and circumstances of the said case is very similar to the present case before this Court. In the said case, the High Court of Gujarat had held as follows:

"39. Examining the facts of the present case in the light of the above principles enunciated by the Supreme Court, a bare perusal of the reasons recorded indicates that there is not even a whisper as regards any failure on the part of the petitioner to disclose fully and truly all material facts, nor is it possible to infer any such failure from the reasons recorded. Merely because of the fact that the assessee had asserted that it is a developer in the returns filed by him, it cannot be said that there is any failure on the part of the petitioner to disclose fully and truly all material facts. At best, the petitioner has made a claim along with supporting documents, namely, development agreements for construction of housing projects, etc. and based upon the said documents, the Assessing Officer had formed an opinion and granted deduction under section 80-IB(10) (of Income Tax Act, 1961). As to whether in a given set of facts, the assessee is a developer or a works contractor is a matter of inference. Hence, the assertion that the petitioner is a developer, without anything more cannot be said to be an incorrect disclosure of facts, as is sought to be contended on behalf of the revenue. In the circumstances, in the absence of any failure on the part of the petitioner to disclose fully and truly all material facts necessary for its assessment for the assessment year under consideration, the assumption of jurisdiction under section 147 (of Income Tax Act, 1961) after the expiry of four years from the end of the relevant assessment year is illegal and invalid. The proceedings under section 147 (of Income Tax Act, 1961) which have been initiated by issuance of the impugned notice under section 148 (of Income Tax Act, 1961), therefore, cannot be sustained."

16. The learned counsel had also relied on the decision of this Court, in Fenner (India) Ltd. Vs. Deputy Commissioner of Income Tax (2000) 241 ITR (Mad.) 672, wherein it had been held that, in the case of a notice being issued for reassessment, after the expiry of four years, the mere escapement of income is not sufficient to justify the initiation of action. The escapement must be by reason of the failure on the part of the assessee, either to file a return, or to disclose fully and truly, the material facts necessary for the assessment.

17. He had also relied on the decision of a Division Bench of this Court, in Commissioner of Income Tax Vs. Elgi Finance Ltd. (2006) 286 ITR (Mad.) 674). The Division Bench of this Court had held that, in addition to the time limits provided for, under Section 149 (of Income Tax Act, 1961), the law has provided another limitation of four years, under the proviso to Section 147 (of Income Tax Act, 1961). As far as proviso to Section 147 (of Income Tax Act, 1961) is concerned, the law prescribes a period of four years to initiate reassessment proceedings, unless the income alleged to have escaped assessment was made out as a result of the failure on the part of the assessee to disclose, fully and truly, all material facts necessary for the assessment. Thus, the Division Bench of this Court had approved the decision of this Court, in Fenner (India) Ltd. Vs. Deputy Commissioner of Income Tax (2000) 241 ITR (Mad.) 672.

18. The learned counsel appearing on behalf of the petitioner had further submitted that there is nothing stated in the notice issued by the respondent, for the re-opening of the assessment, under Section 147 (of Income Tax Act, 1961), in respect of the assesment year 2004-2005 to show that there was a failure on the part of the petitioner to disclose all material facts, fully and truly, for the passing of an assessment order.

19. A mere change of opinion, by the assessing authority, on the finding of a new fact, by such authority, cannot be a reason for the re-opening of the concluded assessment. As such, in the present case, no such reason exists for the re-opening of the concluded assessment, in respect of the assessment year 2004-2005. Therefore, the impugned notice, dated 25.3.2011, issued under Section 148 (of Income Tax Act, 1961), and the consequential proceedings, dated 28.9.2011, issued by the respondent, are illegal and void.

20. In the counter affidavit filed on behalf of the respondent, it has been stated that the assessment, in respect of the assessment year 2004-2005, under Section 143(3) (of Income Tax Act, 1961), had been completed, vide assessment order, dated 27.3.2006. In the said assessment order the deduction was disallowed on the ground that the petitioner had violated the condition that the flats should be below 1500 square feet, and that the flats were not part of an exclusive residential project. The reason for disallowance was that the provision governing the claim of deduction, under Section 80IB (of Income Tax Act, 1961), does not permit commercial areas, especially, when such areas exceed 2000 sq.ft, in extent.

21. It had been further stated that the reassessment proceedings were initiated, vide notice, dated 25.3.2011, and the petitioner had filed a letter, dated 7.4.2011, seeking reasons for the re-opening. The reasons for the re-opening had been provided by the respondent, vide letter, dated 21.4.2011, and they are as follows

"that the assessee has sold undivided share of land through a regular sale deed, by which the building component is transferred through a construction agreement. From the contents of the agreement it is gathered that the assessee operates only as a contractor and not as a builder. In the light of the explanation to Section 80IB(10) (of Income Tax Act, 1961) introduced to sub-section 10 (of Income Tax Act, 1961) of Section 80IB (of Income Tax Act, 1961) by the Finance Act, 2009, with retrospective effect from 1.4.2001 which reads as follows:"For the removal of doubts it is hereby declared that nothing contained in this sub section shall apply to any undertaking which executes the housing project as a works contract awarded by any person (including the Central or State Government)". Therefore, it is clear that the basis for re-opening of assessment under Section 147 (of Income Tax Act, 1961) is as per the provisions of the Act."

22. As such, it is clear that the basis for the re-opening of the assessment, under Section 147 (of Income Tax Act, 1961), is as per the provisions of the said Act. The petitioner had filed its objections, on 28.9.2011. The objections filed by the petitioner had been rejected by way of a speaking order, dated 28.9.2011. The petitioner had challenged the said order. As the procedures laid down by the Supreme Court, in GKN Driveshafts (India) Ltd. Vs. Income-Tax Officer (2003) 259 ITR 19 had been meticulously followed, it would not be proper for the petitioner to state that the said decision had been violated by the respondent.

23. It has been further stated that the petitioner had not fully and truly disclosed the relevant facts, at the time of the original assessment proceedings and therefore, reassessment proceedings had been initiated, as per the proviso to Section 147 (of Income Tax Act, 1961). As such, the contention of the petitioner that the proceedings initiated by the respondent is barred by limitation is liable to be rejected.

24. In fact, the time limit prescribed for the re-opening of the assessment, which is six years from the end of the relevant assessment year, had not lapsed. The re-opening of the assessment had been done only on the basis of the fresh facts gathered after the original assessment. Therefore, the contention of the petitioner that the re-opening of the original assessment is as a result of the change of opinion, cannot be accepted for the reason that no opinion was formed on the issue of eligibility of the deduction, under Section 80IB (of Income Tax Act, 1961), in view of the retrospective effect of the amendment made in the said Section, with effect from the year, 2001. Thereafter, the deduction was not allowable in respect of an undertaking for the execution of housing projects, on works contract. The explanation to Section 80IB(10) (of Income Tax Act, 1961), introduced in sub-Section 10 (of Income Tax Act, 1961) of Section 80IB (of Income Tax Act, 1961), by the Finance Act, 2009, with retrospective effect, from 1.4.2001, reads as follows:

"For the removal of doubts it is hereby declared that nothing contained in this sub section shall apply to any undertaking which executes the housing project as a works contract awarded by any person (including the Central or State Government". Thus, it is evident from a reading of the regular assessment order, passed under Section 143(3) (of Income Tax Act, 1961), that the said issue had not been considered.

25. It had been further stated that since, the relevant records, required to establish that the petitioner is only a contractor and not a developer, had not been produced at the time of the original assessment the petitioner cannot challenge the same. It has been further stated that the original assessment had not taken into consideration the role played by the petitioner in executing the project. Based on the details submitted by the petitioner, after the completion of the assessment proceedings, it was learnt that the petitioner had undertaken and constructed the projects, as a contractor and not as a developer. The rejection of the deduction, under Section 80IB(10) (of Income Tax Act, 1961), to a contractor, is not, primarily, on account of the introduction of the explanation to Section 80IB(10) (of Income Tax Act, 1961), by the Finance Act, 2009, which came into force with retrospective effect from 1.4.2001. In fact, even before its introduction, the Mumbai Bench of the Tribunal had held, in Patel Engineering Vs. DCIT (2005) 94 ITD 411 (Mum), that incentive deduction is available only to a developer of a project, and not to the contractor. The explanation to Section 80IB(10) (of Income Tax Act, 1961) was therefore, clarificatory in nature. Therefore, the petitioner cannot be excluded from the reassessment proceedings, by stating that the reason for re-opening of the assessment is consequent to the introduction of the explanation in the statute.

26. The reliance, by the petitioner, on an order of the Tribunal, in ITA 1058 of 2009, dated 13.8.2009, to state that the reassessment proceedings is not valid, cannot be accepted. The Tribunal had no occasion to consider the issue of eligibility of the deduction, under Section 80IB (of Income Tax Act, 1961), from the point of view of the retrospective amendment made to the section, in the year, 2009, with effect from the year, 2001.

27. Further, the issue pending before a Division Bench of this Court, in a Tax Case Appeal, is different from the issue, in respect of which the assessment had been re-opened. In fact, the reason for the re-opening of the assessment is the amendment to Section 80IB(10) (of Income Tax Act, 1961), which says that the benefit of the deduction shall not be allowed, in respect of an undertaking which executes housing projects, as a works contract.

28. It had been further stated that the petitioner is wrong in stating that fresh facts had not come to light for the re-opening of the assessment. The Supreme Court, in Phool Chand Bajrang Lal vs Income-Tax Officer And Another, (1993) 203 ITR 456 SC, had held, in similar facts and circumstances, that when the assessing officer gets fresh information, which were not available at the time of the original assessment, which enables him to form a reasonable belief that certain income had escaped assessment, because of the omission or failure of the petitioner to disclose full and true facts, re-assessment proceedings could be validly initiated.

29. It had been further submitted that, as per the explanation to Section 147 (of Income Tax Act, 1961), mere submission of particulars does not amount to furnishing of full and true disclosure. In Consolidated Photo and Finvest Vs. Asst. Commissioner of Income Tax (2006) 281 ITR (Del.) 394, it had been held that a matter in issue can be validly determined only upon application of mind, by the authority determining the same. Such application of mind can be seen by the reasons given by the authority concerned. The legal position that a mere change of opinion cannot be a basis for the re-opening of a concluded assessment would be applicable only to situations where the assessing officer had applied his mind and had taken a conscious decision on a particular matter in issue. It would have no application in cases where the order of assessment does not address itself to the aspect which is the basis for the re-opening of the assessment.

30. It had also been submitted that the assessment order, passed by the assessing authority, on appreciation of the available facts, cannot be reappreciated in a writ petition, filed under Article 226 of the Constitution of India. By an order, dated 17.9.2010, this Court had held, in the writ petitions, in W.P.Nos.28457 of 2008 and 19260 of 2009, by following the decision of the Supreme Court, that the proceedings initiated for the reassessment cannot be quashed at the threshold. It would be open to the petitioner to produce the necessary records to satisfy the authority that there is no necessity for reassessment and there is no suppression or non-disclosure of full accounts by the assessee, while submitting the returns relating to the original assessment. If a final order is passed by the assessing authority based on the relevant records furnished by the assessee it would be open to such assessee to file an appeal before the appellate authority and thereafter, before the Income Tax Appellate Tribunal, before approaching this Court. When such efficacious alternative remedies are available it would not be open to the petitioner to approach this Court, by way of a Writ petition filed, under Article 226 of the Constitution of India, as held by the Supreme Court, in Raj Kumar Shivhare Vs. Directorate of Enforcement (2010) 4 SCC 772. As such, the writ petition is devoid of merits and therefore, it is liable to be dismissed.

31. The learned counsel appearing on behalf of the respondent had submitted that the question as to whether the petitioner is a developer or a contractor, undertaking works contracts, was not relevant at the time of the passing of the original assessment order. Only thereafter, after the amendment had been introduced, in Section 80IB (of Income Tax Act, 1961), in the year 2009, with effect from 1.4.2001, the respondent had proposed to reassess the income of the petitioner, by issuing a notice, under Section 147 (of Income Tax Act, 1961). Therefore, it would not be open to the petitioner to contend that the respondent had issued the notice, for the passing of a reassessment order, based on a mere change of opinion. The respondent is empowered to pass a reassessment order based on new grounds, which were not available at the time of the passing of the original assessment order.

32. In reply, the learned counsel appearing on behalf of the petitioner had submitted that the case of the respondent should stand or fall based on the reasons stated in the notice issued by the respondent for the re-opening of the assessment, under Section 147 (of Income Tax Act, 1961). When it had been stated that it had been gathered, from the contents of the construction agreement, that the assessee was operating only as a contractor and not as a builder, in the light of the explanation to Section 80IB(10) (of Income Tax Act, 1961), introduced by the Finance Act, 2009, with retrospective effect, from 1.4.2001, it would not be open to the respondent to re-open the assessment on the ground that the assessee had not disclosed the relevant facts, fully and truly, at the time of the passing of the original assessment order. No such reason has been shown in the notice issued by the respondent, for the re-opening of the assessment. As such, the decision of the High Court of Gujarat, in Aayojan Developers Vs. Income Tax Officer 2011 (335) ITR 234, is squarely applicable to the present case, in all fours.

33. In view of the contentions raised on behalf of the petitioner, as well as the respondent, and in view of the records available, and on considering the decisions cited supra, it could be seen that the respondent had issued a notice, dated 25.3.2011, for the re-opening of the assessment, under Section 147 (of Income Tax Act, 1961). However, in the said notice, issued by the respondent, it has not been stated that the petitioner had failed to fully and truly disclose the material facts, relevant for the passing of the original assessment order. As such, it would not be open to the respondent to re-open the assessment, in respect of the assessment year, 2004-2005.

34. It is not in dispute that the petitioner had placed all the relevant records, including the construction agreement, before the passing of the original assessment order. Further, it is not the case of the respondent that the petitioner had suppressed certain material facts, due to which the original assessment order, passed by the respondent, is liable to be re-assessed. In such circumstances, in the absence of the failure on the part of the petitioner to disclose fully and truly all material facts necessary for the assessment year under consideration, the assumption of jurisdiction, by the respondent, under Section 147 (of Income Tax Act, 1961), after the expiry of four years, from the end of the relevant assessment year, is illegal and invalid. Accordingly, the proceedings, under Section 147 (of Income Tax Act, 1961), which had been initiated by the issuance of the impugned notice, under Section 148 (of Income Tax Act, 1961), cannot be sustained. As such, this Court finds it appropriate to allow the writ petition. Accordingly, the writ petition stands allowed. Consequently, connected miscellaneous petition is closed.

To

The Deputy Commissioner of Income Tax, Company Circle 1(1) 121, Mahatma Gandhi Road, Nungambakkam, Chennai 600 034

×

Similar Ripples

Questions

Court Quashes Reassessment Notice, Upholds 4-Year Time Limit for Tax Cases

Write your CommentSimilar Posts

Generic

- Reportdata/5881.pdf