Court Quashes Tax Reassessment Notice, Upholds Assessee's 54EC Claim

Full News

Court Quashes Tax Reassessment Notice, Upholds Assessee's 54EC Claim

Court Quashes Tax Reassessment Notice, Upholds Assessee's 54EC Claim

This case involves a dispute between Manishkumar Tulsidas Kaneriya (the assessee) and the Deputy Commissioner of Income Tax. The tax department attempted to reopen the assessee's assessment for the year 2010-11, questioning the classification of income from land sales and the related claim for deduction under section 54EC (of Income Tax Act, 1961). The High Court ruled in favor of the assessee, setting aside the reassessment notice.

Get the full picture - access the original judgement of the court order here

Case Name:

Manish Kumar Tulsidas Kaneriya Vs Deputy Commissioner of Income Tax (High Court of Gujarat)

Special Civil Application No. 3696 of 2016

Date: 27th July 2016

Key Takeaways:

1. The Assessing Officer cannot reopen an assessment based on a mere change of opinion.

2. When a claim is scrutinized and accepted during the original assessment, it cannot be reopened without new tangible material.

3. The court emphasized the importance of the "change of opinion" concept even for reassessments within four years.

Issue:

Can the Assessing Officer reopen an assessment when the issue in question was already examined and accepted during the original scrutiny assessment?

Facts:

1. The assessee filed a return for the assessment year 2010-11, showing a total income of Rs.1.41 crores.

2. The return was scrutinized, and an assessment order was passed on 18.01.2013 under section 143(3) (of Income Tax Act, 1961).

3. The Assessing Officer issued a notice on 25.03.2015 to reopen the assessment.

4. The reopening was based on the assessee's claim of deduction under section 54EC (of Income Tax Act, 1961) for an investment of Rs.1 crore in Rural Electrification Board bonds.

5. The Assessing Officer believed that the income from land sales should be treated as business income rather than long-term capital gains.

Arguments:

Assessee's Argument:

- The issue was thoroughly examined during the original assessment.

- Reopening the assessment would be based on a mere change of opinion.

Tax Department's Argument:

- The Assessing Officer had not formed an opinion on this aspect during the original assessment.

- The assessee's income from land sales should be treated as business income, not capital gains.

Key Legal Precedents:

1. CIT v. Kelvinator of India Ltd. [2010] 320 ITR 561 : The Supreme Court held that even after 01.04.1989, the concept of "change of opinion" is relevant for reopening assessments within four years.

2. Gujarat Power Corporation Ltd. v. Assistant Commissioner of Income Tax : The High Court held that if an Assessing Officer examines a claim during scrutiny assessment and doesn't reject it, it's considered that he has formed an opinion, even if reasons aren't explicitly stated in the assessment order.

Judgement:

The High Court ruled in favor of the assessee:

1. The court found that the Assessing Officer had thoroughly examined the issue during the original assessment.

2. The Assessing Officer had accepted the assessee's classification of income and the claim under section 54EC (of Income Tax Act, 1961) after scrutiny.

3. Any attempt to reopen the assessment would be based on a mere change of opinion, which is not permissible.

4. The court set aside the reassessment notice dated 25.03.2015.

FAQs:

1. Q: What is the significance of "change of opinion" in tax reassessments?

A: A mere change of opinion by the Assessing Officer is not sufficient grounds to reopen an assessment. There must be new tangible material to justify reopening.

2. Q: Can an assessment be reopened within four years without any restrictions?

A: No, even for reassessments within four years, the concept of "change of opinion" is relevant and restricts the Assessing Officer's power to reopen assessments.

3. Q: What happens if an Assessing Officer accepts a claim without giving explicit reasons in the assessment order?

A: If a claim is scrutinized and not rejected during the assessment, it's considered that the Assessing Officer has formed an opinion in favor of the claim, even if reasons aren't explicitly stated.

4. Q: How does this judgment impact taxpayers?

A: This judgment provides protection to taxpayers against arbitrary reopening of assessments when issues have been examined and accepted during the original scrutiny.

5. Q: What should an Assessing Officer do to reopen an assessment validly?

A: The Assessing Officer must have new tangible material that suggests income has escaped assessment. A mere change of opinion on previously examined issues is not sufficient.

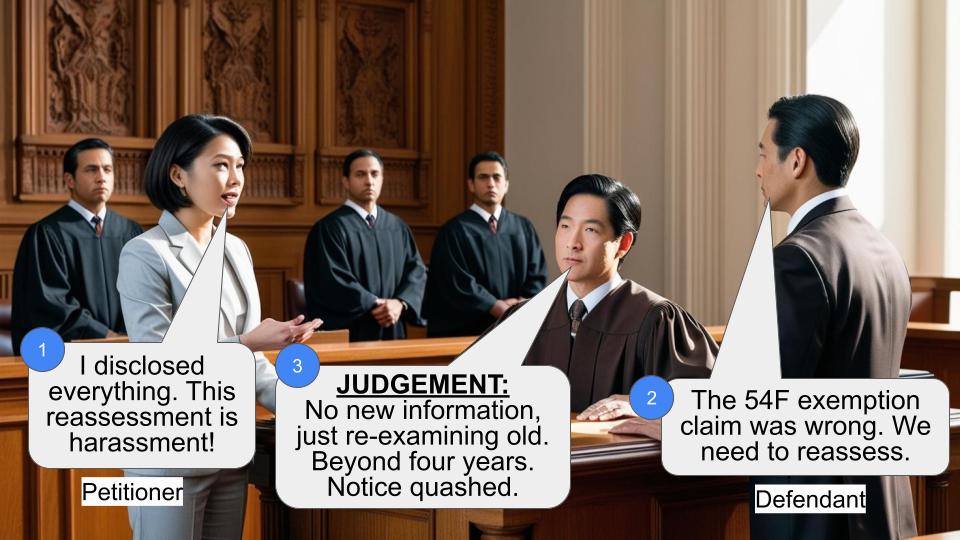

1. Petitioner has challenged a notice dated 25.03.2015 issued by the respondent Assessing Officer to reopen the petitioner's assessment for the assessment year 2010-11.

2. Brief facts are as under:

3. Petitioner is an individual and is engaged in the business of sale and purchase of land. For the assessment year 201011, the petitioner filed the return of income showing total income of Rs.1.41 crores (rounded off) on 15.10.2010. Such return was taken in scrutiny. The Assessing Officer passed order of assessment under section 143(3) (of Income Tax Act, 1961) on 18.01.2013 accepting the petitioner's declaration of total income. To reopen such scrutiny assessment, the Assessing Officer issued impugned notice. For issuing such notice, he has recorded following reasons:

“ In this case the assessee filed the return of income on 15.10.2010 showing total income at Rs.1,41,95,110/. An order u/s. 143(3) (of Income Tax Act, 1961) passed on 18.01.2013 determining total income at Rs.1,41,95,110/. Subsequently, on verification of details it is noticed that the assessee has claimed deduction u/s. 54EC (of Income Tax Act, 1961) at Rs.1,00,00,000/ for investment made in Bonds of Rural Electrification Board. The deduction was claimed against long term capital gain arising on sale of plots for Rs.1,67,48,181/. The assessee has shown the sale of various plots and worked out long term capital gain on such sale treating the plots sold as capital assets.

However, on verification of details filed during the course of assessment proceedings it is noticed that infact the assessee is engaged in the business of real estate. Further scrutiny of accounts also shows that the land sold by the assessee is part of closing stock and therefore the same has to be treated as business income. The maintenance of accounts also shows that the assessee is doing the business of purchase and sale of land. Therefore the net result of sale/purchase of land requires to be taxed as business income as against offered by the assessee, as long term capital gain. The deduction claimed by the assessee u/s. 54EC (of Income Tax Act, 1961) is also not allowable as the income is to be treated as business income. The total sale value of land sold is Rs.1,67,48,181/ and the post of acquisition of such land was Rs.7,83,848/. Therefore the net consideration of Rs.1,59,64,333/ is taxable as business income in the hands of the assessee. Since the same has been taxed as long term capital gain and the assessee has been allowed deduction u/s. 54EC (of Income Tax Act, 1961) which is not allowable on such income, there is under assessment of income to that extent. I have, therefore, reasons to believe that income chargeable to tax has escaped assessment within the meaning of sec. 147 (of Income Tax Act, 1961).”

4. Upon receipt of reasons recorded by the Assessing Officer, the petitioner raised objections under a communication dated 07.05.2015. Such objections were followed by further objections dated 30.07.2015. These objections were however rejected by the Assessing Officer by an order dated 19.02.2016. At that stage, the petitioner filed the present petition.

5. Learned counsel Shri R.K.Patel for the petitioner drawing our attention to the materials on record contended that in the reasons recorded, the sole ground pressed in service by the Assessing Officer pertains to the assessee's claim of deduction under section 54EC (of Income Tax Act, 1961) on having made investment of Rs.1 crore in the Rural Electrification Bond. According to the Assessing Officer, the proceeds of Rs.1.67 crores arising out of the sale of the plot was business income and not capital gain and therefore no deduction under section 54EC (of Income Tax Act, 1961) could have been claimed. Counsel pointed out that this issue was minutely examined by the Assessing Officer in the original assessment proceedings. Any attempt on his part to revisit the claim would be based on mere change of opinion.

6. On the other hand, learned counsel Shri Desai for the department opposed the petition contending that the Assessing Officer has not formed any opinion on this aspect during the original assessment. The assessee was engaged in the business of buying and selling land. Any receipt upon sale of plot of land would therefore form his business income, on which the Assessing Officer wrongly allowed deduction under section 54EC (of Income Tax Act, 1961). The Assessing Officer therefore had jurisdiction to reopen the assessment.

7. We have reproduced the reasons recorded by the Assessing Officer for reopening the assessment. The reasons rely on only one factor viz. assessee's claim of deduction under section 54EC (of Income Tax Act, 1961), on a sum of Rs.1 crore invested by the assessee in Rural Electrification Bond. This investment was made by the assessee from out of the sale proceeds of Rs.1.67 crores from a plots of land. The assessee thus, claimed such receipt as a long term capital gain and claimed deduction under section 54EC (of Income Tax Act, 1961) concerning the specified investment. The Assessing Officer however believed that this income was business income and no deduction under section 54EC (of Income Tax Act, 1961) was therefore allowable.

8. With this background, we may peruse the original assessment proceedings, in which, the Assessing Officer had under a letter dated 30.07.2012, raised various queries, relevant portion of which, reads as under:

“1. Brief note on the nature of activities undertaken by you, and the main source of your income during the year under consideration.”

... “12. Please furnish the details of LTCG on sale of Land alongwith documentary evidence.”

In response to such queries, the petitioner under letter dated 27.08.2012 had supplied following details.

“1. Brief note on the nature of activities: I am doing Business of purchase and sale and development of lands. He sources of my income are partnership interest, capital gains as well as interest from banks and private parties as declared in my return of income filed.”

“12. The details regarding LTCG on sale of land is given in the computation of income submitted/attached with return. The copy of the same alongwith audit report has already been filed by me on 11012012. The copies of the documents of purchase and sale are enclosed. (Please refer reply No.7 as mentioned herein above.”

9. Later on, under a letter dated 05.12.2012, the petitioner also supplied a copy of the assessee's account of Rural Electrification Corporation Limited for the year ending on 31.03.2012 and a copy of the certificate issued. It was only thereupon that the Assessing Officer passed the order of assessment making no disallowance on this ground.

10. It can thus be seen that the fact that the petitioner was engaged in the business of purchase and sale and development of lands was all too known to the Assessing Officer. In fact, the order of assessment also describes the nature of assessee's business as that of sale and purchase of land. Further the Assessing Officer was also aware about the details regarding the petitioner's claim of long term capital gain and sale of land when the petitioner supplied the computation of income alongwith audit report and documents of purchase and sale of the land in question. During the scrutiny assessment also, the Assessing Officer specifically examined the question of petitioner's claim of long term capital gain and deduction relatable to this gain under section 54EC (of Income Tax Act, 1961). It was after such scrutiny that the Assessing Officer passed the order of assessment, in which, he accepted the petitioner's claim by making following observations.

“2. During the year under consideration, the assessee has dealt in Real Estate. It is seen that the assessee has sold various plots of land on which he has either shown long term capital gain or has shown the profit earned thereon under the head “Income from Profit/Gains of Business/Profession”. Various aspects of the transactions so carried out by the assessee have been verified and it is found that the assessee has shown the profits earned thereon under the proper heads of income.

3. The assessee has claimed deduction u/s.54EC (of Income Tax Act, 1961) in respect of Long Term Capital Gain earned on the sale of land at village Vavdi, Survey No.21, Plot No.16 to 18 and 5, consisting of land admeasuring 1946.14 sq.meters. It is seen that the assessee has earned Long Term Capital Gain of Rs.4412635/ on the sale of the impugned Property which he has in turn invested in the Bond of Rural Electrification Corporation Limited. Necessary details and evidence in this regards have been furnished by the assessee. He claim of the assessee for deduction u/s. 54EC (of Income Tax Act, 1961) has been verified. Details like copy of bank account statements, confirmation of depositors etc. are filed. Personal Books of accounts were also produced by the assessee's AR and the same were test checked. He case was also discussed with the AR of the assessee.”

11. In the order of assessment also thus, the Assessing Officer referred to the fact that the assessee had sold various plots of land, receipts of which were shown either as long term capital gain or business profit. In this context, the Assessing Officer noted that he had verified various aspects of the transactions so carried out by the assessee. He concluded the assessee had shown the profit earned under proper heads of income. Thus, the Assessing Officer was fully convinced that the assessee had correctly classified certain receipts from sale of land as business income and other as long term capital gain. Having so concluded, the Assessing Officer proceeded to examine the claim of the assessee under deduction under 54EC of the Act. Having verified the claim, the Assessing Officer accepted the same.

12. It can thus be seen that during the original scrutiny assessment, the entire issue came up for discussion. The Assessing Officer raised the queries which were answered by the assessee. In the order of the assessment, the Assessing Officer passed a reasoned order why he accepted assessee's classification of the sale proceeds of the land under the separate heads of business income and long term capital gain. He also accepted the assessee's claim under section 54EC (of Income Tax Act, 1961). Any attempt on his part now to reopen the issue by doubting whether the sale proceeds would qualify as capital gain or business income would be a mere change of opinion.

The Supreme Court in case of Commissioner of Income- Tax v. Kelvinator of India Ltd. and Anr. reported in [2010] 320 ITR 561 held that even after 01.04.1989 in case of reopening of assessment within four years from the end of the relevant assessment year, the concept of change of opinion would be material. The Assessing Officer would have power to reopen the assessment provided that he has tangible material to come to the conclusion that the income chargeable to tax has escaped assessment.

13. In case of Gujarat Power Corporation Ltd. v. Assistant Commissioner of Incometax, reported in Division Bench of this Court held that once the Assessing Officer examines a particular claim under scrutiny assessment, but makes no disallowance in the final order of assessment, mere fact that he did not give reasons for doing so would be of no consequence. The Court observed as under:

“42. Bearing in mind these conflicting interests, if we revert back to central issue in debate, it can hardly be disputed that once the Assessing Officer notices a certain claim made by the assessee in the return filed, has some doubt about eligibility of such a claim and therefore, raises queries, extracts response from the assessee, thereafter in what manner such claim should be treated in the final order of assessment, is an issue on which the assessee would have no control whatsoever. Whether the Assessing Officer allows such a claim, rejects such a claim or partially allows and partially rejects the claim, are all options available with the Assessing Officer, over which the assessee beyond trying to persuade the Assessing Officer, would have no control whatsoever. Therefore, while framing the assessment, allowing the claim fully or partially, in what manner the assessment order should be framed, is totally beyond the control of the assessee. If the Assessing Officer, therefore, after scrutinizing the claim minutely during the assessment proceedings, does not reject such a claim, but chooses not to give any reasons for such a course of action that he adopts, it can hardly be stated that he did not form an opinion on such a claim. It is not unknown that assessments of larger corporations in the modern day, involve large number of complex claims, voluminous material, numerous exemptions and deductions. If the Assessing Officer is burdened with the responsibility of giving reasons for several claims so made and accepted by him, it would even otherwise cast an unreasonable expectation which within the short frame of time available under law would be too much to expect him to carry. Irrespective of this, in a given case, if the Assessing Officer on his own for reasons best known to him, chooses not to assign reasons for not rejecting the claim of an assessee after thorough scrutiny, it can hardly be stated by the revenue that the Assessing Officer can not be seen to have formed any opinion on such a claim. Such a contention, in our opinion, would be devoid of merits. If a claim made by the assessee in the return is not rejected, it stands allowed. If such a claim is scrutinized by the Assessing Officer during assessment, it means he was convinced about the validity of the claim. His formation of opinion is thus complete. Merely because he chooses not to assign his reasons in the assessment order would not alter this position. It may be a non- reasoned order but not of acceptance of a claim without formation of opinion. Any other view would give arbitrary powers to the Assessing Officer.

43. We are, therefore, of the opinion that in a situation where the Assessing Officer during scrutiny assessment, notices a claim of exemption, deduction or such like made by the assessee, having some prima facie doubt raises queries, asking the assessee to satisfy him with respect to such a claim and thereafter, does not make any addition in the final order of assessment, he can be stated to have formed an opinion whether or not in the final order he gives his reasons for not making the addition.”

14. In the present case, the Assessing Officer has gone a step beyond. He not only accepted the claim of the assessee in the order of assessment, he gave brief reasons for the same. He recorded that he was convinced about the classification adopted by the assessee and that the respective incomes were correctly classified. There is no scope for the Revenue to argue at this stage that this issue was not examined by the Assessing Officer in such assessment and that reopening within a period of four years was permissible. When we find that the Assessing Officer has no jurisdiction to reopen the assessment, question of relegating the assessee to the gamut of submitting to the reassessment proceedings simply would not arise. This suggestion of the counsel for the Revenue is therefore turned down.

15. In the result, impugned notice dated 25.03.2015 is set aside. Petition is allowed and disposed of.

(AKIL KURESHI, J.)

(A.J. SHASTRI, J.)

×