Full News

Court Rejects Revenue's Appeal on Transfer Pricing Adjustment, Upholds Assessee's Position

Court Rejects Revenue's Appeal on Transfer Pricing Adjustment, Upholds Assessee's Position

The Commissioner of Income Tax appealed against an order by the Income Tax Appellate Tribunal (ITAT) that favored Alstom Projects India Limited. The High Court dismissed the appeal, affirming that transfer pricing adjustments should only apply to transactions with Associated Enterprises, not at the entity level, even in the absence of segmental accounts.

To delve deeper, you can read the original judgement of the court order here.

Case Name:

Commissioner of Income Tax Vs Alstom Projects India Limited (High Court of Bombay)

Income Tax Appeal No.362 of 2014

Key Takeaways

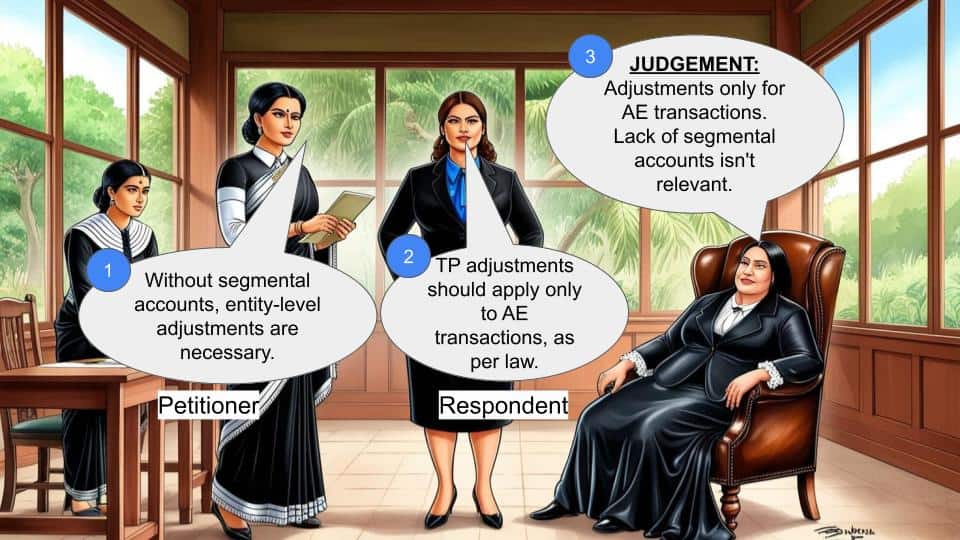

1. Transfer pricing adjustments should only be made for transactions with Associated Enterprises, not at the entity level.

2. The absence of segmental accounts does not justify entity-wide adjustments.

3. The court emphasized the need for consistent application of tax laws by the Revenue department.

4. Proportionate adjustments can be made when separate accounts are unavailable.

Issue

Whether the Tribunal was justified in holding that the Transfer Pricing Officer should apply transfer pricing adjustments only to transactions with Associated Enterprises, rather than at the entity level, in the absence of segmental accounts maintained by the assessee?

Facts

- The case relates to the Assessment Year 2006-07.

- The Income Tax Appellate Tribunal had upheld the assessee's (Alstom Projects India Limited) contention that transfer pricing adjustments should only apply to transactions with Associated Enterprises.

- The Revenue appealed this decision, arguing that in the absence of segmental accounts, adjustments should be made at the entity level.

Arguments

Revenue's Argument:

- In the absence of segmental accounts, transfer pricing adjustments should be done at the entity level.

Assessee's Argument:

- Transfer pricing adjustments should only apply to transactions with Associated Enterprises, regardless of the availability of segmental accounts.

Key Legal Precedents

1. Commissioner of Income Tax-1, Mumbai Vs. M/s Hindustran Unilever Ltd., Income Tax Appeal No.1873 of 2013

2. CIT Vs. M/s Tara Jewellers Exports Pvt. Ltd. in Income Tax Appeal No.1814 of 2013

3. CIT Vs. Pedro Araldite Pvt. Ltd. Income Tax Appeal No.1804 of 2013

4. CIT Vs. M/s Thyssen Krupp Industries Pvt. Ltd. Income Tax Appeal No.2201 of 2013

5. CIT Vs. M/s. Summit Diamond (India) Pvt. Ltd. Income Tax Appeal No.1647 of 2013

6. Commissioner of Income Tax Vs. Keihin Panalfa Ltd. (ITA No.11 of 2015) - Delhi High Court

These precedents consistently held that transfer pricing adjustments should only be made for transactions with Associated Enterprises.

Judgement

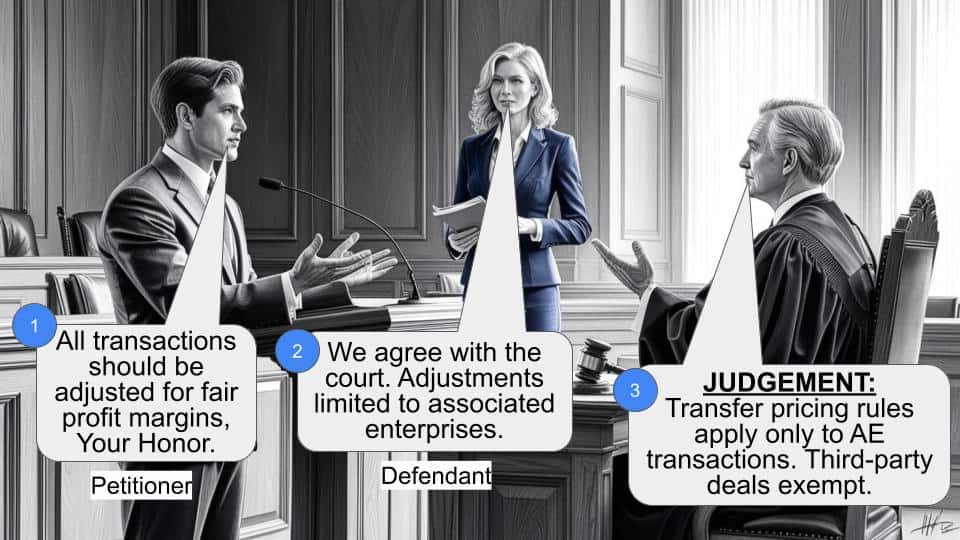

The High Court dismissed the Revenue's appeal, concluding that:

1. Transfer pricing adjustments should only be made for transactions with Associated Enterprises, not at the entity level.

2. The absence of segmental accounts does not justify entity-wide adjustments.

3. Proportionate adjustments can be made when separate accounts are unavailable.

4. The Revenue must apply tax laws consistently across all assessees

FAQs

Q1: What is transfer pricing adjustment?

A1: It's a method to ensure that transactions between related companies are priced at market value for tax purposes.

Q2: What are Associated Enterprises?

A2: These are related companies or entities that have a degree of control or influence over each other.

Q3: Why is this judgment significant?

A3: It clarifies that transfer pricing adjustments should be limited to transactions with Associated Enterprises, even when segmental accounts are not available.

Q4: What if an assessee doesn't maintain segmental accounts?

A4: The court suggests using proportionate adjustments for transactions with Associated Enterprises, rather than entity-wide adjustments.

Q5: How does this judgment affect the Income Tax Department?

A5: It emphasizes that the department must apply tax laws consistently across all assessees and avoid arbitrary application based on the assessee concerned.

1. This appeal under Section 260A (of Income Tax Act, 1961) (“the Act”) assails the order dated 23 July 2013 passed by the Income Tax Appellate Tribunal (“Tribunal”). The impugned order relates to Assessment Year 2006-07.

2. Mr. P.C. Chhotaray, learned Counsel for the Appellant urges the following question of law for our consideration :

“Whether, on the facts and in the circumstances of the case and in law, the Tribunal was justified in holding that the TPO has applied the transfer pricing adjustment to all transactions, i.e. entity level in the absence of actual segmental accounts being maintained on regular basis by the assessee ?”

3. The impugned order of the Tribunal upheld the Respondent-assessee's contention that the transfer pricing adjustment has to be made only in respect of transaction entered into by the Respondent assessee with its Associated Enterprises.

4. The grievance of the Revenue is that in the absence of segmental accounts being maintained by the Respondentassessee, transfer pricing adjustment had to be done at entity level. We specifically asked Mr. Chhotaray, learned Counsel for the appellant whether any such submission was advanced by the Revenue before the Tribunal. At this, he fairly states that no such submission was made on behalf of the Revenue. Thus we fail to understand how the present question arises from the impugned order of the Tribunal.

5. Be that as it may, Mr. Chhotaray, learned Counsel for the Revenue submits that identical question as raised herein had been admitted by this Court and in particular invited our attention to the following orders passed at the stage of admission :

(a) Commissioner of Income Tax15 Vs. M/s Super Diamonds, Income Tax Appeal No.298 of 2013; (Order dated 16 February 2015); and

(b) The Commissioner of Income Tax8 Vs. Global Jewellery Pvt. Ltd., Income Tax Appeal No.1395 of 2013. (Order dated 16 April 2015)

6. In both the above appeals we find that the question admitted was with regard to transfer pricing adjustment being done at the entity level and not restricted only to the transactions with Associated Enterprises.

However, both the appeals were admitted without the Court having had benefit of submissions on behalf of the Respondent assessee.

7. Thereafter this Court consequent to the above two orders had occasion to consider the issue of transfer pricing adjustments being done in respect of all transactions (entity level) or only in respect of transaction entered into with Associated Enterprises in the following cases :

(i) The Commissioner of Income Tax1, Mumbai Vs. M/s Hindustran Unilever Ltd., Income Tax Appeal No.1873 of 2013; (Order dated 26 July 2016)

(ii) CIT Vs. M/s Tara Jewellers Exports Pvt. Ltd. in Income Tax Appeal No.1814 of 2013 rendered on 5th October 2015;

(iii) CIT Vs. Pedro Araldite Pvt. Ltd. Income Tax Appeal No.1804 of 2013 rendered on 24th November 2015;

(iv) CIT Vs. M/s Thyssen Krupp Industries Pvt. Ltd. Income Tax Appeal No.2201 of 2013 rendered on 2nd December, 2015;

(v) CIT Vs. M/s. Summit Diamond (India) Pvt. Ltd. Income Tax Appeal No.1647 of 2013 rendered on 11th July 2016.

In all above appeals, this Court after hearing both sides upheld the view of the Tribunal that the transfer pricing adjustment has to be done only in respect of International Transactions with Associated Enterprises and not at an entity level. It may be pointed out that during the course of all the above appeals, the fact that two appeals had been admitted on the above issue were not pointed out.

8. Nevertheless, the distinction sought to be made by the Revenue is that the issue of non keeping of segmental accounts by the Assessee was not for consideration in the above cases which were dismissed, as in this case.

9. This very issue/question as raised herein was raised by the Revenue in Pedro Araldite Pvt. Ltd. (Supra). The question raised therein was as under :

“Whether on the facts and law the Tribunal was justified in directing AO/TPO to bench mark as AE transactions without appreciating (a) the Assessee itself in its transfer pricing study & report (TPSR) has chosen entity level PLI to benchmark the AE transactions; (b) the Assessee had itself failed to furnish audited segmental accounts and therefore, the TPO had rightly applied revised PLI at the entity level to determine the ALP ?”

At the above hearing, the Revenue accepted that even in the absence of segmental accounts, the adjustment has to be done only in respect of the international transactions with Associated Enterprises. This is so recorded in the order dated 24 November 2015. Therefore, on the above ground itself, the question as proposed does not give rise to any substantial question of law.

10. We may once more note that the Income Tax Department within the jurisdiction of this Court must adopt a consistent view on issues of law. In this case, we find that the Revenue urges the absence of segmental accounts would warrant entity wise adjustment, when the Revenue had itself in Pedro Araldite Pvt. Ltd. (Supra) did not canvas the point, as even according to it the issue stood covered by the earlier orders of this Court in favour of the Assessee. The Revenue must apply the law equally to all and cannot take inconsistent position in law (de hors the facts) to apply different standards to different assessee. The administration of the tax laws should not degenerate into an arbitrary and inconsistent application of law dependent upon the Assessee concerned.

11. We also note that the Delhi High Court in Commissioner of Income Tax Vs. Keihin Panalfa Ltd. (ITA No.11 of 2015) decided on 9th September, 2015 has while dealing with transfer pricing adjustment in the absence of segmental accounts held that adjustments have to be restricted only to transactions with Associated Enterprises. It further held that where separate accounts are not available, then proportionate adjustments to be made only in respect of the international transactions with Associated Enterprises.

12. We are in respectful agreement with the view of the Delhi High Court in Keihin Panalfa Ltd. (Supra). One must not loose sight of the fact that the transfer pricing adjustment is done under Chapter X of the Act. The mandate therein is only to redetermine the consideration received or given to arrive at income arising from for International Transactions with Associated Enterprises. This is particularly so as in respect of transaction with non Associated Enterprises, Chapter X of the Act is not triggered to make adjustment to considerations received or paid unless they are Specified Domestic Transactions. The transaction with nonAssociated Enterprises are presumed to be at arms length as there is no relationship which is likely to influence the price. If the contention of the Revenue is accepted, it would lead to artificial increase in the profits of transactions entered into with non Associated Enterprises by applying the margin at entity level which is not the object of Chapter X of the Act. Absence of segmental accounting is not an insurmountable issue, as proportionate basis could be adopted as done by the Delhi High Court in Keihin Panalfa Ltd. (supra).

13. In the above view, no substantial question of law arises. Therefore, we do not entertain the present appeal.

14. Accordingly, the appeal is dismissed. No order as to costs.

(S.C. GUPTE, J.) (M.S. SANKLECHA, J.)

×

Similar Ripples

Questions

Court Rejects Revenue's Appeal on Transfer Pricing Adjustment, Upholds Assessee's Position

Write your CommentSimilar Posts

Generic

- Reportdata/11486-bombay-HC.pdf