Full News

Court Rejects Tax Department's Appeal in Alleged Undervalued Property Sale Case

Court Rejects Tax Department's Appeal in Alleged Undervalued Property Sale Case

This case involves an appeal by the Revenue Department against a judgment of the Tribunal, which had upheld the order of the Commissioner Gift Tax (Appeals). The dispute centered around whether the assessee had sold properties for less than adequate consideration, potentially evading gift tax. The court dismissed the Revenue's appeal, finding insufficient evidence to prove undervaluation or tax evasion.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Gift Tax Vs H.H. Shri Gaj Singh (High Court of Rajasthan)

Income Tax Appeal No.17 of 2004

Date: 17th December 2007

Key Takeaways:

1. The burden of proof lies with the Revenue to demonstrate tax evasion through property undervaluation.

2. Mere suspicion or an Inspector's report is insufficient to invoke Section 4(1)(a) of the Gift Tax Act.

3. Positive evidence is required to show significant discrepancy between market value and sale price at the time of transaction.

Issue:

Was the Income Tax Appellate Tribunal (ITAT) correct in dismissing the department's appeal by holding that the Assessing Officer was unjustified in invoking the provisions of Section 4(1)(a) of the Gift Tax Act?

Facts:

1. The Assessing Officer initially held that the assessee had transferred properties for less than adequate consideration.

2. A taxable gift of Rs.11,38,334/- was determined, and penalty proceedings were initiated.

3. The assessee appealed to the Commissioner of Gift Tax, arguing against the invocation of Section 4(1)(a) (of Income Tax Act, 1961).

4. The Commissioner allowed the assessee's appeal, finding insufficient evidence of inadequate consideration.

5. The department then appealed to the Tribunal, which dismissed their appeal.

6. The Revenue filed this appeal in the High Court.

Arguments:

Assessee's Arguments:

1. The Assessing Officer wasn't justified in invoking Section 4(1)(a) of the Gift Tax Act.

2. The property wasn't sold for inadequate consideration.

3. Proceedings were wrongly initiated based on Section 52(2) (of Income Tax Act, 1961).

4. The department failed to prove with facts and figures that properties were sold for inadequate consideration.

Revenue's Arguments:

1. The property was undervalued to evade tax.

2. The Inspector's report indicated a higher market value than the sale price.

Key Legal Precedents:

1. The court relied on four judgments cited by the Tribunal (specific cases not mentioned in the provided text).

2. A judgment from 217 ITR 59 was referenced (details not provided in the text).

Judgement:

1. The court dismissed the Revenue's appeal.

2. It found that for Section 4(1)(a) (of Income Tax Act, 1961) to apply, there must be positive evidence showing the property was undervalued with the intention to evade tax.

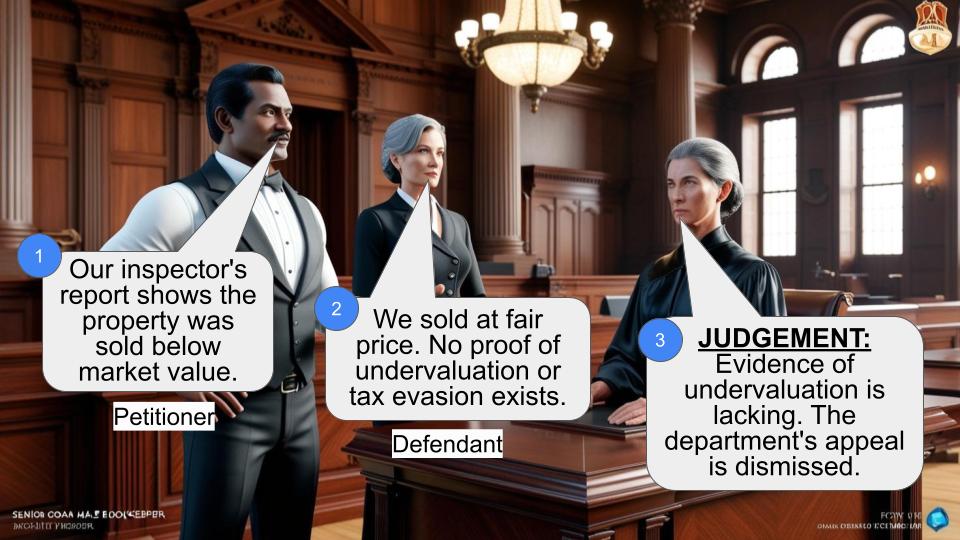

3. The Inspector's report alone was deemed insufficient evidence.

4. The Revenue failed to provide any contrary judgments or additional material about the property's valuation at the relevant time.

FAQs:

Q1: What is Section 4(1)(a) of the Gift Tax Act?

A1: While not explicitly defined in the text, it appears to be a provision dealing with deemed gifts when property is sold for less than adequate consideration.

Q2: Why was the Inspector's report considered insufficient?

A2: The report alone, without additional supporting evidence, was not considered enough to prove undervaluation or intent to evade tax.

Q3: What kind of evidence would the Revenue need to win such a case?

A3: They would need positive evidence showing the market value of the property at the time of sale and demonstrating a significant discrepancy with the actual sale price, indicating an intent to evade tax.

Q4: Does this judgment set a precedent for similar cases?

A4: While it reinforces existing principles, it emphasizes the need for substantial evidence in cases of alleged tax evasion through property undervaluation.

Q5: What's the main lesson for tax authorities from this case?

A5: Tax authorities should gather comprehensive evidence beyond just internal reports before alleging undervaluation and tax evasion in property sales.

Nobody appears for the assessee, nor any appearance has been put on behalf of the assessee, despite service.

This appeal has been filed by the Revenue, against the judgment of the learned Tribunal, upholding the order of the learned Commissioner Gift Tax (Appeals).

The brief facts are, that the Assessing Officer vide order Annex.4, dated 28.2.97, held that the assessee had transferred the properties for consideration lesser than the adequate and full consideration, and accordingly, held, that there is a taxable gift to the tune of Rs.11,38,334/-, accordingly demand notice and challan were ordered to be issued, and penalty proceedings were ordered to be separately initiated.

This order was challenged by the assessee, by filing appeal before the Commissioner of Gift Tax under Section 15(3) (of Income Tax Act, 1961)/22 of the Gift Tax Act, contending inter- alia, that the Assessing Officer was not justified in invoking the provisions of Section 4(1)(a) of the Gift Tax Act, as the assessee had not sold any property for inadequate consideration, rather the proceedings had been initiated, taking it to be a case of deemed gift, on the basis of the proceedings, concluded by him under Section 52(2) (of Income Tax Act, 1961), which he was not justified, as the provisions of Section 52(2) (of Income Tax Act, 1961) could not be invoked, merely on the basis of valuation-cell of the Income Tax Department, and that the department has not proved by facts and figure, that the appellant has sold various properties for inadequate consideration. Learned Commissioner found in para 4.2 of Annex.5, that the Assessing Officer was not justified in invoking the provisions of Section 4(1)(a) of the Gift Tax Act, because it is not established that the appellant has sold the property for inadequate consideration. It was found, that the Assessing Officer has concluded the sale to be for inadequate consideration, only on the basis of Income Tax Inspector's report, who was not technical person, for ascertaining the value. It was also found that the assessee had sold property during the accounting years relating to the assessment year 1971-72 and 1972-73, and almost on the same reasonings, the Assessing Officer also invoked the provisions of Section 4(1)(a) (of Income Tax Act, 1961), for those years, and the Tribunal, in those matters, by giving detailed reasons found, that the sale cannot be said to be deemed gifts, because the department was of the opinion, that the fair market value of the property is higher on the date of sale, than the consideration shown therein. It was found, that this clearly could not be the intention of the legislature in enacting Section 4(1)(a) (of Income Tax Act, 1961). Consequently, the appeal of the assessee was allowed.

Against that order, the department filed appeal before the learned Tribunal, and the learned Tribunal also, by relying upon four judgments in cases of different assessees, referred to in para 7, found that the burden was on the Revenue to show that the assessee had attempted to evade the tax, and had undervalued the property, and that, since there was no evidence to prove such allegation against the assessee, the computation by department at higher value, at a subsequent point of time, by itself, does not establish, that the consideration for which the transfer has been effected, was not adequate consideration, nor that the assessee had done anything with a view to evade the tax properly payable. Thus, it was also found, that in the case in hand, the Revenue has not been able to substantiate the report by any independent evidence, and then relying upon the judgment in 217 ITR 59, and some other judgments, it was held, that the department's appeal has no force, and the same was dismissed.

This appeal was admitted vide order dated 12.7.2004, by framing following substantial question of law:-

“(i) Whether on the facts and in the circumstances of the case, the learned I.T.A.T. was right in law in dismissing the appeal of the department by holding that the Assessing Officer was totally unjustified in invoking the provisions of Section 4(1)(a) (of Income Tax Act, 1961)?”

After hearing learned counsel for the appellant, and after going through the impugned judgments, we find, that for attracting the applicability of Section 4(1)(a) (of Income Tax Act, 1961), it has to be shown, that the property was undervalued, with intention to evade payment of tax, legitimately payable. Obviously, there has to be positive evidence on the side of the Revenue, to show the market value of the property at the time of sale, and to show that the market price was so high at the relevant time, that it can be concluded, that the property was sold at a deflated figure, in order to evade the tax, so as to be described as deemed gift, under Section 4(1)(a) (of Income Tax Act, 1961). In the present case, we find that apart from the Inspector's report, there is no other material, and the two learned authorities below have found, as a fact, that the Inspector's report was not sufficient, apart from the fact, that for arriving at this conclusion, the authorities below have relied upon catena of judgments, as cataloged in the order. Learned counsel for the Revenue has not been able to cite any contrary judgment, nor has he been able to bring to our notice, any material, about the valuation of the property, at the relevant time.

That being the position, obviously the question framed is required to be answered against the Revenue, and is accordingly answered.

The appeal thus, has no force and is dismissed.

( MUNISHWAR NATH BHANDARI ),J. ( N P GUPTA ),J.

×

Similar Ripples

Questions

Court Rejects Tax Department's Appeal in Alleged Undervalued Property Sale Case

Write your CommentSimilar Posts

Generic

- Reportdata/5080.pdf