Court Rules on Deductions Under Section 80HHC (of Income Tax Act, 1961): Mixed …

Full News

Court Rules on Deductions Under Section 80HHC (of Income Tax Act, 1961): Mixed Verdict for Sesa Goa Ltd.

Court Rules on Deductions Under Section 80HHC (of Income Tax Act, 1961): Mixed Verdict for Sesa Goa Ltd.

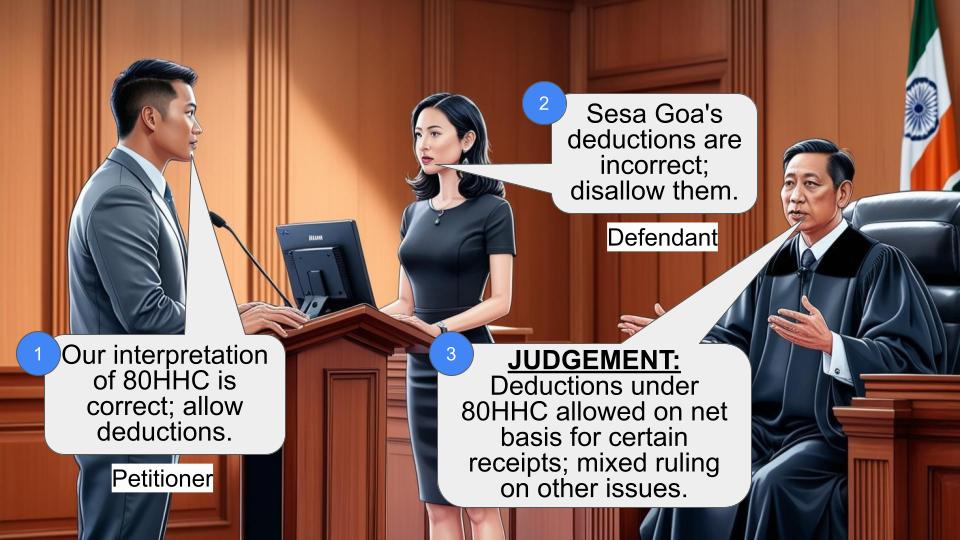

This case involves Sesa Goa Ltd. (the Appellant) and the Commissioner of Income Tax (the Respondent) regarding various issues related to income tax deductions under Section 80HHC (of Income Tax Act, 1961). The court delivered a mixed verdict, ruling in favor of both parties on different points.

Get the full picture - access the original judgement of the court order here

Case Name:

Sesa Goa Ltd. vs. Commissioner of Income Tax (High Court of Bombay)

Tax Appeal No. 30 of 2007

Date: 3rd February 2020

Key Takeaways:

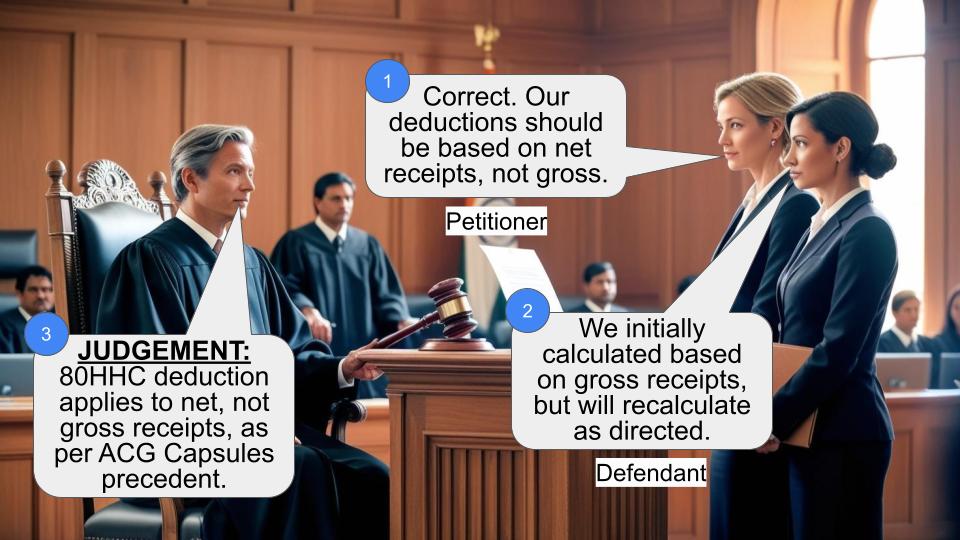

1. Certain receipts must be reduced from profits under Section 80HHC (of Income Tax Act, 1961), but on a net basis, not gross.

2. The court clarified the treatment of various types of income and expenses for tax purposes.

3. The decision impacts how businesses calculate deductions under Section 80HHC (of Income Tax Act, 1961).

Issue:

The main issue was how to interpret and apply various clauses of Section 80HHC (of Income Tax Act, 1961), particularly regarding what types of income should be reduced from profits and how these reductions should be calculated.

Facts:

- The case pertains to the Assessment Year 1997-98.

- Sesa Goa Ltd. appealed against certain tax assessments made by the Income Tax Department.

- The appeal was admitted on June 25, 2007, with several questions of law to be addressed.

- The case involved interpretation of various clauses of Section 80HHC (of Income Tax Act, 1961).

Arguments:

The arguments revolved around several points, including:

1. Whether certain types of income (like shipping agency fees and hire charges) should be reduced from profits under Section 80HHC (of Income Tax Act, 1961).

2. If reductions are to be made, should they be on a gross or net basis?

3. How to treat various types of income and expenses for tax purposes.

Key Legal Precedents:

1. ACG Associated Capsule (P) Ltd. vs. Commissioner of Income-tax (Supreme Court decision)

2. Commissioner of Income Tax vs. Sesa Goa Ltd. (Tax Appeal No. 81/2006)

3. V.M. Salgaoncar & Brother Private Limited vs. Commissioner of Income Tax (Tax Appeal No. 21 of 2011)

4. Principal Commissioner of Income Tax vs. Sesa Resources Ltd.

5. Commissioner of Income Tax vs. V.S. Dempo & Co. Pvt. Ltd. (Full Bench decision)

6. T.R.F. Limited vs. Commissioner of Income Tax, Ranchi

7. Kerala State Industrial Development Corporation Ltd. vs. CIT

8. CIT Poona vs. R.B. Rungta & Co.

Judgement:

The court delivered a mixed verdict:

1. Receipts from shipping agency fees and hire charges of machinery must be reduced under Section 80HHC (of Income Tax Act, 1961), but on a net basis, not gross.

2. Extraction charges cannot be considered part of "total turnover" for Section 80HHC (of Income Tax Act, 1961) calculations.

3. Interest received from subsidiary companies can be considered as "Profits and gains of business."

4. Hire of ships/transhippers and barges must be reduced under Section 80HHC (of Income Tax Act, 1961), but proceeds from services and repairs of vessels need not be.

5. Demurrage payable to non-resident ship owners/charterers is not disallowable under section 40(a)(i) (of Income Tax Act, 1961).

6. Bad debts written off after the close of the year, based on Board authorization, are allowable.

FAQs:

1. Q: What's the main takeaway from this judgment?

A: The court clarified how various types of income should be treated under Section 80HHC (of Income Tax Act, 1961), emphasizing that reductions should be made on a net basis, not gross.

2. Q: Does this judgment apply to all businesses?

A: While it's specific to Sesa Goa Ltd., the principles could be applied to similar cases involving Section 80HHC (of Income Tax Act, 1961) deductions.

3. Q: What's the significance of reducing on a net basis instead of gross?

A: It means businesses can deduct related expenses before calculating the reduction, potentially resulting in a lower tax liability.

4. Q: How does this judgment affect the treatment of bad debts?

A: The court ruled that bad debts can be written off even if the authorization comes after the close of the financial year, as long as it's before finalizing the accounts.

5. Q: What should businesses take away from this judgment?

A: They should carefully review their income sources and ensure they're correctly applying Section 80HHC (of Income Tax Act, 1961) deductions, particularly regarding net vs. gross calculations.

Heard Mr. R.G. Ramani for the Appellant-Assessee and Ms. S. Linhares, learned Standing Counsel for the Respondent-Revenue.

2. This appeal pertains to the Assessment Year 1997-98.

3. This appeal was admitted on 25th June, 2007, on the following substantial questions of law :

A) Whether on the facts and in the circumstances of the case, the receipts by way of "Shipping Agency fees" and "hire charges of machinery and installations" have to be reduced in terms of the said clause (baa); and if the said receipts have to be so reduced, whether it is the gross receipts that have to be reduced or it is the net receipts included in the profits, that have to be reduced ?

B) Whether on the facts and in the circumstances of the case, the receipts under the head "extraction charges" could be considered as part of the "total turnover" as defined in the said clause (ba), for the purpose of computation of the deduction under section 80 (of Income Tax Act, 1961) HHC of the Act ?

C) Whether on the facts and in the circumstances of the case, the interest received from the subsidiary companies on loans lent to them to meet their working capital requirements, and claimed by the Appellant as forming part of the income from "Profits and gains of business" could be considered as assessable as "Income from other sources"?

D) Whether on the facts and in the circumstances of the case, the receipts in the Appellant's accounts under the heads (i) proceeds of services; (ii) hire of Ship/transhippers; (iii) hire of barges; and (iv) repairs of vessels by Shipyards, which receipts have substantial costs, and arise from the main business activity of the Appellant, would have to be reduced in terms of the said clause (baa)?

E) Whether on facts and in the circumstances of the case, the demurrage payable to non-resident Ship owners/charterers of the vessels, on which tax was not deductible as found by the Tribunal,could be considered as disallowable under section 40(a)(i) (of Income Tax Act, 1961)?

F) Whether on facts and in the circumstances of the case, the bad debt actually written off as irrecoverable in the accounts of the Appellant, on the basis of an authorisation by the Board of Directors at a meeting held to approve the accounts after the close of the year, could be disallowed on the ground that the writing off of such bad debt did not take place in the relevant previous year ?

G) Whether on facts and in the circumstances of the case, in computing the deducting under section 80 (of Income Tax Act, 1961) HHC, the interest credited in the accounts, which formed part of the bad debt written off as irrecoverable, was not to be netted off from the total interest assessed as income from "Profits and gains of business" while reducing 90% of the interest receipts in accordance with the said clause (baa) in arriving at the "profits of the business"?

4. In so far as the substantial question of law (A) is concerned, we feel that the same has to be divided into two parts :-

(i) Whether, in the facts and in the circumstances of the present case, the receipts by way of "Shipping Agency fees" and "hire charges of machinery and installations" have to be reduced in terms of the clause (baa) to Section 80 (of Income Tax Act, 1961) HHC ?

(ii) If the aforesaid question of law is to be answered in favour of the Respondent-Revenue and against the Appellant-Assessee, then, whether the reduction is to be of the gross receipts or the net receipts ?

5. In so far as "hire charges of machinery and installations" are concerned, this question has been squarely answered against the Appellant-Assessee and in favour of the Respondent-Revenue in Tax Appeal No.53/2006 decided on 7th May, 2005. Incidentally, this was also an appeal instituted by this very Appellant in relation to the Assessment Year 1996-97. Applying the reasoning therein, it will, therefore, have to be held that the hire charges of machinery and installations will have to be reduced in terms of clause (baa) to Section 80 (of Income Tax Act, 1961) HHC.

6. In so far as shipping agency fees are concerned, again, we note that for the previous assessment year, as also for the assessment year with which we are concerned in the present Appeal, the fact finding authorities have held that the shipping agency fees have no nexus as such with the export and, therefore, reduction of even these receipts is warranted in terms of the explanation (baa) to Section 80 (of Income Tax Act, 1961) HHC. Since this appeal is on substantial question of law and further, since no perversity as such has been pointed out in the findings of fact recorded by the fact finding authorities, we hold that even shipping agency fees are required to be reduced from the profits in terms of clause (baa) to Section 80 (of Income Tax Act, 1961) HHC.

7. Accordingly, in so far as the first part of the substantial question of law (A) is concerned, we hold that the receipts by way of shipping agency fees and the hire charges of machinery and installations will have to be reduced from the profits in terms of the explanation clause (baa) to Section 80 (of Income Tax Act, 1961) HHC. In short, this part of the substantial question of law will have to be answered in favour of the Respondent-Revenue and against the Appellant-Assessee.

8. In so far as the second part of the substantial question of law (A) is concerned, according to us, this is covered by the decision of the Hon'ble Supreme Court in ACG Associated Capsule (P) Ltd. vs. Commissioner of Income-tax. In fact, this decision was followed by us in the Commissioner of Income Tax vs. Sesa Goa Ltd., Tax Appeal No. 81/2006 decided on 7th May, 2015 and thereafter, in V.M. Salgaoncar & Brother Private Limited vs. Commissioner of Income Tax, Tax Appeal No. 21of 2011, decided on 22nd November, 2019. In terms of these rulings, reduction has to be made not on gross basis, but on net basis only. Accordingly, we hold that though the receipts by way of shipping agency fees and higher charges for machinery and installation will have to be reduced in terms of explanation (baa) to Section 80 (of Income Tax Act, 1961) HHC, such receipts will have to be computed on net basis and not on gross basis. Accordingly, the reduction will also have to be effected only on net basis and not on gross basis. This part of the substantial question of law (A) will, therefore, have to be answered in favour of the Appellant-Assessee and against the Respondent-Revenue.

9. Accordingly, we answer the substantial question of law at (A) by holding that the receipts by way of shipping agency fees and the higher charges of machinery and installation will have to be reduced in terms of the explanation (baa) to Section 80 (of Income Tax Act, 1961) HHC of the Income Tax Act. However, such reduction will have to be on net basis and not on gross basis.

10. In so far as substantial question of law (B) is concerned, the same is directly covered against the Appellant-Assessee and in favour of the Respondent-Revenue in Sesa Goa Ltd. vs. The Commissioner of Income Tax. Accordingly, this substantial question of law is decided against the Appellant-Assessee and in favour of the Respondent-Revenue.

11. In so far as substantial question of law (C) is concerned, this issue is covered in favour of the Appellant-Assessee and against the Respondent-Revenue in Principal Commissioner of Income Tax vs. Sesa Resources Ltd.of law (C) is answered in favour of the Appellant-Assessee and against the Respondent-Revenue.

12. In so far as the substantial question of law (D) is concerned, we have to again fall back upon the decision of this Court in Sesa Goa Ltd. (supra). In the said decision, this Court has held that in so far as hire of ship/transhipper and hire of barges is concerned, receipts are covered under the explanation (baa) to Section 80 (of Income Tax Act, 1961) HHC and, therefore, such receipts will have to be reduced from out of the profits. To that extent, this substantial question of law will have to be answered against the Appellant-Assessee and in favour of the Respondent-Revenue.

13. However, when it comes to proceeds of services and repairs of vessels by shipyards, it is held in Sesa Goa Ltd. (supra) that such receipts will not be covered under the explanation (baa) to Section 80 (of Income Tax Act, 1961) HHC and, therefore, there is no question of reduction of such receipts from out of the profits. To that extent, therefore, this substantial question of law will have to be answered in favour of the Appellant-Assessee and against the Respondent-Revenue. The substantial question of law (D) is, therefore answered by holding that the receipts towards hire of ships/transhippers and hire charges of barges will have have to be reduced in terms of the explanation (baa) to Section 80 (of Income Tax Act, 1961) HHC. However, the receipts towards proceeds of services and repairs of vessels by shipyards have not been covered under the explanation (baa) to Section 80 (of Income Tax Act, 1961) HHC, will have to be reduced from out of the profits. Further, we add that in matters of such reductions, the computation will have to be on net basis and not on gross basis.

14. In so far as the substantial question of law (E) is concerned, the same is covered in favour of the Appellant-Assessee and against the Respondent-Revenue in the decision of the Full Bench of this Court in the Commissioner of Income Tax vs. V.S. Dempo & Co. Pvt. Ltd. Incidentally, three of the connected Appeals i.e. Tax Appeals No. 948/2015, 957/2015 and 978 of 2015 were the Appeals instituted by this very Appellant-Assessee. Accordingly, the substantial question of law (E) is answered in favour of the Appellant- Assessee and against the Respondent-Revenue.

15. In so far as the substantial question of law (F) is concerned, the same is again covered in favour of the Appellant-Assessee and against the Respondent-Revenue in the following decisions :

(i) T.R.F. Limited vs. Commissioner of Income Tax,Ranchi

(ii) Kerala State Industrial Development Corporation Ltd. vs. CIT

(iii) CIT Poona vs. R.B. Rungta & Co.

Accordingly, the substantial question of law (F) is answered in favour of the Appellant-Assessee and against the Respondent-Revenue.

16. Mr. Ramani, the learned Counsel for the Appellant quite correctly submits that in view of the decision on the substantial question of law (F), any decision on the substantial question of law (G) becomes redundant. Accordingly, the substantial question of law (G) is not required to be answered in the present Appeal.

17. This Appeal is, accordingly, disposed of in the aforesaid terms. There shall be no order as to costs.

Smt. M.S. Jawalkar, J. M.S. Sonak, J.

×

Similar Ripples

Questions

Court Rules on Deductions Under Section 80HHC (of Income Tax Act, 1961): Mixed Verdict for Sesa Goa Ltd.

Write your CommentSimilar Posts

Generic

- Reportdata/6299.pdf