Court Rules Rs.13.35 Lakhs as Undisclosed Income in Property Sale Dispute.

Full News

Court Rules Rs.13.35 Lakhs as Undisclosed Income in Property Sale Dispute.

Court Rules Rs.13.35 Lakhs as Undisclosed Income in Property Sale Dispute.

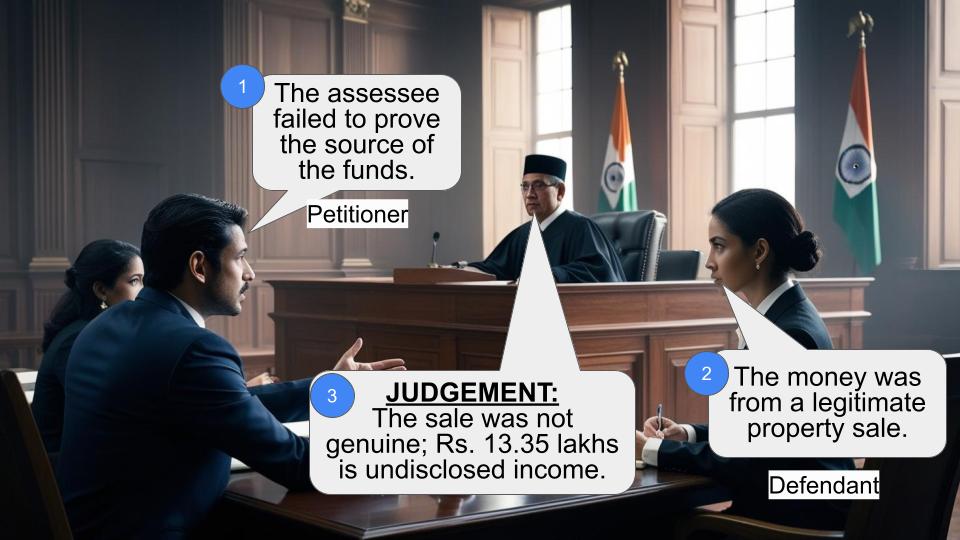

In the case of “Commissioner of Income Tax vs. K. Sundaramoorthy,” the court examined whether a property sale agreement was genuine and if the funds involved were undisclosed income. The court ultimately ruled in favor of the Revenue, determining that the transaction was not genuine and the funds were indeed undisclosed income.

Get the full picture - access the original judgement of the court order here

Case Name

Commissioner of Income Tax vs. K. Sundaramoorthy (Individual) (High Court of Madras)

Tax Case Appeal Nos. 1188 & 1199 of 2007

Date: 20th April 2016

Key Takeaways

- The court found that the alleged property sale was not genuine due to the lack of a valid agreement and the purchaser’s insufficient income.

- The decision emphasizes the importance of proving the source and nature of income in tax assessments.

- The ruling restored the Assessing Officer’s finding that Rs.13.35 lakhs was undisclosed income.

Issue

Was the property sale agreement genuine, and was the Rs.13.35 lakhs undisclosed income?

Facts

- A search at K. Sundaramoorthy’s residence revealed cash and fixed deposits totaling Rs.20.66 lakhs and Rs.13.35 lakhs, respectively.

- Sundaramoorthy claimed the funds were from a sale advance for a property, but the alleged purchaser, Mr. Kannappan, did not sign the agreement and lacked the financial means.

- The property was valued much lower than the sale price stated in the agreement.

Arguments

- Revenue’s Argument: The transaction was not genuine, and the funds were undisclosed income. The purchaser did not sign the agreement and lacked the financial capacity.

- Assessee’s Argument: The funds were from a legitimate sale advance and agricultural income, supported by necessary documentation.

Key Legal Precedents

The court did not explicitly cite other legal precedents but focused on the factual discrepancies and the lack of genuine documentation to support the assessee’s claims.

Judgement

The court ruled in favor of the Revenue, stating that the transaction was not genuine and the Rs.13.35 lakhs was undisclosed income. The court restored the Assessing Officer’s decision, emphasizing the lack of evidence to support the assessee’s claims.

FAQs

Q: Why was the property sale agreement considered not genuine?

A: The agreement was not signed by the purchaser, and the purchaser lacked the financial means to make the purchase.

Q: What was the significance of the court’s decision?

A: The decision underscores the necessity for clear documentation and proof of income sources in tax matters.

Q: What does this mean for K. Sundaramoorthy?

A: The court’s decision means that the Rs.13.35 lakhs is treated as undisclosed income, impacting his tax liabilities.

1. The above appeals have been preferred by the Revenue as against the order of the Income Tax Appellate Tribunal dated 25.08.2006 holding that the Fixed Deposit Receipts, to the tune of Rs.13.35 lakhs, in the name of the assessee and his son and cash of Rs.20.66 lakhs seized, at the time of search in his residence, did not amount to undisclosed income.

2. The respondent – assessee is a Deputy Superintending Engineer, National Highways Department, Madurai. A search was conducted under Section 132 (of Income Tax Act, 1961), in the residence of the respondent, on 24.11.1995 and cash of RS. 20,66,637/- along with Fixed Deposit Receipts of Rs.13.35 lakhs, in the name of the assessee and his son Arunkumar, were found. After repeated notices, the assessee filed a return in HUF status and did not choose to file return in his individual status. The assessment was completed under Section 158BC (of Income Tax Act, 1961) read with Section 144 (of Income Tax Act, 1961), in the hands of the assessee (individual) and a separate assessment was made regarding HUF including investment in Bank deposits and cash. The assessee had filed return of income in the status of HUF i.e, on 05.08.1996 declaring undisclosed income of Rs.1,50,764/- for the previous years 1991-1992 to 1994-1995 comprised in the block period furnishing the details of source of investment made by him in Bank Deposits and for cash found in his residence.

3. The explanation of the assessee for the source of deposits was that it was out of a sale advance of Rs.14 lakhs received from one K. Kannappan towards the sale of a shop located in Cumbum Town, jointly owned by the respondent assessee and his brother, for a total consideration of Rs.23 lakhs, as per sale agreement dated 20.11.2004. The Assessing Officer,held that the agreement seized during the search is not a genuine one and treated Rs.13.35 lakhs as unexplained investment of the assessee and treated as undisclosed income of the assessee for the block period. The Assessing Officer, further concluded that the creditors of assessee could not have advanced the amount as he has not explained the various other transactions and that the said property offered for sale may not fetch the agreed sale consideration. The Assessing Officer treated Rs.20,66,337/- seized from the assessee’s residence, at the time of raid, as unexplained and undisclosed income of the assessee as the assessee did not properly account for the said amount. The Assessing Officer determined the tax payable under Section 113 (of Income Tax Act, 1961) @ Rs. 22,45,583/-. As against the said order, two appeals, one in individual capacity and the other in the status of HUF were filed before the Income Tax Appellate Tribunal. The Tribunal held that the Fixed Deposit Receipts made in the name of the assessee and his son did not amount to undisclosed income by accepting the assessee’s explanation that the money came out of the advance given by Kannappan, with whom the assessee entered into an agreement of sale of shop in Cumbum. The Tribunal also held that Rs.12 lakhs is the accumulations of agricultural income derived from own lands and trust lands and from loan amounts received from other parties. Further, the Tribunal held that there was no corroboratory material in the possession of the Revenue to hold that the amount seized was the undisclosed income of the assessee as the assessee produced necessary materials and evidence in support of his claim and it would be sufficient for discharge of his initial burden. Against the allowing of the appeals, the present appeals have been preferred by the Revenue.

4. At the time of admission, the following two substantial questions of law were framed:

“1. Whether in the facts and circumstances of the case, the Tribunal had enough material to hold and was right in holding that the fixed deposit of Rs. 13.35 lakhs in the names of the assessee and his son is not undisclosed income?

2. Whether in the facts and circumstances of the case, the Tribunal had enough material to hold and was right in holding that the amount of cash of Rs.20.66 lakhs found at the time of search did not amount to undisclosed income?”

5. Heard Mr.M. Swaminathan, learned Standing Counsel for the appellant and Mr. R. Krishnamurthy, learned Senior Counsel for the respondent and perused the materials on record.

6. During the course of search, Money Multiplier Deposit Certificates of Central Bank of India at Ellis Nagar Branch, Madurai, to the tune of Rs. 13.35 lakhs in the name of assessee and his son Arunkumar, were found. It is the case of the assessee that the source of the said amount was the sale advance amount of Rs.14 lakhs received from one K. Kannappan of Cumbum Town towards the sale of a shop premises, jointly owned by him and his younger brother, by name, K. Chandrasekaran, for a total consideration of Rs.20 lakhs, as per the sale agreement dated 20.11.1994, which was also seized during the search. The Assessing Officer rightly suspected the genuineness of the said agreement. The signature of Kannappan found in the sale agreement and signatures found in the sworn statement filed before the authorities were different and in fact, he had admitted that he did not affix his signature in the agreement as the agreement was not presented to him for his signature.

Therefore, the Assessing Officer rightly found that the agreement was not legally valid as it was not signed by both parties. Moreover, the property,which was sought to be sold was a property measuing about 29 x 11 1⁄2 sq.ft and it was found to be in a dilapidated condition in Cumbum Town, which is a semi-urban town. On personal visit, the Assessing Officer found that the building was a very old one with brick walls plastered with mud and lime mortar, with no doors and windows available, except one folded plate shutter.

The total measurement of the property was only 333.5 sq.ft. The market value of the property, as per the recent enquiry, revealed that it would not exceed Rs.2.5 lakhs, as on date. Therefore, the Assessing Officer found that in the year 1994, when the agreement was entered into, the value of the property would have been only Rs.1.5 lakhs.

7. That apart, it was found that Mr. Kannappan was not a man of means and that he did not have sufficient income to pay Rs.14 lakhs as advance. He had got only 4 acres of cardamom estate and he could not have had any surplus money, as rightly found by the Assessing Officer. Eventhough the agreement was entered into, in the year 1993, it was neither performed nor renewed, even after the ultimate date for completing the sale. Further, the said Kannappan, did not even seek return of money. Therefore, taking into account, the above circumsances, the Assessing Officer rightly found that the sale was not a genuine one and the contention made by the assessee was only a make-believe affair. Further, the said Kannappan had no surplus money to pay an advance of Rs.14 lakhs, that too, for the purchase of the property, which was worth, only about 1.5 lakhs. Therefore, the Assessing Officer rightly treated Rs.13.35 lakhs as unexplained investment of the assessee.

8. However, the Tribunal, contrary to the material evidence available, erroneously held that the assessee, having discharged his onus, by virtue of sale agreement dated 20.11.1994, entered into between him and Kannappan, had proved the source of income ad it was open to the Department to consider the same in the assessment of Kannappan and the same cannot be added in the assessment of the assessee as undisclosed income.

9. The aforesaid findings of the Tribunal is perverse and contrary to facts. As already pointed out, the agreement was for the sale of a property,which was worth only Rs.1.5 lakhs whereas the total sale consideration was Rs.20 lakhs. Secondly, Mr. Kannappan, the alleged purchaser, did not have sufficient source of income or surplus income for purchase of the property.

Further, admittedly, the said Kannappan did not affix his signature in the agreement. Therefore, the finding of the Tirbunal that the assessee has discharged his burden of proving the source, nature and character of the credit is erroneous. The materials available would only make it very clear that the transaction in question was not genuine and the finding of the Assessing Officer that the amount of Rs.13.35 lakhs is undisclosed income is sustainable.

Therefore, the first substantial question of law is answered in favour of the revenue and against the assessee and the finding of the Assessing Officer that Rs.13.35 lakhs is undisclosed income is restored.

10. As far as the second substantial question of law is concerned, the sum of Rs.20.66 lakhs in cash, was seized during the raid on 24.11.1995 and the amount was found in different covers with certain notings on them showing contract payment, percentage of premium reduced thereon, etc. The contention of the assessee was that the said amount was out of his agricultural income and loans received from brothers and close relatives.

“10. In the statement filed along with the return, the assessee furnished the following details of sources in order to explain the cash found Rs.20,66,637.

Interest on FDRS :: 5,420 Interest on FDRS assessable in the asst. Year 96-97 :: 26,073 Sale proceeds of Jewellery :: 1,92,000 Loan from his brother Mr.Venkittu :: 4,00,000

Income from House Property :: 60,000 Agricultural Income (own lands) :: 2,00,000 Agricultural Income (Trust lands) :: 12,00,000

Total :: 20,83,493

The assessee had also contended that trust lands along with his own lands accounted for his agricultural income. With regard to the loan amount received from his brothers and close relatives, the Assessing Officer enquired the respondent's brother, who had categorically stated that he did not advance any amount to the respondent or to any other person, as per his sworn statement dated 25.11.1995. Moreover, the other relatives of the assessee were not capable of giving such a huge amount as loan. Therefore, the Assessing Officer rightly found that the creditors did not advance money nor they had the capacity to lend money. Therefore, the sum of Rs.4 lakhs,alleged to be the loan obtained by the assessee from his brother was found to be false. With regard to the agricultural income from his own lands, to the tune of of Rs.2 lakhs, though the assessee had stated that he had received 2.33 acres of agricultural lands as per the partition deed of 1984 and the sum of Rs.2 lakhs was out of the accumulations of the agricultural income derived from these lands, the Assessing Officer found that the assessee could not have earned any income from these lands as they were leased out all these years for lumpsum amounts received by the assessee as loan or lease advance. Further, the sum of Rs. 60,000/-, as income from house property, was also not accepted by the Assessing Officer. With regard to the agricultural income of Rs.12 lakhs from trust lands, the contention of the assessee was that he kept on hand Rs.12 lakhs out of the accumulations of the agricultural income derived during the past 4 years from 10.70 acres of agricultural lands owned by a private discretionary trust created by his father in the year 1942, in which the assessee is a trustee from the year 1976 onwards and as per the Village Administrative Officer's certificate, filed by the assessee, the net income from the lands was Rs.3.85 lakhs per annum. However, the Assessing Officer, taking into consideration, the fact that no books of accounts were maintained by the Trust and the trust is also not registered under Section 12A (of Income Tax Act, 1961) and non -production of any sale bills of agricultural produce and on personal visit, rightly found that the agricultural income from the Trust lands would not be more than Rs.1 lakh, after meeting the expenses of cultivation.

Therefore, the sum of Rs.12 lakhs, said to be agricultural income derived from Trust lands, amounts to undisclosed income.

11. Moreover, the sum of Rs.20,66,637/- was found kept in different covers with certain notings. Considering the status of the assessee as a Deputy Superintending Engineer in National Highways Department, Madurai, it was found that this would amount to undisclosed income as the assessee is a salaried employee of the State Government and his take home salary was Rs.8,125/- as per his own statement dated 25.11.1995. Therefore, the Assessing Officer found that no proper explanation had been given by the assessee by producing documents. Even with regard to the bank receipts for Rs.50,000/-, Rs.4000/- and Rs.20,000/- standing in the name of the assessee and his wife, the assessee did not adduce any evidence with regard to the source for the aforesaid deposit.

12. The finding reached by the Tribunal that the Revenue was not able to bring any material on record to conclude that the claim of the assessee that he kept on hand Rs.12 lakhs, out of the accumulations of the agricultural income from 10.70 acres of agricultural land owned by private discretionary trust created by the assessee's father in which the assessee is a trustee was not genuine is not sustainable as the Assessing Officer found that the lands were leased out for lumpsum amounts and they were capable of fetching income of only Rs.1 lakh per year, after meeting the cultivation expenses. Further, no books of accounts were maintained by the Trust and the Trust was also found to be an unregistered one and no sale bills were produced by the assessee to show that the agricultural income from the said lands amounted to Rs.12 lakhs. The burden was on the assessee to prove that Rs.12 lakhs got accumulated out of the agricultural income from the Trust lands, by producing supportive documents, especially, when the lands were leased out to third parties.

Therefore, the Tribunal erred in holding that the Revenue failed to produce material on record that the sum of Rs.12 lakhs was out of the accumulation of agricultural income from the Trust lands of the assessee.

13. When the brothers and relatives of the assessee have categorically stated that they have not advanced any money to the assessee nor they have the capacity to do so, the Tribunal erroneously, contrary to the facts, stated that the brothers have accepted the advance amounts paid by them and that they have also established their source. The said finding is perverse. Therefore, the conclusion of the Tribunal that the assessee did not possess any undisclosed income is liable to be set aside.

14. Further, the Tribunal was of the opinion that the assessee produced necessary materials in support of his claim and that it would be sufficient for discharge of his initial burden. But, the said finding is erroneous and contrary to law. The assessee did not produce any document and even the documents produced were not genuine, as rightly found by the Assessing Officer. No corroborative evidence was produced by the assessee to account for the income. Therefore, the second substantial question of law is also answered in favour of the department and against the assessee and the order of the Assessing Officer is restored.

15. In the result, the appeals are allowed setting aside the order of the Appellate Tribunal and restoring the order of the Assessing Officer. No costs.

(V.R.S.,J.) (N.K.K.,J.)

20 --04--2016

Index: Yes

Internet: Yes

V. RAMASUBRAMANIAN,J. AND

N. KIRUBAKARAN,J.

×

Similar Ripples

Questions

Court Rules Rs.13.35 Lakhs as Undisclosed Income in Property Sale Dispute.

Write your CommentSimilar Posts

Generic

- Reportdata/2986.pdf