Court Upholds Broad Interpretation of Profits for Tax Deduction Under Section 8…

Full News

Court Upholds Broad Interpretation of Profits for Tax Deduction Under Section 80-IA (of Income Tax Act, 1961)

Court Upholds Broad Interpretation of Profits for Tax Deduction Under Section 80-IA (of Income Tax Act, 1961)

This case involves the Commissioner of Income Tax (the Revenue) appealing against a decision by the Income Tax Appellate Tribunal. The dispute centered around whether certain types of income should be included in the calculation of profits for tax deduction purposes under Section 80-IA (of Income Tax Act, 1961). The High Court dismissed the Revenue's appeal, affirming a broader interpretation of what constitutes profits derived from an industrial undertaking.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs T.T.G. Industries Limited (High Court of Madras)

TC(A). No. 677 of 2005

Date: 25th April 2012

Key Takeaways:

1. The court affirmed a broad interpretation of "profits and gains" under Section 80-IA (of Income Tax Act, 1961).

2. Service charges, labor charges, transportation charges, and scrap sales can be included in the calculation of profits for tax deduction purposes.

3. The decision emphasizes that the only requirement for Section 80-IA (of Income Tax Act, 1961) applicability is deriving income from businesses referred to in subsection (4).

Issue:

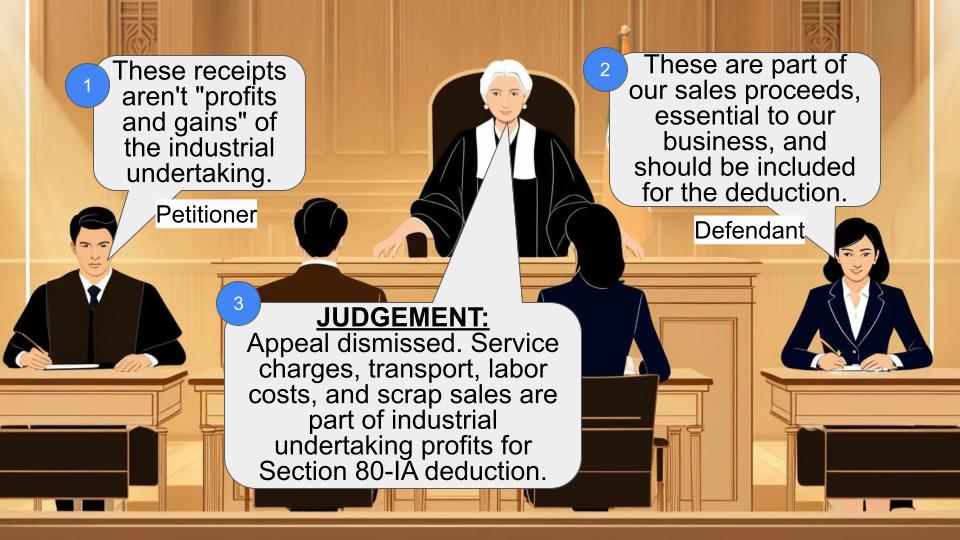

Whether service charges for maintenance, charges for transportation, erection and commission charges, labor charges, and sale of scraps during manufacturing should be included as profits and gains of the industrial undertaking for the purpose of computing deduction under Section 80-IA (of Income Tax Act, 1961)?

Facts:

- The case relates to the assessment year 1992-93.

- The assessee (T.T.G. Industries Limited) manufactures coke-oven and goose neck cleaning systems for steel and other industries.

- The Assessing Officer excluded receipts of Rs.77,27,918/- from various charges and scrap sales when computing the deduction under Section 80-IA (of Income Tax Act, 1961).

- The Commissioner of Income Tax (Appeals) agreed with the assessee that these receipts should be included.

- The Income Tax Appellate Tribunal confirmed the view of the Commissioner of Income Tax (Appeals).

- The Revenue appealed to the High Court against this decision.

Arguments:

Revenue's Argument:

- The excluded receipts (service charges, transportation charges, etc.) do not constitute profits and gains of the industrial undertaking.

Assessee's Argument:

- These charges are part of the sale proceeds, designated differently for sales tax purposes.

- The expenditures were incurred for erection, testing, and commissioning of the units sold by the assessee.

- These receipts form part of the undertaking's income and should be included in the calculation for Section 80-IA (of Income Tax Act, 1961) deduction.

Key Legal Precedents:

1. Liberty India v. CIT [2009] 317 ITR 218: The Supreme Court discussed the scope of Sections 80-IA and 80-IB, emphasizing that these sections provide profit-linked incentives.

2. CIT v. Wheels India Limited [1983] 141 ITR 745: This High Court decision held that scrap sales proceeds would fall under the profits of the undertaking.

Judgement:

The High Court dismissed the Revenue's appeal, affirming the Tribunal's decision. Key points of the judgment include:

1. The only requirement for Section 80-IA (of Income Tax Act, 1961) applicability is deriving income from businesses referred to in subsection (4).

2. Any profits and gains derived by an undertaking from any eligible business would qualify for deduction under Section 80-IA (of Income Tax Act, 1961).

3. Service charges, labor charges, and transportation charges incurred for erection, testing, and commissioning of sold units are part of the industrial undertaking's receipts.

4. Scrap sales also qualify for consideration under Section 80-IA (of Income Tax Act, 1961).

FAQs:

1. Q: What types of income can be included in the calculation of profits under Section 80-IA (of Income Tax Act, 1961)?

A: According to this judgment, a wide range of income including service charges, labor charges, transportation charges, and even scrap sales can be included.

2. Q: Does this decision apply to all industries?

A: While the case specifically dealt with a manufacturer of coke-oven and goose neck cleaning systems, the principle could potentially apply to other industries eligible for Section 80-IA (of Income Tax Act, 1961) deductions.

3. Q: How does this judgment differ from the treatment of duty drawbacks and similar incentives?

A: Unlike duty drawbacks, which the Supreme Court in Liberty India v. CIT ruled as separate from profits derived from the industrial undertaking, this judgment considers the disputed charges as integral to the business operations.

4. Q: What is the significance of the phrase "derived from" in Section 80-IA (of Income Tax Act, 1961)?

A: The court interprets this phrase broadly, including various types of income that are directly related to the business operations of the industrial undertaking.

5. Q: Does this judgment change the fundamental nature of Section 80-IA (of Income Tax Act, 1961) deductions?

A: No, it reinforces that Section 80-IA (of Income Tax Act, 1961) provides a "profit-linked incentive," but broadens the interpretation of what constitutes profits derived from the eligible business.

1. The Revenue is on appeal as against the order of the Income Tax Appellate Tribunal relating to assessment year 1992-93. The above Tax Case (Appeal) was admitted on the following substantial question of law :-

"Whether on the facts and in the circumstances of the case, the Income Tax Appellate Tribunal was right in holding that, service charges for maintenance, charges for transportation, erection and commission charges, labour charges, sale of scraps during manufacturing to be included as profits and gains of the industrial undertaking for the purpose of computation of deduction under Section 80IA (of Income Tax Act, 1961)?

2. The assessee herein is engaged in the manufacture of coke-oven and goose neck cleaning system for steel and other industries. The Assessing Officer while computing the deduction under Section 80IA (of Income Tax Act, 1961), excluded the receipts of service charges, charges for transportation, erection and commission charges, labour charges and sale scrap to the tune of Rs.77,27,918/- as not constituting the profits and gains of the Industrial undertaking. The assessee preferred an appeal before the Commissioner of Income Tax (Appeals), who agreed with the assessee. The Appellate authority pointed out that the amount represented part of the sale proceeds designated differently in order to get reduction in sales tax. The expenditure were incurred for erection, testing and commissioning of the units sold by the assessee. Such receipts formed part of the receipts of the undertaking. He further pointed out that Section 80IA (of Income Tax Act, 1961) is concerned about deduction of profits and gains derived from the business of industrial undertaking or enterprise which could not be construed as profits and gains arising from manufacture. The first Appellate Authority held that the sum of Rs.57,28,091/- representing erection charges formed part of the profits. As regards other receipts, the first Appellate Authority held the same view. As to the sale of scrap, the first Appellate Authority pointed out that even by the Assessing Officer's restrictive standards the scrap sales proceeds would fall to be called the profits of the undertaking as held in the decision of this Court reported in [1983] 141 ITR 745 CIT v. WHEELS INDIA LIMITED. Aggrieved by the same, the Revenue went on appeal before the Tribunal, which confirmed the view of the Commissioner of Income Tax (Appeals). Aggrieved by this, the Revenue is on appeal before this Court.

3. In the decision reported in [2009] 317 ITR 218 LIBERTY INDIA v. CIT, the Apex Court considered the scope of Section 80IA (of Income Tax Act, 1961) and 80IB (of Income Tax Act, 1961). The Apex Court pointed out that,

". It is evident that section 80-IB (of Income Tax Act, 1961) provides for allowing of deduction in respect of profits and gains derived from the eligible business. The words "derived from" are narrower in connotation as compared to the words "attributable to". In other words, by using the expressing "derived from", Parliament intended to cover sources not beyond the first degree. "

4. Pointing out that Sections 80-IA/80-IB have a common scheme, it held that, ".We may reiterate that sections 80-I, 80-IA and 80-IB have a common scheme and if so read it is clear that the said sections provide for incentives in the form of deduction(s) which are linked to profits and not to investment. On an analysis of sections 80-IA and 80-IB it becomes clear that any industrial undertaking, which becomes eligible on satisfying sub-section (2), would be entitled to deduction under sub-section (1) only to the extent of profits derived from such industrial undertaking after specified date(s). Hence, apart from eligibility, sub-section (1) purports to restrict the quantum of deduction to a specified percentage of profits. This is the importance of the words "derived from industrial undertaking" as against "profits attributable to industrial undertaking .. "

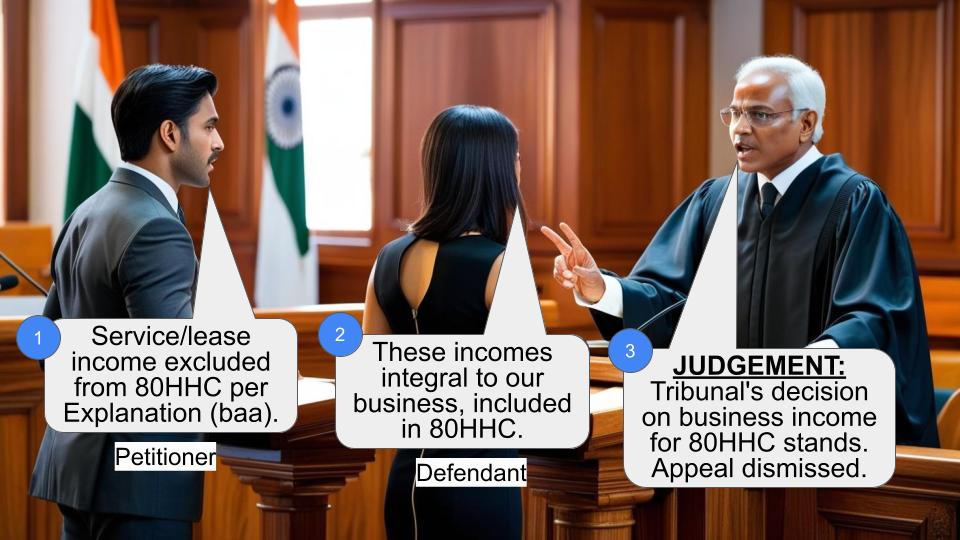

5. Dealing with the question as to whether duty draw back, DEPB benefits, rebate etc., could be credited against the cost of manufacture of goods debited in the profits and loss account for the purpose of Section 80IA (of Income Tax Act, 1961)/ 80IB, the Apex Court held that such benefits/ rebates would constitute independent source of income beyond the first degree nexus between profits and the industrial undertaking. It pointed out that the cost of purchase includes duties and taxes (other than those subsequently recoverable by the enterprise from the taxing authorities), freight inwards and other expenditure directly attributable to the acquisition. Hence, trade discounts, rebate, duty drawback and such similar items are deducted in determining the costs of purchase. Therefore, duty drawback, rebate etc., should not be treated as adjustment (credited) to the cost of purchase or manufacture of goods. They should be treated as separate items of Revenue or income and accounted for accordingly. Thus the profits derived from such incentive scheme do not fall within the expression of profits derived from industrial undertaking under Section 80IB (of Income Tax Act, 1961).

6. Guided by the above decision, when we look at Section 80IA (of Income Tax Act, 1961), it is clear that the only requirement for the applicability is deriving of income by an undertaking or an enterprise from any business referred to in sub section (4). Thus, any profits and gains derived by an undertaking from any business would qualify for deduction under Section 80IA (of Income Tax Act, 1961).

7. As the Apex Court pointed out in [2009] 317 ITR 218 LIBERTY INDIA v. CIT, the deduction provided under Section 80IA (of Income Tax Act, 1961) being "profit linked incentive", we have no hesitation in confirming the order of the Tribunal. Thus on the facts found that the service charges, labour charges and transportation charges incurred were for erection testing and commissioning of the units sold and were part of the receipts of the industrial undertaking, they come within the meaning of the profits and gains derived by the undertaking or an enterprise from any business referred to in sub Section (4). Extending the same, scrap sales also qualify for consideration under Section 80IA (of Income Tax Act, 1961).

8. In the result, the Tax Case Appeal is dismissed. No costs.

(C.V.,J) (K.R.C.B.,J)

25.04.2012

Index : Yes/No

Internet : Yes/No

To

1. The Commissioner of Income Tax Tamil Nadu I, Madras

2. The Income Tax Appellate Tribunal, Chennai B Bench

CHITRA VENKATARAMAN,J and K.RAVICHANDRA BAABU,J

25.04.2011

×

Questions

Court Upholds Broad Interpretation of Profits for Tax Deduction Under Section 80-IA (of Income Tax Act, 1961)

Write your CommentSimilar Posts

Generic

- Reportdata/5892.pdf