Court Upholds Deletion of Tax Additions, Emphasizes Importance of Satisfactory …

Full News

Court Upholds Deletion of Tax Additions, Emphasizes Importance of Satisfactory Explanations

Court Upholds Deletion of Tax Additions, Emphasizes Importance of Satisfactory Explanations

This case involves an income tax appeal filed by the Income Tax Department against a decision made by the Income Tax Appellate Tribunal (ITAT). The ITAT had upheld the deletion of certain additions made by the Assessing Officer to the assessee's income. The High Court dismissed the appeal, agreeing with the ITAT's decision that the assessee's explanations regarding the nature and source of credits in their books were satisfactory.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax & Another Vs Kanhaiya Lal Jaiswal (High Court of Allahabad)

Income Tax Appeal No. 66 of 2011

Date: 13th July 2012

Key Takeaways:

1. The importance of providing satisfactory explanations for credits in books of accounts under Section 68 (of Income Tax Act, 1961).

2. Assessing Officers must record their findings regarding the explanations offered by assessees.

3. Additions cannot be made arbitrarily without considering the assessee's explanations.

4. The High Court's reluctance to interfere with factual findings of lower authorities unless there's a question of law.

Issue

Was the Income Tax Appellate Tribunal justified in deleting the additions made by the Assessing Officer to the assessee's income when the assessee provided satisfactory explanations for the credits in their books?

Facts

1. The case pertains to the assessment year 2005-06.

2. The Income Tax Officer made two additions to the assessee's income:

a) Rs. 11,39,000/- as unexplained increase of cash credit in the balance sheet

b) Rs. 68,484/- as extra profit

3. The assessee challenged these additions, arguing that the Assessing Officer didn't consider their explanations.

4. The appellate authority found the assessee's explanations satisfactory and deleted the additions.

5. The Income Tax Department appealed against this decision to the ITAT and then to the High Court.

Arguments

Assessee's Arguments:

1. The creditworthiness of the creditors was adequately explained.

2. The genuineness of transactions was established during the assessment proceedings.

3. Proper documentation was provided to prove the transfers and credits.

Income Tax Department's Arguments:

1. The additions were justified as the audit report filed with the return didn't show these creditors.

2. The Tribunal wasn't justified in deleting the additions made by the Assessing Officer.

Key Legal Precedents

The judgment doesn't mention specific case laws, but it heavily relies on Section 68 (of Income Tax Act, 1961). This section deals with unexplained cash credits and the burden of proof on the assessee to explain the nature and source of such credits.

Judgement

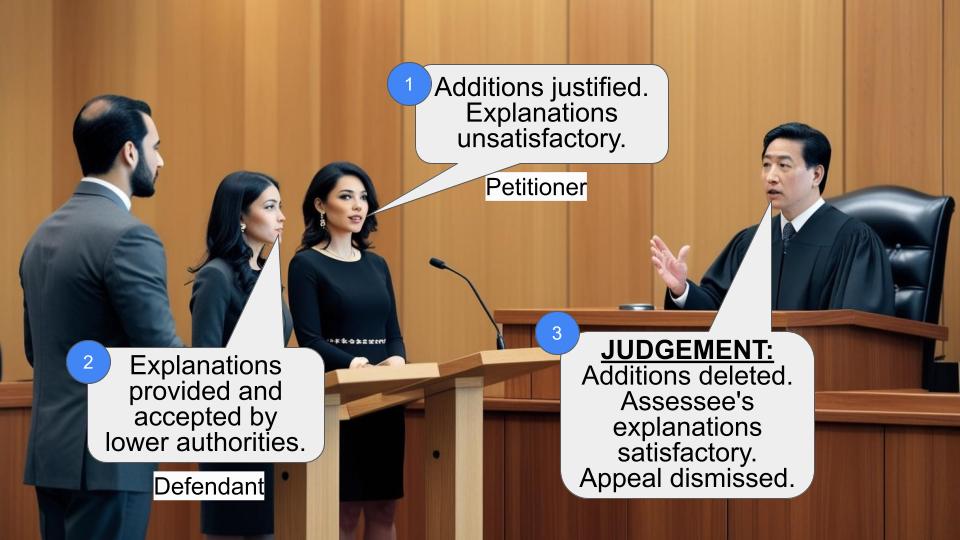

1. The High Court dismissed the appeal filed by the Income Tax Department.

2. It agreed with the ITAT's findings that the Assessing Officer didn't record any finding regarding the explanation offered by the assessee.

3. The court emphasized that the Assessing Officer didn't state that the explanation was unsatisfactory.

4. The High Court found no error in the factual findings of the appellate authority and the ITAT.

5. The court concluded that the questions raised didn't constitute questions of law for consideration by the High Court.

FAQs

1. Q: What is Section 68 (of Income Tax Act, 1961)?

A: Section 68 (of Income Tax Act, 1961) deals with unexplained cash credits. It allows the Assessing Officer to tax unexplained sums found credited in the books of an assessee if the assessee fails to offer a satisfactory explanation about their nature and source.

2. Q: Why did the High Court dismiss the appeal?

A: The High Court found no error in the factual findings of the lower authorities and determined that no question of law arose for consideration.

3. Q: What was the main issue with the Assessing Officer's actions?

A: The Assessing Officer made additions without considering the assessee's explanations or recording that these explanations were unsatisfactory.

4. Q: What lesson can taxpayers learn from this case?

A: It's crucial to maintain proper documentation and be prepared to offer satisfactory explanations for all credits in your books of accounts.

5. Q: Can the Income Tax Department appeal this decision further?

A: While the judgment doesn't mention it explicitly, typically, the department could appeal to the Supreme Court if they believe there's a substantial question of law involved.

We have heard Shri Dhananjay Awasthi, learned counsel for the income tax department. Shri Krishna Ji Agrawal appears for the respondent.

This income tax appeal under Section 260-A (of Income Tax Act, 1961), 1961 has been filed on the following questions of law:-

"(1) Whether on the facts and in the circumstances of the case, the Tribunal is justified in law in deleting the addition of Rs.11,39,000/- made by the A.O. on account of loan creditors despite the fact that in the audit report filed along with the returned no such creditors were shown?

(2) Whether on the facts and in the circumstances of the case, the Tribunal is justified in law in confirming the order of the CIT (A) deleting the addition of Rs.68,484/- made by the A.O. by applying a higher rate of gross profit on estimated sale of Rs.20,00, 000/-?"

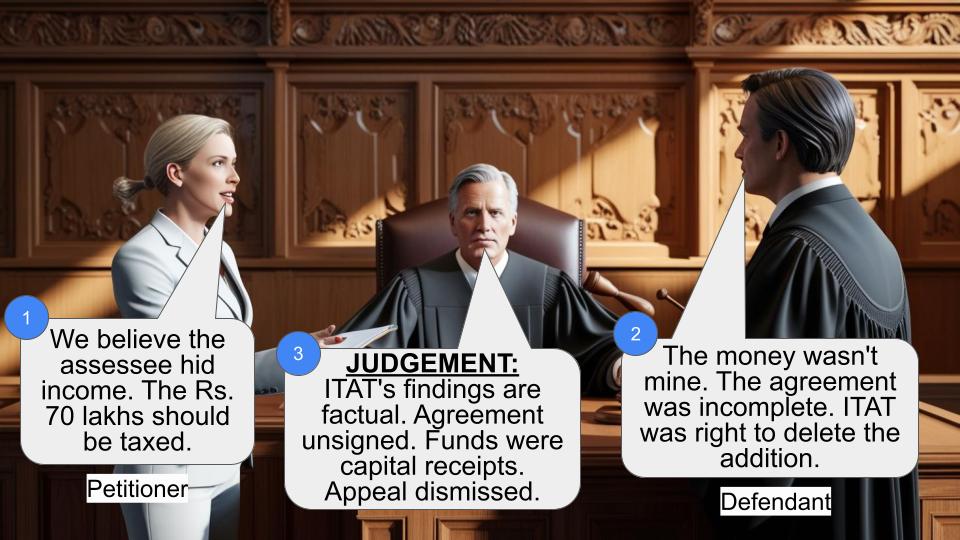

The Income Tax Officer, in respect of the assessment year 2005-06 did not accept the books of account. He added Rs.11,39,000/- as unexplained increase of cash credit in the balance sheet, and also added the extra profit of Rs.68,484/-.

The assessee challenged the order of the Income Tax Officer dated 10.12.2007 making additions on the returned income. He objected that the Assessing Officer has not considered the explanation of the assessee while adding the cash credits, under Section 68 (of Income Tax Act, 1961) (the Act) and the excess profit. The appellate authority found that the explanation submitted by the assessee was satisfactory. The creditworthiness of the creditors was explained, in as much as the credit entry in respect of Ram Kali Devi, the wife of the petitioner of Rs.6,10,000/- and Rs.5 lacs of Mohit Agencies as well as Rs.29,300/- on the liability side of the balance sheet was sufficiently explained.

The appellate authority found that the genuineness of the transactions and identity and creditworthiness of Smt. Ram Kali Devi was well established during selections of assessment proceeding, which is quite evident from the final query letter dated 29.11.2007. So far as entry of Rs.5 lacs relating to M/s Mohit Agency is concerned, the appellate authority found that the appellant had appointed M/s Mohit Agency for its stocking business on receipt of draft of Rs.5 lacs in favour of M/s Mohan Bakers Pvt. Ltd., Calcutta (the consigner). A copy of the account of M/s Mohit Agency along with account of M/s Mohan Bakers was submitted before the Assessing Officer during the course of assessment proceedings to prove the transfer. No cash credit was credited in the books of the assessee. The copies of the certificate issued by the Bank of Baroda, Bans Mandi Branch, Allahabad verifying the draft was also enclosed with the written submissions. With regard to addition of Rs.24,000/- the appellate authority found that the assessee was carrying on consigning business on large scale and shown sale and purchase of more than Rs.2 crores under the head C and F. For the purposes of stocking the goods expenditure incurred for hiring of godowns was genuine business expenditure for which the assessee had made in his books of accounts.

The ITO filed appeal against the appellate order dated 3.2.2010. The Tribunal did not find any error of law in the findings recorded by the appellate authority and reiterated the findings that the ingredients of Section 68 (of Income Tax Act, 1961), were not satisfied. The additions were made only for the sake of addition without stating that the assessee had failed to prove the identity and creditworthiness of Smt. Ram Kali Devi. The Tribunal also confirmed the findings with regard to entries of the demand draft in respect of M/s Mohit Agency.

Section 68 (of Income Tax Act, 1961) provides that where any sums are found credited in the books of an assessee maintained for any previous year, and the assessee offers no explanation about the nature and source thereof or the explanation offered by him is not in the opinion of the assessing officer satisfactory, the sum so credited may be charged to income tax as the income of the assessee of that previous year.

We do not find any error in the findings recorded by the appellate authority as confirmed by the Tribunal that the Assessing Officer did not record any finding regarding the explanation offered by the assessee. He did not record that the explanation was not found to be satisfactory.

We also find substance in the contention of Shri Krishna Ji Agrawal that the books of accounts were not rejected. Only additions were made without considering the explanation, which were found to be sufficient by the appellate authority. In our opinion, the questions raised do not arise for consideration. The findings recorded by the appellate authority and the Tribunal are findings of fact, which do not raise any question of law to be considered by the High Court.

The income tax appeal is dismissed.

Order Date :- 13.7.2012

×

Similar Ripples

Questions

Court Upholds Deletion of Tax Additions, Emphasizes Importance of Satisfactory Explanations

Write your CommentSimilar Posts

Generic

- Reportdata/5680.pdf