Court upholds nil value of shares, rejects Revenue's appeal on book profit calc…

Full News

Court upholds nil value of shares, rejects Revenue's appeal on book profit calculation

Court upholds nil value of shares, rejects Revenue's appeal on book profit calculation

This case involves a dispute between the Revenue (tax authorities) and Eicher Ltd. (the assessee) regarding the calculation of book profits under Section 115JA (of Income Tax Act, 1961). The Revenue's appeal was dismissed by the High Court, which agreed with the lower authorities that the value of the assessee's shares was nil and that no substantial question of law arose from the case.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs. Eicher Ltd. (High Court of Delhi)

ITA 1147/2007

Date: 28th November 2007

Key Takeaways

1. The court upheld the lower authorities' decision that the value of the assessee's shares was nil.

2. Explanation (c) to Section 115JA(1) (of Income Tax Act, 1961) was found inapplicable in this case.

3. The court emphasized the importance of substantial questions of law for appeals to be considered.

4. Previous judgments involving the same assessee can influence current decisions.

Issue

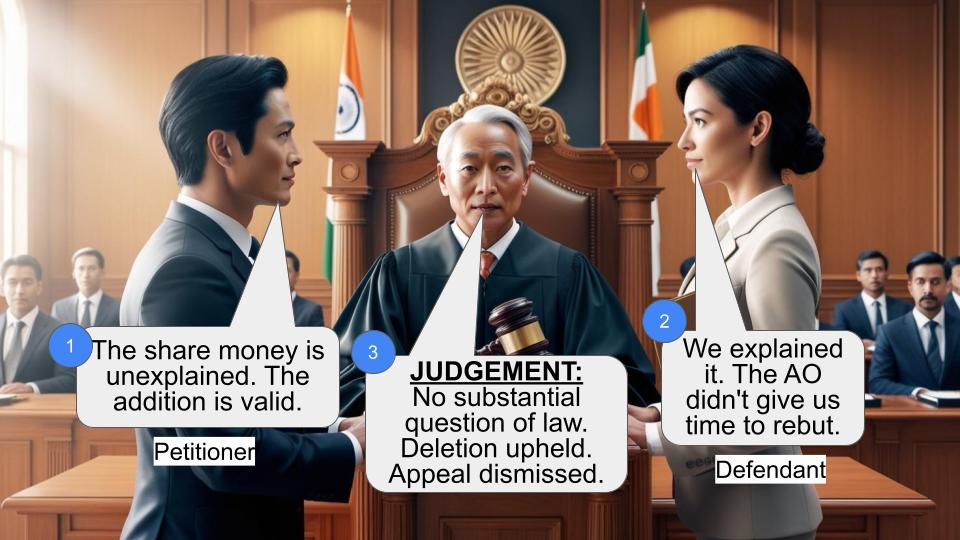

Did the Income Tax Appellate Tribunal err in deleting the addition of Rs. 52,00,000 from the book profit calculation under Section 115JA (of Income Tax Act, 1961), which the Assessing Officer had considered as a provision for diminution in the value of shares?

Facts

1. The case relates to the assessment year 2000-01.

2. The Revenue appealed against an order passed by the Income Tax Appellate Tribunal on January 25, 2007.

3. Two questions of law were raised by the Revenue before the High Court.

4. The first question concerned a provision of Rs. 3,58,65,172 made by the assessee for bad and doubtful debts.

5. The second question related to deleting the addition of Rs. 52,00,000, which the Assessing Officer considered a provision for diminution in the value of shares.

6. The assessee claimed that the value of their shares was nil, but this was not accepted by the Assessing Officer.

Arguments

Revenue's Argument:

- The Assessing Officer believed that the Rs. 52,00,000 should be added to the book profit calculation under Section 115JA (of Income Tax Act, 1961).

- They argued that Explanation (c) to Section 115JA(1) (of Income Tax Act, 1961) was applicable in this case.

Assessee's Argument:

- The value of their shares was nil.

- No provision was made for diminution in the value of shares.

- Explanation (c) to Section 115JA(1) (of Income Tax Act, 1961) was not applicable as there was neither a provision made nor an unascertained liability.

Key Legal Precedents

1. CIT vs. Eicher Ltd. (2006) 205 CTR (Del) 469 : (2006) 287 ITR 170 (Del) - This case, involving the same assessee, was cited regarding the first question about the provision for bad and doubtful debts. The court relied on this precedent to dismiss the first question.

Judgement

1. The court dismissed the appeal, finding no substantial question of law.

2. Regarding the first question about bad and doubtful debts, the court relied on its previous decision involving the same assessee.

3. On the second question, the court agreed with the CIT(A) and Tribunal that there was nothing to suggest the value of the assessee's shares was not nil.

4. The court found Explanation (c) to Section 115JA(1) (of Income Tax Act, 1961) inapplicable as there was neither a provision made by the assessee nor an unascertained liability.

FAQs

Q1: What is Section 115JA (of Income Tax Act, 1961) about?

A1: Section 115JA (of Income Tax Act, 1961) deals with the calculation of deemed income in relation to certain companies. It's about computing book profits for tax purposes.

Q2: Why was Explanation (c) to Section 115JA(1) (of Income Tax Act, 1961) found inapplicable in this case?

A2: The court found that there was neither a provision made by the assessee nor an unascertained liability, which are the conditions for Explanation (c) to apply.

Q3: What impact does this judgment have on the interpretation of share valuation for tax purposes?

A3: This judgment suggests that tax authorities should have concrete evidence to dispute a company's claim of nil share value. It emphasizes the importance of factual evidence in such disputes.

Q4: How did the previous case (CIT vs. Eicher Ltd. 2006) influence this decision?

A4: The previous case helped resolve the first question about the provision for bad and doubtful debts. It shows how courts often rely on their own previous decisions, especially when dealing with the same parties.

Q5: What does "no substantial question of law" mean in this context?

A5: It means that the court found no significant legal issue that required its intervention. The factual findings of the lower authorities were accepted, and no new legal principle needed to be established or clarified.

1. The Revenue is aggrieved by an order dt. 25th Jan., 2007 passed by the Income-tax Appellate Tribunal, Delhi Bench ‘G’, New Delhi (Tribunal) in ITA No. 3427/Del/2003 relevant for the asst. yr. 2000-01. The Revenue has raised two questions of law before us.

2. Insofar as the first question relating to a provision of Rs. 3,58,65,172 made by the assessee for bad and doubtful debts which could not be added to the book profit while computing deemed income under s. 115JA of the IT Act, 1961 (the Act) is concerned, learned counsel for the Revenue frankly submits that in view of the decision rendered by this Court in the case of the same assessee in CIT vs. Eicher Ltd. (2006) 205 CTR (Del) 469 : (2006) 287 ITR 170 (Del) , no substantial question of law arises.

3. The second question relates to deleting the addition of Rs. 52,00,000 said to be a provision made by the assessee for diminution in value of shares while computing the deemed income under s. 115JA of the Act. It appears that the value of the shares of the assessee was claimed to be nil but this was not accepted by the AO.

4. Both the Commissioner of Income-tax (Appeals) [CIT(A)] as well as the Tribunal were of the view that there was nothing to suggest that the value in shares of the assessee was not nil. Moreover, reliance placed by the AO on Expln. (c) to s. 115JA(1) of the Act was inapplicable because neither was there a provision made by the assessee nor was the liability an unascertained liability. There cannot be any dispute about this in view of the facts of the case and so the terms of Expln. (c) are not at all relevant.

5. No substantial question of law arises.

6. Dismissed.

MADAN B. LOKUR, J

S.

MURALIDHAR, J

NOVEMBER 28, 2007

×

Similar Ripples

Questions

Court upholds nil value of shares, rejects Revenue's appeal on book profit calculation

Write your CommentSimilar Posts

Generic

- Reportdata/5133.pdf