Court Upholds Reassessment: Undisclosed Property Sale Leads to Tax Scrutiny

Full News

Court Upholds Reassessment: Undisclosed Property Sale Leads to Tax Scrutiny

Court Upholds Reassessment: Undisclosed Property Sale Leads to Tax Scrutiny

This case involves a dispute between Chunibhai Ranchhodbhai Dalwadi (late) and the Assistant Commissioner of Income Tax. The core issue revolves around the validity of reassessment proceedings initiated by the tax authorities due to an undisclosed property sale. The High Court ultimately upheld the reassessment, ruling in favor of the tax department.

Get the full picture - access the original judgement of the court order here

Case Name:

Chunni bhai Ranchhod Bhai Dalwadi (Late) Vs Assistant Commissioner of Income Tax (High Court of Gujarat)

Special Civil Application No. 5376 of 2015

Date: 6th April 2015

Key Takeaways:

1. Failure to disclose full details of a property sale can lead to reassessment of income tax.

2. Section 50C (of Income Tax Act, 1961) can be invoked to treat the difference between declared sale value and stamp duty valuation as deemed long-term capital gain.

3. Reopening of assessment within four years is permissible if the assessee fails to disclose material facts fully and truly.

Issue:

Was the Income Tax Department justified in reopening the assessment based on the discovery of an undisclosed property sale?

Facts:

1. The assessee (Chunibhai Ranchhodbhai Dalwadi) sold an immovable property on April 19, 2006.

2. The declared sale value was Rs.87.71 lakhs (rounded off).

3. The sale deed was registered with the Sub-Registrar, Nadiad, with a registration charge of Rs.1.32 lakhs and stamp duty of Rs.11.92 lakhs.

4. Based on the stamp duty, the stamp authorities determined the sale value to be Rs.2.12 crores (rounded off).

5. The Assessing Officer noticed a difference of Rs.1.25 crores between the declared value and the stamp duty valuation.

6. The sale deed was not on record during the original assessment.

Arguments:

Assessing Officer's Argument:

- The assessee failed to disclose the true sale value of the property.

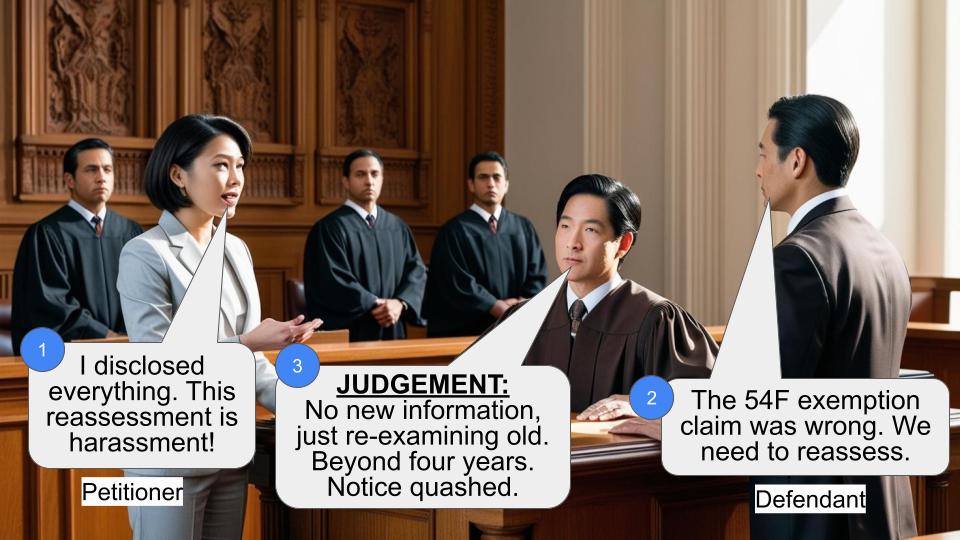

- Section 50C (of Income Tax Act, 1961) should be invoked to treat the difference as deemed long-term capital gain.

- Income chargeable to tax of Rs.1.25 crores had escaped assessment.

Assessee's Argument:

- The reassessment proceedings were invalid.

- The notice for reassessment was improper.

Key Legal Precedents:

The judgment doesn't explicitly mention any specific legal precedents. However, it refers to Section 50C (of Income Tax Act, 1961), which allows the stamp duty valuation to be considered as the full value of consideration for computing capital gains in certain cases.

Judgement:

1. The High Court upheld the validity of the reassessment proceedings.

2. The court found that the Assessing Officer had jurisdiction to reopen the assessment.

3. The failure to disclose the sale deed during the original assessment was deemed a failure to disclose material facts fully and truly.

4. Reopening the assessment within four years was found to be permissible under these circumstances.

5. The court left the contention about the invalidity or improper notice for the petitioner to raise in appellate proceedings if desired.

FAQs:

Q1: Why was the reassessment initiated?

A: The reassessment was initiated because the Assessing Officer discovered a significant difference between the declared sale value of a property and its valuation based on stamp duty.

Q2: What is Section 50C (of Income Tax Act, 1961)?

A: Section 50C (of Income Tax Act, 1961) allows tax authorities to use the stamp duty valuation of a property as the full value of consideration for computing capital gains, if it's higher than the declared sale value.

Q3: Why did the court allow the reopening of the assessment?

A: The court allowed it because the assessee failed to disclose the full details of the property sale during the original assessment, which is considered a failure to disclose material facts necessary for assessment.

Q4: What happens next for the assessee?

A: The assessee can raise contentions about the validity of the notice in appellate proceedings if they choose to do so.

Q5: Did the court address all the assessee's arguments?

A: The court didn't examine the contention about the invalidity or improper notice in this proceeding, leaving it for potential appellate proceedings.

1.00. Mr. K.M. Parikh, learned advocate appearing on behalf of the respondent - revenue prays for time. Mr. Divatia, learned advocate appearing on behalf of the petitioner - assessee has made a grievance that despite the specific order passed by this Court dated 27/3/2015, directing that final order, if any passed, may not be implemented till next date of hearing i.e. 6/4/2015, not only the Assessing Officer has passed re-assessment order, but has also issued Notice of Demand of Rs.67,41,200/- on the basis and/or pursuant to the reassessment order and thus, has implemented the reassessment order.

2.00. Considering the order passed by this Court dated 27/3/2015, though the assessing officer was permitted to pass final order, the same was not required to be implemented. Despite that, Notice of Demand under section 156 (of Income Tax Act, 1961) has been issued and served upon the petitioner assessee, which ought not to have been done by the Assessing Officer.

3.00. At this stage, Mr. Parikh, learned advocate appearing on behalf of the respondent – revenue, more particularly Assessing Officer, has stated at the bar that proper instructions shall be issued to the Assessing Officer to withdraw the Notice of Demand which has been issued pursuant to reassessment order.

4.00. So as to enable the respondent – revenue to file Affidavit-in-reply to the main petition, S.O. to 21/4/2015. Ad-interim relief granted earlier is directed to be continued till 23/4/2015. Affidavit-in-reply to be filed on or before 16/4/2015.

Sd/-

(M.R.SHAH, J.)

Sd/-

(S.H.VORA, J.)

×

Questions

Court Upholds Reassessment: Undisclosed Property Sale Leads to Tax Scrutiny

Write your CommentSimilar Posts

Generic

- Reportdata/2744.pdf