Court upholds tax additions, finds no perversity in Tribunal's order

Full News

Court upholds tax additions, finds no perversity in Tribunal's order

Court upholds tax additions, finds no perversity in Tribunal's order

This case involves an appeal against tax additions made by the Assessing Officer and upheld by the Income Tax Appellate Tribunal. The High Court reviewed the Tribunal's decision and found no reason to interfere, concluding that no question of law arose from the Tribunal's order.

Get the full picture - access the original judgement of the court order here

Case Name:

Sudhir Bhasin & Vijay Kumar Bhasin Vs Commissioner of Income Tax (High Court of Punjab & Haryana)

I.T.R. No. 69 and 69A of 1998

Date: 11th September 2007

Key Takeaways:

1. The High Court affirmed the Tribunal's decision to uphold tax additions.

2. The court emphasized the importance of satisfactory explanations for income sources.

3. The judgment highlights the limited scope for interference with Tribunal orders unless they are perverse or unwarranted.

Issue:

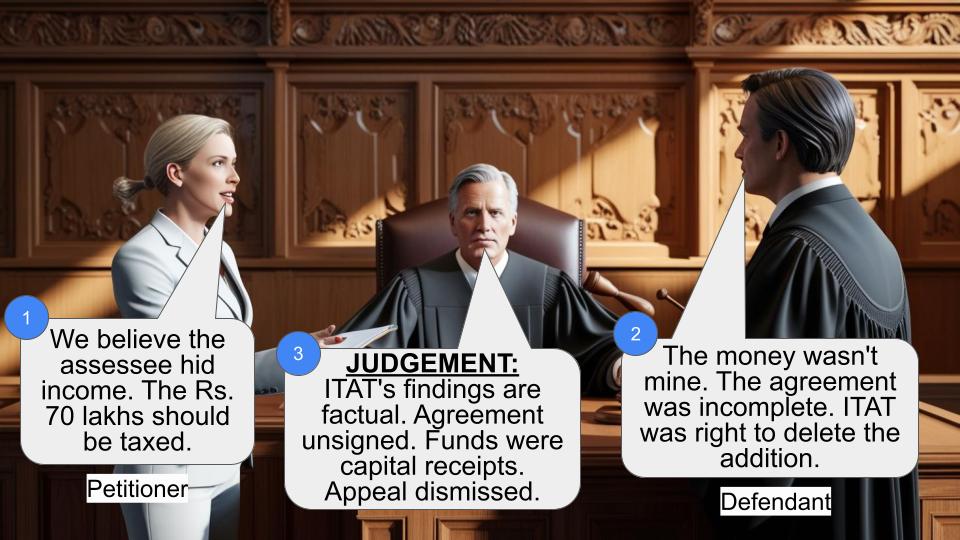

Whether the Income Tax Appellate Tribunal was correct in upholding the additions of Rs.15,000 and Rs.9,603 made by the Assessing Officer to the assessees' taxable income?

Facts:

1. The case pertains to the assessment year 1989-90.

2. The Assessing Officer made two additions to the assessees' taxable income:

a) Rs.15,000 each to Sudhir Bhasin and his brother Vijay Kumar Bhasin, totaling Rs.30,000.

b) Rs.9,603 each as unexplained cash found during a search on 5.5.1988.

3. The assessees appealed these additions to the Income Tax Appellate Tribunal.

4. The Tribunal passed a consolidated order on 28.7.1997 in I.T.A. Nos. 1573/91 and 1574/91.

Arguments:

While the specific arguments aren't detailed in the provided context, we can infer:

Assessees' argument:

- The additions made by the Assessing Officer were unjustified.

- They likely claimed to have satisfactorily explained the source of the Rs.30,000 and the Rs.9,603 found during the search.

Tax Department's argument:

- The additions were justified as the assessees failed to satisfactorily explain the source of the funds.

- The household expenses (Rs.9,603) found during the search were unexplained and thus taxable.

Key Legal Precedents:

The judgment doesn't mention specific legal precedents. However, it refers to Section 256(1) (of Income Tax Act, 1961), under which the Tribunal referred the questions of law to the High Court.

Judgement:

1. The High Court found that the Tribunal had categorically concluded that the assessee-applicant did not satisfactorily explain the source of Rs. 30,000.

2. The court agreed that the Assessing Officer was justified in taxing Rs.15,000 in the hands of each brother.

3. Regarding the Rs.9,603 addition, the court noted that the Tribunal found the Assessing Officer's addition on account of household expenses justified.

4. The High Court found no evidence to suggest that the additions were unwarranted or perverse.

5. The court concluded that no question of law arose for determination and returned the questions unanswered.

FAQs:

Q1: What were the main issues in this case?

A1: The main issues were the additions of Rs.15,000 each to two brothers' taxable income and Rs.9,603 each as unexplained cash found during a search.

Q2: Why did the High Court refuse to interfere with the Tribunal's decision?

A2: The High Court found no evidence that the Tribunal's decision was perverse or unwarranted. The Tribunal had provided clear reasons for upholding the additions.

Q3: What does this judgment mean for taxpayers?

A3: This judgment emphasizes the importance of providing satisfactory explanations for income sources and cash found during searches. It also shows that courts are unlikely to interfere with Tribunal decisions unless they are clearly perverse.

Q4: What is the significance of Section 256(1) (of Income Tax Act, 1961) in this case?

A4: This section allows the Tribunal to refer questions of law to the High Court. In this case, the Tribunal used this provision to refer the questions, but the High Court found no substantial question of law arose.

Q5: Can the assessees appeal this decision further?

A5: While the judgment doesn't mention further appeal options, generally, decisions of High Courts can be appealed to the Supreme Court if there's a substantial question of law. However, given that the High Court found no question of law arose, such an appeal might be challenging.

The Income Tax Appellate Tribunal, Chandigarh Bench, Chandigarh (for brevity, ‘the Tribunal’), by exercising its power under Section 256(1) (of Income Tax Act, 1961) (for brevity, ‘the Act’) has referred the following questions of law, which are stated to have emerged from consolidated order dated 28.7.1997, in I.T.A. Nos. 1573/91 and 1574/91, in respect of assessment year 1989-90:-

“i). Whether on the facts and circumstances of the case, the Tribunal has rightly upheld the addition of Rs.15,000/- on account of alleged advance received by the assessees from Sh. Nishan Singh?

ii) Whether on the facts and circumstances of the case, the Tribunal has rightly upheld the addition of Rs.9,603/- in case of each assessee as unexplained cash found during search on 5.5.1988?

A perusal of the consolidated order passed by the Tribunal shows that it has been categorically concluded that the assessee-applicant did not satisfactorily explained the source of Rs. 30,000/- and, therefore, the Assessing Officer was justified in taxing the amount of Rs. 15,000/- in his hand and Rs. 15,000/- in the hands of his brother Shri Vijay Kumar. The addition was accordingly confirmed. There is nothing on record to suggest that the additions are unwarranted or perverse. Likewise, in respect of addition of Rs. 9,603/- the finding recorded by the Tribunal is that the addition made by the Assessing Officer on account of household expenses was justified. Therefore, there is no room to conclude that any question of law would arise for determination of this Court. Accordingly, the questions are returned unanswered.

(M.M. KUMAR)

JUDGE

(AJAY KUMAR MITTAL)

September 11, 2007 JUDGE

×

Similar Ripples

Questions

Court upholds tax additions, finds no perversity in Tribunal's order

Write your CommentSimilar Posts

Generic

- Reportdata/5195.pdf