Court Upholds Tax Deduction Despite Delayed Building Use Permission

Full News

Court Upholds Tax Deduction Despite Delayed Building Use Permission

Court Upholds Tax Deduction Despite Delayed Building Use Permission

This case involves a dispute between the Commissioner of Income Tax and Tarnetar Corporation regarding a tax deduction claimed under section 80IB(10) (of Income Tax Act, 1961). The main issue was whether the assessee (Tarnetar Corporation) qualified for the deduction despite not receiving building use (BU) permission within the statutory timeframe. The High Court ultimately ruled in favor of the assessee, upholding the tax deduction.

Get the full picture - access the original judgement of the court order here

Case Name:

COMMISSIONER OF INCOME TAX VS TARNETAR CORPORATION

(High Court of Gujrat)

Date:12 September 2012

Key Takeaways:

1. Substantial compliance with statutory conditions can be sufficient for claiming tax deductions in certain cases.

2. Courts may take a lenient view on minor deviations if the primary purpose of the deduction is fulfilled.

3. The timing of Building Use (BU) permission is not always the sole determinant for completion of a housing project.

Issue:

Was the Appellate Tribunal correct in law and on facts in deleting the disallowance of deduction of Rs. 1,02,69,964/- made under section 80IB(10) (of Income Tax Act, 1961)?

Facts:

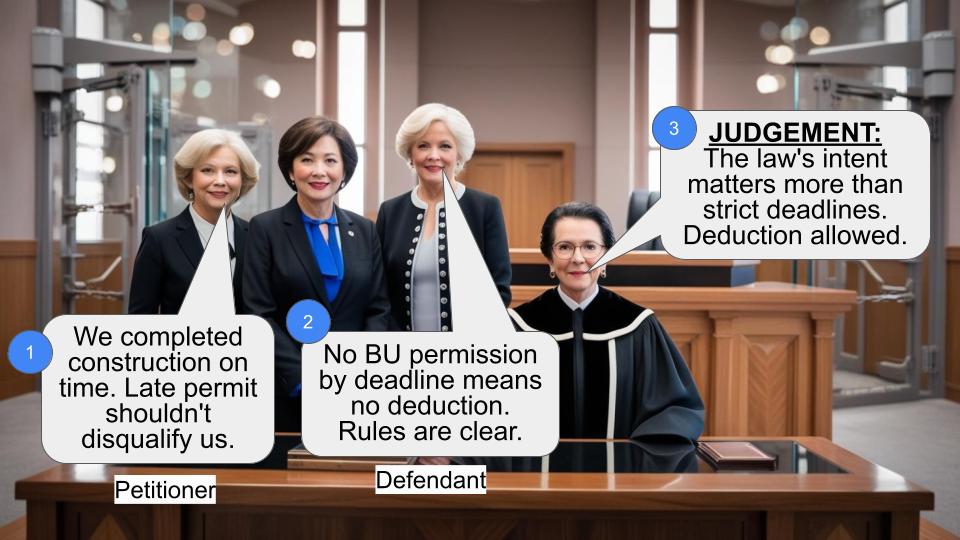

1. Tarnetar Corporation claimed a deduction under section 80IB(10) (of Income Tax Act, 1961) for developing a housing project.

2. The Assessing Officer initially denied this deduction.

3. The project approval was obtained before April 1, 2004, requiring completion by March 31, 2008.

4. Construction was completed in 2006, and the assessee applied for BU permission on February 15, 2006.

5. The initial BU permission application was rejected on July 1, 2006, for technical reasons.

6. Several residential units were occupied and sold before the March 31, 2008 deadline.

7. The assessee paid penalties to regularize the occupations without formal permission.

8. BU permission was eventually granted on March 19, 2009, after the statutory deadline.

Arguments:

Revenue's (Income Tax Department) arguments:

1. The assessee was not a developer and thus not qualified for the deduction.

2. The housing project wasn't completed within the statutory timeframe as BU permission was granted after March 2008.

Assessee's (Tarnetar Corporation) arguments:

1. They qualified as a developer and were eligible for the deduction.

2. The project was substantially completed before the deadline, despite the delayed BU permission.

Key Legal Precedents:

1. CIT v. Radhe Developers, (2012) 341 ITR 403 (Guj.): This case established that assessees in similar circumstances cannot be denied the benefit of deduction under section 80IB(10) (of Income Tax Act, 1961) .

Judgement:

The High Court ruled in favor of the assessee, upholding the Appellate Tribunal's decision. Key points of the judgment include:

1. The court dismissed the Revenue's argument about the assessee not being a developer, citing the CIT v. Radhe Developers case .

2. While acknowledging that the BU permission was granted after the deadline, the court noted that not every statutory condition should be seen as mandatory .

3. The court emphasized that substantial compliance can be sufficient if the primary purpose of the deduction is fulfilled .

4. The court considered the peculiar facts of the case, including that construction was completed two years before the deadline and that the initial BU permission rejection was not due to incomplete construction .

Based on these factors, the court concluded that granting the benefit of deduction was not illegal, and dismissed the Tax Appeal .

FAQs:

1. Q: What is section 80IB(10) (of Income Tax Act, 1961)?

A: Section 80IB(10) (of Income Tax Act, 1961) provides tax deductions for profits derived from developing and building housing projects, subject to certain conditions.

2. Q: Why was the timing of the BU permission important in this case?

A: The law linked the completion of construction to the granting of BU permission by the local authority. However, the court ruled that this wasn't the only factor to consider.

3. Q: What does "substantial compliance" mean in this context?

A: It means that while the assessee didn't strictly meet all conditions (like getting BU permission on time), they fulfilled the main purpose of the law by completing the construction and selling units before the deadline.

4. Q: Could this judgment affect other similar cases?

A: Yes, it could. This judgment suggests that courts may take a more flexible approach in interpreting tax deduction conditions, focusing on substantial compliance rather than strict adherence to all technical requirements.

5. Q: What's the significance of the CIT v. Radhe Developers case?

A: This case established a precedent that assessees in similar circumstances to Tarnetar Corporation should not be denied the benefit of deduction under section 80IB(10) (of Income Tax Act, 1961).

Revenue is in appeal against the judgment of the Tribunal dated 24.5.2011 raising following question for our consideration :

“Whether the Appellate Tribunal is right in law and on facts in deleting the disallowance of deduction of Rs.1,02,69,964/- made u/s.80IB(10) (of Income Tax Act, 1961) ?”

The issue pertains to deduction claimed by the assessee under section 80IB(10) (of Income Tax Act, 1961) on development of housing project. The Assessing Officer was of the opinion that such deduction was not justified. Revenue's stand appears to be that the assessee was not a developer and that therefore, would not be qualified for deduction under section 80IB(10) (of Income Tax Act, 1961). Additional contention of the Revenue was that the assessee did not fulfill one of the essential conditions required for claiming deduction under section 80IB(10) (of Income Tax Act, 1961). With respect to the first contention, the learned counsel for the Revenue candidly agree that such issue was discussed by this Court at considerable length in the case of CIT v. Radhe Developers, (2012) 341 ITR 403 (Guj.) and under similar circumstances held that the assessees cannot be denied the benefit of deduction. Without further elaboration, therefore, such contention is turned down.

With respect to the second contention, we may record that the contention of the Revenue is that the assessee did not complete the housing project within the statutory time frame. Under sub-clause (i) of clause (a) of section 80IB(10) (of Income Tax Act, 1961), the assessee since had got approval for the housing project from the local authority before 1st April 2004 was required to complete the construction latest by 31st March 2008. Relying on explanation (ii) to clause (i), Revenue contends that since BU permission was granted after March 2008, the construction must be deemed to have been completed after such date. Explanation (ii) reads as under:

“(ii) the date of completion of construction of the housing project shall be taken to be the date on which the completion certificate in respect of such housing project is issued by the local authority.”

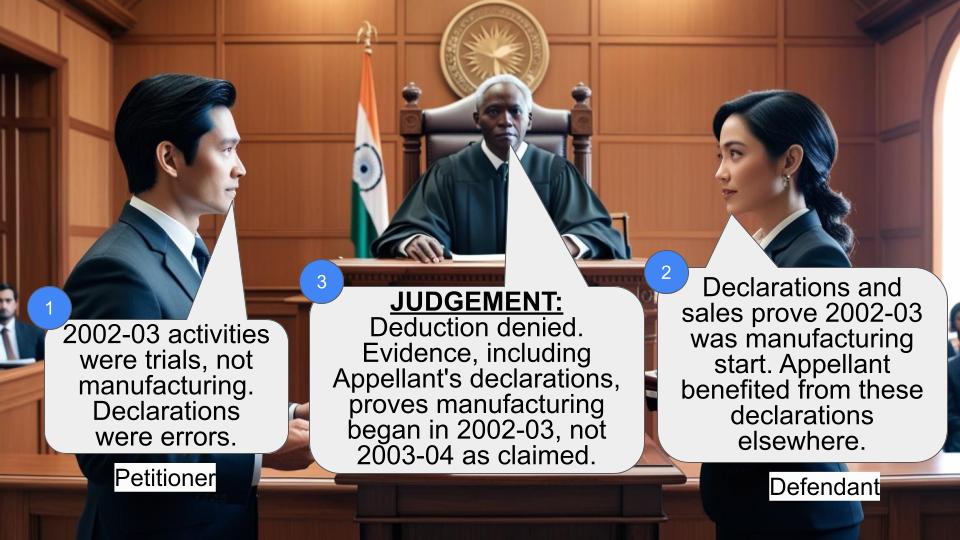

CIT (Appeals) as well as the Tribunal after detailed discussion came to the conclusion that such requirement was not mandatory in nature. In the present case, the assessee had completed the construction well before the last date, namely, 31st March 2008 and had also sold several units which was completed and actually occupied, and it also applied for BU permission to the local authority. The local authority, however, for technical reasons, at one stage rejected such application in the year 2006 and thereafter upon revised efforts from the assessee granted the same by order dated 19th March 2009.

We have perused the detailed discussion of the CIT (Appeals) as well as the Tribunal on the issue. In particular, the Tribunal noted that the construction was completed in 2006. Application for BU permission to the Municipal authorities was filed on 15.2.2006 which was rejected on 1.7.06. Several residential units were occupied since the same was done without necessary permission. The assessee had also paid penalty and got such occupation regularized. Several tenements were sold long before the last date.

In the present case, therefore, the fact that the assessee had completed the construction well before 31st March 2008 is not in doubt. It is, of course, true that formally BU permission was not granted by the Municipal Authority by such date. It is equally true that explanation to clause (a) to section 80IB(10) (of Income Tax Act, 1961) links the completion of the construction to the BU permission being granted by the local authority. However, not every condition of the statute can be seen as mandatory. If substantial compliance thereof is established on record, in a given case, the court may take the view that minor deviation thereof would not vitiate the very purpose for which deduction was being made available.

In the present case, the facts are peculiar. The assessee had not only completed the construction two years before the final date and had applied for BU permission. Such BU permission was not rejected on the ground that construction was not completed, but the some other technical ground. In that view of the matter, granting benefit of deduction cannot be held to be illegal.

In the result, the Tax Appeal is dismissed.

(Akil Kureshi, J.)

(Harsha Devani, J.)

×

Questions

Court Upholds Tax Deduction Despite Delayed Building Use Permission

Write your CommentSimilar Posts

Generic

- Reportdata/5458.pdf