Court Upholds Tax on Undisclosed Share Capital: Burden of Proof on Assessee

Full News

Court Upholds Tax on Undisclosed Share Capital: Burden of Proof on Assessee

Court Upholds Tax on Undisclosed Share Capital: Burden of Proof on Assessee

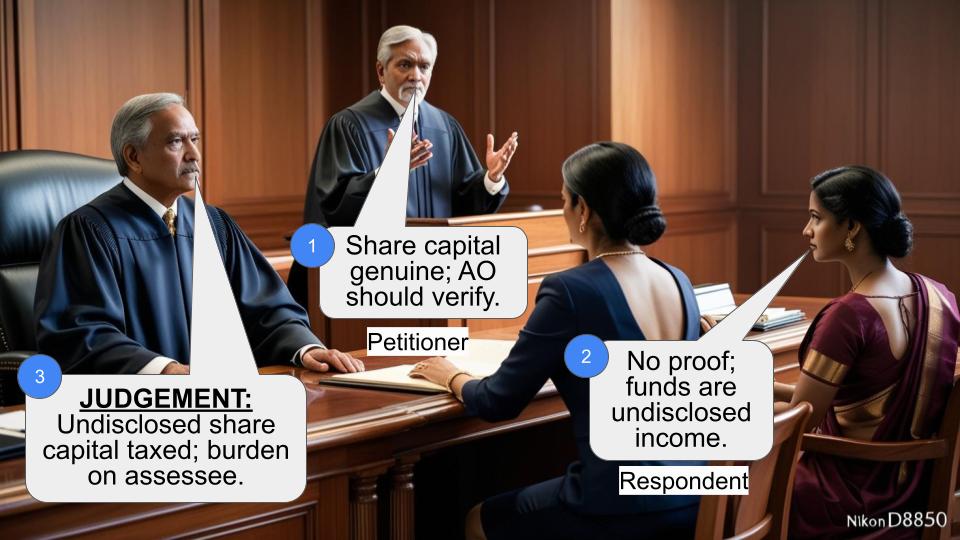

This case involves Sriman Sai Securities Investment Finance Limited (the assessee) and the Deputy Commissioner of Income Tax. The dispute centered around whether Rs.48,58,000 claimed as share capital should be treated as undisclosed income. The court upheld the decision to treat this amount as taxable income from undisclosed sources, as the assessee failed to provide sufficient evidence to prove it was legitimate share capital.

Get the full picture - access the original judgement of the court order here

Case Name:

Sriman Sai Securities Investment Finance Limited Vs Deputy Commissioner of Income Tax (High Court of Andhra Pradesh)

ITTA No. 137 of 2005

Date: 20th December 2017

Key Takeaways:

1. The burden of proof lies initially with the assessee to explain the nature and source of cash credits.

2. Failure to provide satisfactory evidence can result in the amount being treated as undisclosed income.

3. The Assessing Officer (AO) has wide powers to examine the real nature of transactions.

4. Mere submission of a list of alleged shareholders is insufficient without supporting documentation.

Issue:

Was the Assessing Officer correct in treating the sum of Rs.48,58,000 as the assessee's income from undisclosed sources, rather than legitimate share capital?

Facts:

1. The assessee claimed that Rs.48,58,000 was collected as share capital from 464 persons.

2. The AO gave the assessee 16 opportunities to submit books of accounts, vouchers, and confirmation letters from purported shareholders.

3. The assessee only provided a list of alleged shareholders, without any supporting documentation.

4. The AO treated the amount as income from undisclosed sources and computed tax accordingly.

5. The assessee's appeals to the Commissioner of Income Tax (Appeals-II) and the Income Tax Appellate Tribunal were unsuccessful.

Arguments:

Assessee's arguments:

1. It's the AO's duty to conduct a necessary inquiry before concluding on the nature of the amount.

2. Relied on the judgment in Commissioner of Income Tax Vs. Stellar Investment Limited and a Supreme Court order confirming this decision.

3. Also cited the judgment in Commissioner of Income Tax Vs. LANCO Industries Limited.

Tax Department's arguments:

1. Under Section 68 (of Income Tax Act, 1961), the initial burden lies on the assessee to satisfy the AO about the nature of cash credits.

2. The assessee failed to produce any material despite numerous opportunities.

3. No addresses were provided for most alleged shareholders, and no attempt was made to secure their statements.

4. No books of accounts or vouchers were filed to prove the receipt of money.

Key Legal Precedents:

1. Hindusthan Tea Trading Company Limited Vs. Commissioner of Income Tax: Established that the AO has wide powers to examine the real nature of transactions.

2. Commissioner of Income Tax Vs. Stellar Investment Limited: Observed that share capital shouldn't be regarded as undisclosed income even if subscribers were not genuine. However, this judgment didn't discuss Section 68 (of Income Tax Act, 1961).

3. Commissioner of Income Tax Vs. LANCO Industries Limited: Held that to add unexplained investments to the assessee's income, there must be a finding that shareholders were mere name-lenders.

Judgement:

The court dismissed the assessee's appeal, holding that:

1. The assessee failed to discharge its initial burden of proving the money was collected through share capital.

2. The AO was justified in treating the sum as income from undisclosed sources and charging it to tax.

3. Both lower appellate forums correctly confirmed the AO's order.

FAQs:

1. Q: What is Section 68 (of Income Tax Act, 1961)?

A: Section 68 (of Income Tax Act, 1961) allows the AO to charge unexplained cash credits to income tax if the assessee fails to satisfactorily explain their nature and source.

2. Q: What evidence should the assessee have provided?

A: The assessee should have provided books of accounts, vouchers, receipts, bank statements, and confirmation letters from shareholders.

3. Q: Can share capital ever be treated as undisclosed income?

A: Yes, if the assessee fails to provide satisfactory evidence of its legitimacy, it can be treated as undisclosed income.

4. Q: What are the implications of this judgment for companies raising share capital?

A: Companies must maintain proper documentation and be prepared to provide evidence of the legitimacy of their share capital if questioned by tax authorities.

5. Q: How does this judgment affect the burden of proof in tax cases?

A: It reinforces that the initial burden of proof lies with the assessee to explain the nature and source of funds, before the onus shifts to the tax department.

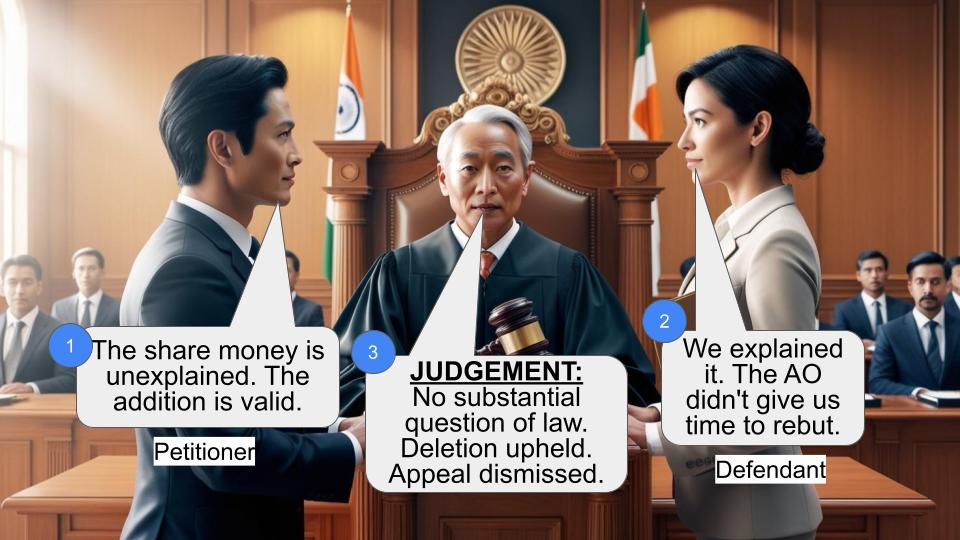

The assessee, being unsuccessful before both the lower appellate fora, filed this appeal by raising the following substantial question of law:

"Whether on the facts and circumstances of the case the Hon'ble Income Tax Appellate Tribunal is right in sustaining the order of the CIT (Appeals) who confirmed the order of the assessing authority treating the entire share capital of the assessee/appellant as its income without conducting any enquiry in that regard."

One of the two issues decided against the assessee, in respect of which this appeal is field, is whether the Assessing Officer (for short, 'A.O.') was correct in treating the sum of Rs.48,58,000/- as the assessee's income from undisclosed sources. The assessee has taken the stand before the A.O. that the said money was collected through share capital from 464 persons. The A.O. has given the assessee an opportunity of submitting books of accounts, vouchers and confirmation letters of the purported shareholders. Despite having been given as many as 16 opportunities, the assessee did not file any of those documents except giving a list of the purported shareholders. In such circumstances, the A.O. has computed the income treating the said amount as the income from undisclosed sources. This decision of the A.O. was unsuccessfully challenged by the appellant before the Commissioner of Income Tax (Appeals-II), Hyderabad, as well as before the Income Tax Appellate Tribunal, Hyderabad Bench 'A', Hyderabad (for short, 'the Tribunal').

2. At the hearing, Sri A.V.A.Siva Kartikeya, learned counsel for the appellant, has submitted that it is the duty and obligation of the A.O. to hold necessary inquiry before coming to a conclusion on the nature of the amount. In support of his submission, he has placed reliance on the judgment of Delhi High Court in Commissioner of Income Tax Vs. Stellar Investment Limited1 and also the order dated 20-07-2000 of the Supreme Court confirming the said decision. Learned counsel has also referred to and relied on the judgment of a Division Bench of this Court in Commissioner of Income Tax Vs. LANCO Industries Limited2 .

3. Opposing the above submissions, Ms. M.Lalitha, learned counsel, representing Ms. K.Mamata, learned senior standing counsel appearing for Income Tax Department, has submitted that under Section 68 (of Income Tax Act, 1961) (for short, 'the Act'), the initial burden lies on the assessee to satisfy the A.O. that the amount found as cash credit is not chargeable to income tax as the income of the assessee of the previous year and that notwithstanding a number of opportunities presented to the assessee by the A.O., the former failed to avail such opportunities and produce any material whatsoever to satisfy the A.O. in that regard. She has also submitted that except furnishing the names of the persons who allegedly contributed to the share capital, not even their addressees have been furnished and no attempt whatsoever was made by the assessee to secure statements of the said persons. She has further submitted that the assessee has not filed any books of accounts or vouchers proving the receipt of money from the said 464 persons in support of his plea that the amount was collected from them towards share capital. She has relied on the judgments of Calcutta High Court in Hindusthan Tea Trading Company Limited Vs. Commissioner of Income Tax3 and also the Jaipur Bench of Rajasthan High Court in Commissioner of Income Tax Vs. ARL Infratech Limited4 .

4. We have carefully considered the respective submissions of learned counsel for both parties and perused the record.

5. Section 68 (of Income Tax Act, 1961), as it stood before provisos were added, reads as follows:

"Where any sum is found credited in the books of an assessee maintained for any previous year, and the assessee offers no explanation about the nature and source thereof or the explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory, the sum so credited may be charged to income tax as the income of the assessee of that previous year."

It is evident from the said provision, where assessee offers no explanation about the nature and source of the cash credit or the explanation offered by him is not, in the opinion of the A.O., satisfactory, such cash credit is liable to be charged to income tax as the income of the assessee of the previous year. As concurrently found by all the fora below including the A.O., a number of opportunities were given to the assessee to substantiate its stand that the amount was collected towards allotment of shares to third parties. Except submitting a list of the persons from whom share capital was allegedly collected, no other material, such as books of accounts, vouchers, receipts or bank statements etc., was produced. A perusal of the list during hearing shows that except in a very few cases, even door numbers of the persons shown in the list have not been furnished. In Hindusthan Tea Trading Company Limited (3rd supra), the High Court of Calcutta held that the extent of the power of the A.O. while considering the material produced by the assessee is very wide and that the A.O. is empowered to lift the corporate veil and examine the real nature of the transaction and in the process, it may exercise its power of examining the material and it may require the assessee to produce further material if so required. The Court further held that the process of enquiry is such that the assessee has to offer the explanation and produce the material in support of such explanation and that only in such case, the onus shifts to the Revenue to scrutinize the material and form an opinion on the basis thereof. No doubt, the High Court of Delhi in Stellar Investment Limited (1st supra) observed that even assuming that the subscribers to the increased share capital were not genuine, nevertheless, under no circumstances, can the amount of share capital be regarded as undisclosed income of the assessee. We find from this order that no reference to Section 68 (of Income Tax Act, 1961) or discussion thereon has been undertaken. Though the Supreme Court has dismissed the civil appeal filed against the said order, no ratio as such has been laid down therein. In LANCO Industries Limited (2nd supra), a Division Bench of this Court held that if the ostensible shareholders failed to explain the means of investment, that should have been treated as unexplained income in their hands and in order to add it to the income of the assessee, there must be a further finding that in fact the shareholders were mere name-lenders and the money allegedly invested by them really belonged to the directors of the assessee company. The Court further held that in the absence of a finding that the persons to whom the share certificates were issued on receipt of consideration as per the book entries were in fact dummies or stooges of the directors of the assessee company, the same cannot be treated as unaccounted income of the assessee. In that case, the assessee produced relevant material such as confirmation letters from the shareholders and all other relevant material and the A.O. termed the material as stereotyped without rendering a finding that the shareholders were mere name-lenders.

6. In the light of the provisions of Section 68 (of Income Tax Act, 1961) and the legal position referred to above, we are of the opinion that the assessee has failed to discharge its initial burden to prove that the money of Rs.48,58,000/- was collected through share capital.

Therefore, the A.O. is wholly justified in rejecting the stand of the assessee and treating the sum of Rs.48,58,000/- as the income from undisclosed sources and accordingly charging the same to tax. Both the lower appellate fora and in our view rightly confirmed the order of the A.O.

7. For the aforementioned reasons, the question of law framed by the assessee is held against it. The appeal is accordingly dismissed.

C.V.NAGARJUNA REDDY, J.

M.S.K.JAISWAL, J.

Date: 20-12-2017. Note:

L.R. Copies to be marked. B/O

×

Questions

Court Upholds Tax on Undisclosed Share Capital: Burden of Proof on Assessee

Write your CommentSimilar Posts

Generic

- Reportdata/HC-AP-137-2005.pdf