Court Upholds Tribunal's Decision on Income Tax Reassessment, Dismisses Revenue…

Full News

Court Upholds Tribunal's Decision on Income Tax Reassessment, Dismisses Revenue's Appeal

Court Upholds Tribunal's Decision on Income Tax Reassessment, Dismisses Revenue's Appeal

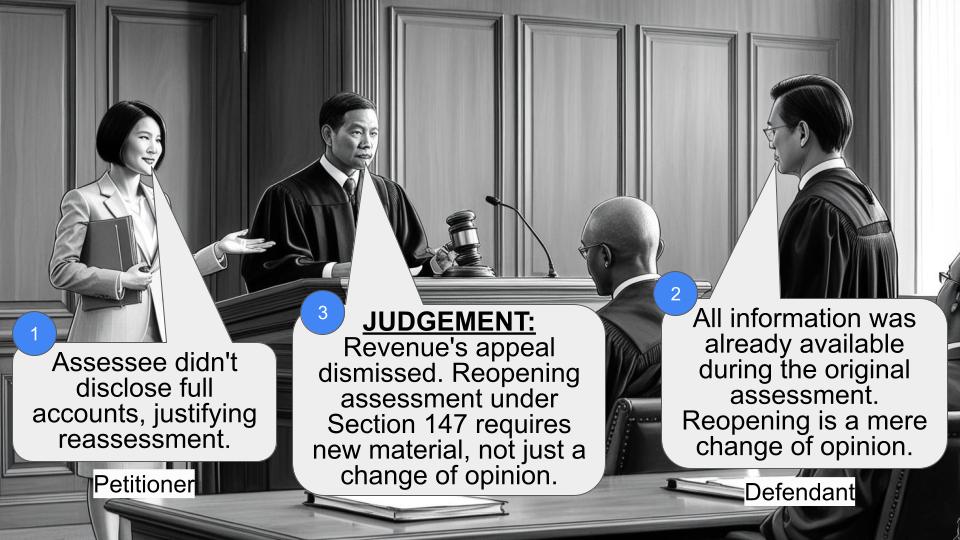

This case involves appeals by the revenue department challenging orders of the Income Tax Appellate Tribunal (ITAT) in Ahmedabad. The ITAT had dismissed the revenue's appeal and allowed the assessee's cross-objection regarding the reopening of an assessment under Section 147 (of Income Tax Act, 1961). The High Court upheld the Tribunal's decision, ruling in favor of the assessee and dismissing the revenue's appeals.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs. Akshar Enterprises (High Court of Gujarat)

Tax Appeal No. 1914 & 1917 of 2009

Date: 20th July 2016

Key Takeaways:

1. Mere change of opinion does not justify reopening an assessment under Section 147 (of Income Tax Act, 1961).

2. The court emphasized the importance of having new material or change in law to invoke Section 147 (of Income Tax Act, 1961).

3. The judgment reinforces the principle that tax authorities cannot use Section 147 (of Income Tax Act, 1961) to review their own decisions without substantial reasons.

Issue:

Whether the Income Tax Appellate Tribunal erred in interpreting Section 147 (of Income Tax Act, 1961), by ruling that the Assessing Officer could not reopen the assessment for the relevant year?

Facts:

1. The assessee, a partnership firm, was involved in constructing a township with M/s. Akshar Corporation.

2. A search and seizure operation was conducted on 14.2.1994, where a partner admitted to charging 40% on-money for flat sales.

3. A survey under Section 133A (of Income Tax Act, 1961) was conducted on 24.3.1999, obtaining a trial balance printout.

4. The assessee filed a return for the Assessment Year 1999-2000, showing booking receipts of Rs. 93,56,713/-.

5. The trial balance showed booking receipts of Rs. 1,13,32,043/-, a difference of Rs. 19,75,330/-.

6. The Assessing Officer reopened the assessment under Section 147 (of Income Tax Act, 1961) and added the difference to the total income.

7. The Commissioner of Income Tax (Appeals) partly allowed the assessee's appeal.

8. The ITAT dismissed the revenue's appeal and allowed the assessee's cross-objection.

Arguments:

Revenue's Argument:

- The Tribunal erred in holding that the Assessing Officer couldn't reopen the assessment under Section 147 (of Income Tax Act, 1961).

- The case involved non-disclosure of full and truthful accounts by the assessee, justifying reassessment.

Assessee's Argument:

- All particulars were already on record and considered in the original assessment.

- The reopening was based on a mere change of opinion, which is not valid grounds for reassessment.

Key Legal Precedents:

1. Indian and Eastern Newspaper Society v. CIT (1979) 119 ITR 996 (SC)

2. A.L.A. Firm v. CIT (1991) 189 ITR 285 (SC)

3. CIT v. Rao Thakur Narayan Singh (1965) 56 ITR 234, 239 (SC)

4. Garden Silk Mills Pvt. Ltd. (1999) 237 ITR 668 (Gujarat HC)

5. CIT v. Kelvinator of India Ltd. (2002) 256 ITR 1 (Delhi HC)

These precedents establish that mere change of opinion or re-examination of existing material does not justify reopening an assessment under Section 147 (of Income Tax Act, 1961).

Judgement:

The High Court dismissed the revenue's appeals, ruling in favor of the assessee. The court held that:

1. The Tribunal did not err in interpreting Section 147 (of Income Tax Act, 1961).

2. There was no change in law or new material to justify reopening the assessment.

3. The case was a mere change of opinion, which doesn't provide jurisdiction to invoke Section 147 (of Income Tax Act, 1961).

FAQs:

1. Q: What is Section 147 (of Income Tax Act, 1961)?

A: Section 147 (of Income Tax Act, 1961) allows for reassessment of income that has escaped assessment, subject to certain conditions.

2. Q: Can an assessment be reopened based on a change of opinion?

A: No, mere change of opinion does not justify reopening an assessment under Section 147 (of Income Tax Act, 1961).

3. Q: What conditions must be met to reopen an assessment under Section 147 (of Income Tax Act, 1961)?

A: There must be either new material or a change in law that suggests income has escaped assessment.

4. Q: How does this judgment impact tax assessments?

A: It reinforces the principle that tax authorities cannot arbitrarily reopen assessments without substantial reasons, protecting taxpayers from unwarranted reassessments.

5. Q: What is the significance of the cited legal precedents?

A: They establish and reinforce the principle that mere change of opinion or re-examination of existing material does not justify reopening an assessment under Section 147 (of Income Tax Act, 1961).

1. By way of these appeals, the revenue has challenged the order of the Income Tax Appellate Tribunal, Ahmedabad Bench “D”, Ahmedabad (For short, “the Tribunal”) in ITA No.36/Ahd/2006 with CO No.50/Ahd/2006, ITA No.41/Ahd/2006 with CO No.51/Ahd/2006 dated 17.4.2009, whereby the appeal filed by the revenue was dismissed and the cross-objection of the assessee was allowed.

2. As per the facts of Tax Appeal No.1914 of 2009, the respondent is a partnership firm and it undertook the work to construct a township with one firm, M/s.Akshar Corporation. A search and seizure operation was carried out on 14.2.1994 and statement of partner of the assessee, Shri Vireshbhai D. Patel was recorded wherein he admitted that 40% on-money was charged in respect of sale of flats. Thereafter, a survey operation under Section 133A (of Income Tax Act, 1961) was conducted on 24.3.1999 and a print-out of trial balance was also obtained from the assessee. The assessee filed return of income for the Assessment Year 1999-2000 and the Assessment Officer determined the total income of the assessee to be at Rs.11,13,180/-. Thereafter, the Assessing Officer found that the assessee has shown the receipt against booking of flats at Rs.93,56,713/- in the balance-sheet filed with the return, whereas, in the trial balance obtained at the time of survey on 24.3.1999, the same was shown as Rs.1,13,32,043/-. Thus, the assessee has shown Rs.19,75,330/- less in the return. The Assessing Officer, therefore, recorded reasons as required under Section 147 (of Income Tax Act, 1961) and, thereafter, issued notice directing the assessee to file its return for the Assessment Year on 24.3.2004 and initiated re-assessment. Vide Assessment order dated 28.3.205, the Assessing Officer determined total income of the assessee at Rs.30,88,510/- by making addition of difference of booking amount being Rs.19,75,330/-. Against said order, the assessee preferred an appeal before the Commissioner of Income Tax (Appeals), who vide order dated 28.10.2005 partly allowed the appeal of the assessee and deleted addition made by the Assessing Officer. Against the said order, the department preferred an appeal before the Income Tax Appellate Tribunal while the assessee filed Cross Objection No.50/Ahd/2006 in the said Appeal. Both the appeal and the Cross Objection were disposed of by the impugned order, whereby the appeal of the revenue was dismissed and the cross objection of the assessee was allowed.

3. At the time of admission of the Appeals, following question of law was framed:-

“"Whether the learned Tribunal below committed substantial error of law in misinterpreting the provision of Section 147 (of Income Tax Act, 1961) ["the Act"] by overlooking the fact that this is a case of non-disclosure of full and truthful account by the assessee and thus the case is covered under Section 147 (of Income Tax Act, 1961)."

4. Mr.Sudhir Mehta, learned advocate for the appellant submitted that the Tribunal has committed a serious error in holding that under Section 147 (of Income Tax Act, 1961), the Assessing Officer could not have reopened the assessment for the relevant year. He has relied upon the observations of the Commissioner of Income Tax (Appeals), wherein he has observed as under:-

“The first ground of appeal is regarding reopening of assessment u/s.147 (of Income Tax Act, 1961). The ld. AR stated that the conditions required for valid reopening of assessment were not satisfied. The AO observed that on verifying the assessment record for A.Y. 1999-2000, it was seen that the booking amount as per balance sheet filed was Rs.93,56,713/- and as per trial balance it was Rs.1,13,32,043/- which means there was a difference of Rs.19,75,330/- in the booking amount. In the original order the AO had discussed that the firm had been charging “on money” of Rs.13,16,886/- which was added while computing the total income but, the difference between trial balance and balance sheet filed was not added. He therefore, reopened the assessment u/s.147 (of Income Tax Act, 1961).

Before me, the ld.A.R. submitted that all the particulars were already on record and considered and what had now happened was a mere change of opinion or rather taking a different view on the same facts considered by the AO in the course of the original assessment. Reconciliation between the two figures was also shown and there was no need for any addition nor any valid ground for this reopening.

I have considered the submissions and do not agree with the appellant on this count. As per explanation 1 to Section 147 (of Income Tax Act, 1961), production before the AO of account books or rather evidence from which material evidence could with due diligence have been discovered by the AO will not necessarily amount to disclosure of all materials facts necessary for the assessment. In the instant case, the AO had reasons to believe that income chargeable to tax had escaped assessment due to difference between the balance sheet and the trial balance and therefore came to the conclusion that prima-facie, income chargeable to tax had escaped assessment within the meaning of section 147 (of Income Tax Act, 1961). Therefore the reopening of assessment is valid and this ground is dismissed.”

4.1 He submitted that the Tribunal has committed an error while passing the impugned orders, therefore, these appeals are required to be allowed by setting aside impugned orders.

5. Mr.Manish Shah, leaned counsel for the respondent contended that the Tribunal has not committed any error while passing the impugned order. He has relied upon following observations of the Tribunal in the impugned order:-

“8.3 The scope and effect of section 147 (of Income Tax Act, 1961) as substituted with effect from April 1, 1989, as also sections 148 to 152 are substantially different from provisions as they stood prior to such substitution. Under the old provisions of section 147 (of Income Tax Act, 1961), separate clauses (a) and (b) laid down the circumstances under which income escaping assessment for the past assessment years could be assessed or re- assessed. To confer jurisdiction under section 147(a) (of Income Tax Act, 1961) two conditions were required to be satisfied firstly the Assessing Officer must have reason to believe that income profits or gains chargeable to income tax have escaped assessment, and secondly he must also have reason to believe that such escapement occurred due to reason of either omission or failure on the part of the taxpayer to disclose fully or truly all material facts necessary for his assessment of that year. Both these conditions were conditions precedent to be satisfied before the Assessing officer could have jurisdiction to issue notice because the opinion formed earlier by himself (or more often, by a predecessor-Income-tax officer), was in his opinion, incorrect, judicial decisions have consistently held that this could not be done. (see Indian and Eastern Newspaper Society v. CIT (1979) 119 ITR 996 (SC) and A.L.A. Firm v. CIT (1991) 189 ITR 285 (SC).

The power to reopen an assessment was conferred by the Legislature not with the intention to enable the Income-tax officer to reopen the final decision made against the Revenue in respect of questions that directly arose for decision in earlier proceedings. If that were not the legal position it would result in placing an unrestricted power of review in the hands of the assessing authorities depending on their changing moods. (See CIT v. Rao Thakur Narayan Singh (1965) 56 ITR 234, 239 (SC)”.

8.5 Admittedly, in the case under consideration there is no change of law and no fresh material has come on record enabling the AO to invoke the powers under section 147 (of Income Tax Act, 1961). The instant case is a case of mere change of opinion which does not provide jurisdiction to the AO to initiate proceedings under section 147 (of Income Tax Act, 1961). We may also refer to a decision of the Hon'ble Gujarat High Court in Garden Silk Mills Pvt. Ltd. (1999) 237 ITR 668, while expressing similar views observed.

“The reasons recorded by the Assessing officer which led to the belief about the escapement of assessment disclose that the present case is nothing but mere change of opinion on the facts which were already before the Assessing officer while making the first assessment to which conscious application of mind as reflected from the proceedings, and allowed in the computation and which has not been disputed by the Revenue.” 8.6 Similarly in CIT v. Kelvinator of India Ltd. (2002) 256 ITR 1 (Delhi), Hon'ble Delhi High Court held that section 147 (of Income Tax Act, 1961) does not postulate conferment of power upon the Assessing officer to initiate reassessment proceedings upon his mere change of opinion. Hon'ble Court further observed as follows:

“We also cannot accept the submission of Mr.Jolly to the effect that only because in the assessment order, detailed reasons have not been recorded an analysis of the materials on the record by itself may justify the Assessing Officer to initiate a proceeding under section 147 (of Income Tax Act, 1961). The said submission is fallacious. An order of assessment can be passed either in terms of sub-section (1) of section 143 (of Income Tax Act, 1961) or sub-sec. (3) of section 143 (of Income Tax Act, 1961). When a regular order of assessment is passed in terms of the said sub- section (3) of section 143 (of Income Tax Act, 1961) a presumption can be raised that such an order has been passed on application of mind. It is well known that a presumption can also be raised to the effect that in terms of clause (e) of section 114 of the Indian Evidence Act judicial and official act have been regularly performed. If it held that an order which has been passed purportedly without application of mind would itself confer jurisdiction upon the Assessing officer to reopen the proceeding without anything further, the same would amount to giving a premium to an authority exercising quasi-judicial function to take benefit of its own wrong”.

5.1 He submitted that the Tribunal has rightly relied upon the aforesaid decisions and disposed of the appeals as well as cross objections by passing the impugned order, which is just and proper and the present appeals may be dismissed.

6. We have heard both the learned counsel. We have also gone through the materials on record and the judgments relied upon by the Tribunal while passing the impugned orders. Learned advocate for the appellant is not in a position to dispute the decisions relied upon by the Tribunal at the time of passing the impugned orders. Therefore, applying this ratio, in our view, the Tribunal has not committed an error while passing the impugned orders. Accordingly, all these appeals are dismissed. The question posed for our consideration is answered in favour of the assessee and against the revenue and it is held that the Tribunal has not committed any error in interpreting the provision of Section 147 (of Income Tax Act, 1961).

Sd/-

(K.S.JHAVERI, J.)

Sd/-

(G.R.UDHWANI, J.)

×