Court Upholds Tribunal's Decision on Interest-Free Funds Availability

Full News

Court Upholds Tribunal's Decision on Interest-Free Funds Availability

Court Upholds Tribunal's Decision on Interest-Free Funds Availability

The High Court dismissed appeals by the revenue department, affirming the Income Tax Appellate Tribunal's decision to delete disallowances of interest made by the Assessing Officer under section 36(1)(iii) (of Income Tax Act, 1961). The court ruled in favor of the assessee, agreeing that interest-free funds were available for non-business purposes.

Get the full picture - access the original judgement of the court order here.

Case Name:

Commissioner of Income Tax vs. Torrent Leasing & Finance Pvt. Ltd (High Court of Gujarat)

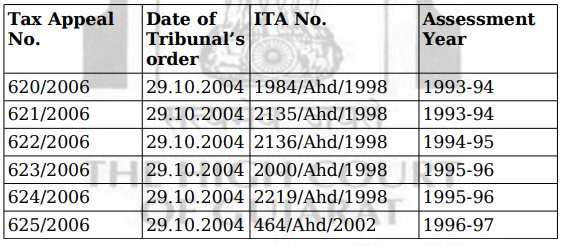

Tax Appeal No. 620 of 2006

Date: 17th December 2014

Key Takeaways:

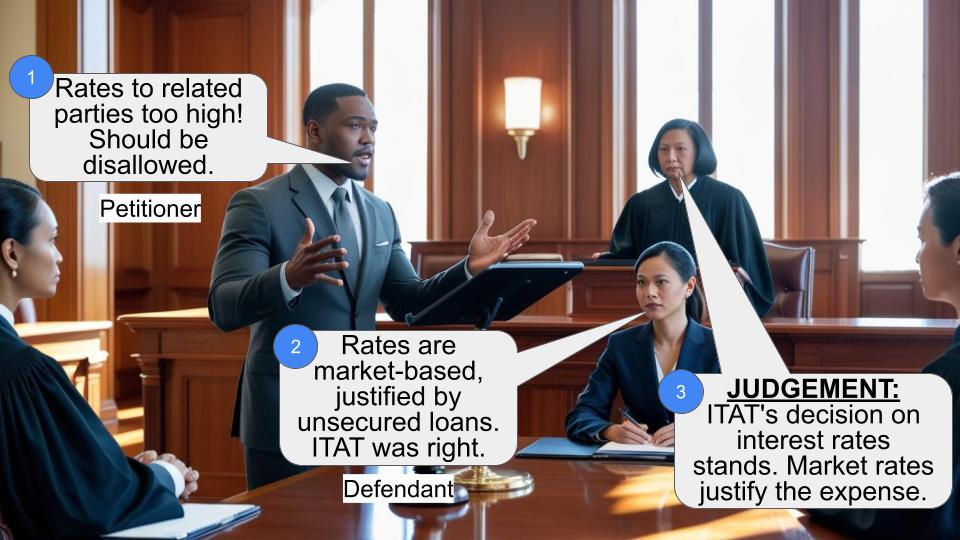

1. If total interest-free advances (including partners' debit balances) don't exceed total interest-free funds available, no interest is disallowable for non-business use of funds.

2. The court affirmed the principle that investments are presumed to be made from interest-free funds if such funds are sufficient.

3. Commercial expediency is a key factor in determining the allowability of interest on borrowed funds.

Issue:

Whether the Income Tax Appellate Tribunal was correct in law and facts in holding that interest-free funds were available with the assessee, thereby deleting the disallowance of interest made by the Assessing Officer under section 36(1)(iii) (of Income Tax Act, 1961)?

Facts:

1. The assessees filed income tax returns for the relevant assessment years.

2. During assessment, the Assessing Officer made disallowances/additions regarding interest amounts and stamp charges.

3. The assessees appealed to the CIT(A), which partly allowed the appeals.

4. Both the assessee and revenue appealed to the Tribunal, which deleted the disallowance of interest amount.

5. The revenue department challenged the Tribunal's decision in the High Court.

Arguments:

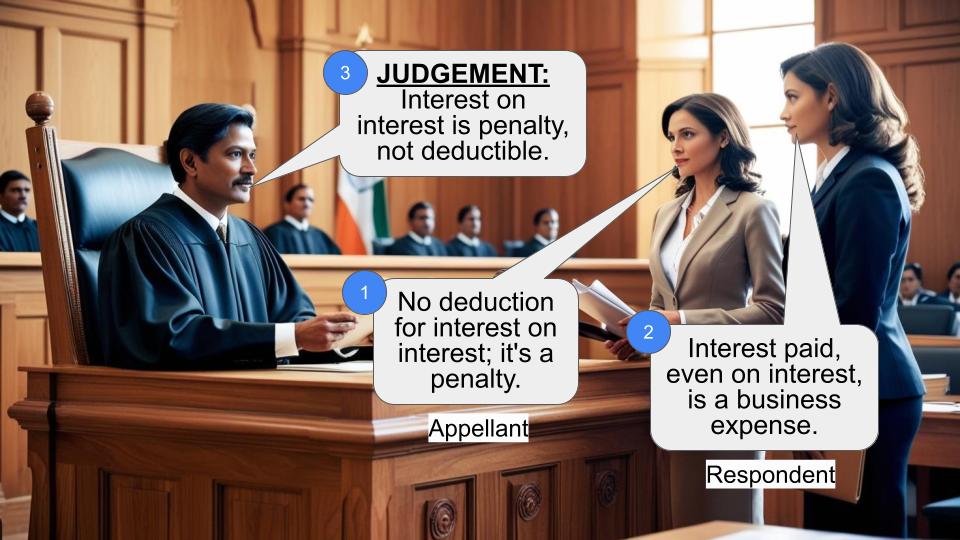

1. Revenue's Argument:

The Tribunal didn't provide sufficient reasons for allowing the assessee's appeals and the matter should be remanded for reconsideration.

2. Assessee's Argument:

The Tribunal considered all aspects in detail, including transactions with M/s. Mehta Financiers. Since interest-free funds available exceeded the balance, no disallowance of interest was necessary.

Key Legal Precedents:

1. Commissioner of Income-tax vs. Raghuvir Synthetics Ltd [2013] 354 ITR 222

2. Commissioner of Income-tax – I vs. Amod Stamping (P.) Ltd [2014] 45 taxmann.com 427 (Gujarat)

3. Commissioner of Income-Tax vs. Gujarat State Fertilizers and Chemicals Ltd [2013] 358 ITR 323 [Guj]

4. S.A. Builders Ltd. v. Commissioner of Income Tax (Appeals) 288 ITR 1 (SC)

5. CIT vs. Dalmia Cement (Bhart) Ltd. (2002) 254 ITR 377

Judgement:

1. The High Court dismissed the revenue's appeals, affirming the Tribunal's decision.

2. The court agreed that interest-free funds were available to the assessee, justifying the deletion of interest disallowance made by the Assessing Officer under section 36(1)(iii) (of Income Tax Act, 1961).

3. The court confirmed that if total interest-free advances (including partners' debit balances) don't exceed total interest-free funds available, no interest is disallowable for non-business use of funds.

FAQs:

Q1: What is the significance of "commercial expediency" in this case?

A1: Commercial expediency is a key factor in determining whether interest on borrowed funds should be allowed as a deduction, even if the funds were lent interest-free to a sister concern.

Q2: How does the availability of interest-free funds affect the disallowance of interest?

A2: If the total interest-free advances don't exceed the total interest-free funds available, no interest is disallowable for non-business use of funds.

Q3: What principle did the court affirm regarding investments and interest-free funds?

A3: The court affirmed that investments are presumed to be made from interest-free funds if such funds are sufficient to cover the investments.

Q4: Can the Income Tax Authorities decide what constitutes reasonable expenditure for a business?

A4: No, the court emphasized that Income Tax Authorities should not put themselves in the position of the businessman or board of directors to decide what is reasonable expenditure.

Q5: What is the relevance of the S.A. Builders Ltd. case in this judgment?

A5: The S.A. Builders Ltd. case established that the key test for allowing interest on borrowed funds is whether the lending was done as a measure of commercial expediency, even if it was to a sister concern at no interest.

1. Being aggrieved and dissatisfied with the impugned judgment and order passed by the Income Tax Appellate Tribunal, Ahmedabad Bench (hereinafter referred to as ‘the Tribunal’), the revenue has preferred the present Tax Appeals assailing the following orders

1.1 These appeals were admitted by this Court on 11.10.2006 for consideration of the following substantial question of law:

“Whether the Appellate Tribunal is right in law and on

facts in holding that interest free funds were available

with the assessee and thereby deleting the disallowance

of interest made by the Assessing Officer u/s. 36(1)(iii) (of Income Tax Act, 1961)

of the Act?”

2. The assessees filed their return of income for the

respective assessment years in question. During the course of

assessment proceedings the Assessing Officer made

disallowances/addition with regard to interest amount and

stamp charges.

2.1 Being aggrieved by the same, the assessee filed appeal

before CIT(A). The CIT(A) partly allowed the appeals. The

assessee as well as revenue therefore preferred appeals

before the Tribunal. The Tribunal deleted the disallowance of

interest amount which is being challenged by the revenue in

the present set of appeals.

3. Mr. Varun Patel, learned advocate appearing for the

revenue contended that the Tribunal has not assigned any

reasons for allowing the appeals filed by the assessee and

therefore the appeals may be remanded to the Tribunal for

reconsideration of the matters and decision afresh with

cogent and convincing reasons.

4. Mr. B.S. Soparkar, learned advocate appearing for the

respondents supported the impugned order passed by the

Tribunal and submitted that the Tribunal has not committed

any error in passing the same. He has drawn our attention to

paragraphs no. 31.1, 3.2, 3.4 & 3.5 of the impugned order and

contended that the Tribunal has considered each and every

aspect of each of the matters in detail and the transactions

carried out between M/s. Mehta Financiers. He submitted

that since the interest free funds available with the assessees

were much more than the balance no disallowance of interest

was called for.

3.1 In support of his submissions, Mr. Soparkar has relied

upon the decision of this Court in the case of Commissioner

of Income-tax vs. Raghuvir Synthetics Ltd reported in

[2013] 354 ITR 222 and in the case of Commissioner of

Income-tax – I vs. Amod Stamping (P.) Ltd reported in

[2014] 45 taxmann.com 427 (Gujarat).

5. We have heard learned advocates for the parties and

gone through the records of the case. At the outset we think

it appropriate to have a look at section 36(1)(iii) (of Income Tax Act, 1961)

and the same is reproduced hereunder:

"(iii) the amount of the interest paid in respect of

capital borrowed for the purposes of the business

or profession. Explanation.- Recurring

subscriptions paid periodically by shareholders, or

subscribers in Mutual Benefit Societies which fulfil

such conditions as may be prescribed, shall be

deemed to be capital borrowed within the meaning

of this clause; “

5.1 An identical issue had come up before this Court in the

case of Amod Stamping (supra) and this Court has observed

as under:

“[3.2] Similar observations are made by the learned

ITAT with respect to the assessment years 2005-06

and 2006-07. In the case of Reliance Utilities and

Power Ltd. (Supra), the Bombay High Court has

held that if there are funds available both interest-

free and overdraft and/or loans taken, then a

presumption would arise that investments would be

out of the interest-free funds generated or

available with the company, if the interest-free

funds were sufficient to meet the investments and

therefore, interest was deductible. Similar view has

been taken by the Division Bench of this Court in

the case of Commissioner of Income-Tax vs.

Gujarat State Fertilizers and Chemicals Ltd.

reported in [2013] 358 ITR 323 [Guj]. Applying

the ratio/law laid down by the Bombay High Court

in the case of Reliance Utilities and Power Ltd.

(Supra) as well as Division Bench of this Court in

the case of Gujarat State Fertilizers and Chemicals

Ltd. (Supra) to the facts of the case on hand and

when it has been found that the assessee was

having interest-free funds far in excess of

investments and therefore, it can be said that the

investments are made out of interest-free funds

and therefore, the AO was not justified in making

additions and/or making disallowance under

section 36(1)(iii) (of Income Tax Act, 1961). Under the

circumstances, no error and/or illegality has been

committed by the learned ITAT in deleting the

disallowance made by the AO under section 36(1) (of Income Tax Act, 1961)

(iii) of the IT Act. No question of law much less

substantial question of law arise with respect to

deletion of the disallowance made by the AO under

section 36(1)(iii) (of Income Tax Act, 1961). “

5.2 Similarly in the case of Raghuvir Synthetics Ltd (supra),

this Court has held as under:

“9. We may refer to the judgment of Apex Court

at this stage given in case of S.A.Builders Ltd. v.

Commissioner of Income Tax (Appeals)

reported in 288 ITR 1 (SC) where the question was

whether interest on funds borrowed by the

assessee to give an interest free loan to sister

concern should be allowed as deduction and the

Apex Court ruled thus :

“We have considered the submission of the

respective parties. The question involved in

this case is only about the allowability of the

interest on borrowed funds and hence we are

dealing only with that question. In our

opinion, the approach of the High Court as

well as the authorities below on the aforesaid

question was not correct.

In our opinion, the High Court in the

impugned judgment, as well as the Tribunal

and the Income Tax Authorities have

approached the matter from an erroneous

angle. In the present case, the assessee

borrowed the fund from the bank and lent

some of it to its sister concern (a subsidiary)

on interest free loan. The test, in our opinion,

in such a case is really whether this was done

as a measure of commercial expediency.

The expression "commercial expediency" is an

expression of wide import and includes such

expenditure as a prudent businessman incurs

for the purpose of business. The expenditure

may not have been incurred under any legal

obligation, but yet it is allowable as a

business expenditure if it was incurred on

grounds of commercial expediency.

We agree with the view taken by the Delhi

High Court in CIT vs. Dalmia Cement (Bhart)

Ltd. (2002) 254 ITR 377, that once it is

established that there was nexus between the

expenditure and the purpose of the business

(which need not necessarily be the business

of the assessee itself), the Revenue cannot

justifiably claim to put itself in the arm-chair

of the businessman or in the position of the

board of directors and assume the role to

decide how much is reasonable expenditure

having regard to the circumstances of the

case. No businessman can be compelled to

maximize its profit. The Income Tax

Authorities must put themselves in the shoes

of the assessee and see how a prudent

businessman would act. The authorities must

not look at the matter from their own

viewpoint but that of a prudent businessman.

As already stated above, we have to see the

transfer of the borrowed funds to a sister

concern from the point of view of commercial

expediency and not from the point of view

whether the amount was advanced for

earning profits.”

10. Accordingly, the question is answered in

favour of the assessee by the Apex Court. In this

Tax Appeal it is to be specified here that

considering the material on record and keeping in

view substantial interest free funds and business

expediency that the CIT(A) and Tribunal held the

issue in favour of assessee.

6. The question raised in the present appeals is squarely

governed by these two abovementioned decisions. In view of

the above, we are of the opinion that the Tribunal was

justified in holding that interest free funds were available with

the assessee and thereby deleting the disallowance of interest

made by the Assessing Officer u/s. 36(1)(iii) (of Income Tax Act, 1961). The

Tribunal has rightly considered that the assessees have

clearly demonstrated that it had interest free funds available

and the balance amount of interest free advances after

reducing the advance of M/s. Mehta Financiers was given for

purchase of shares. The Tribunal proceeded on the footing

that if total interest-free advances including debit balances of

partners do not exceed the total interest-free funds available

with the assessee, no interest is disallowable on account of

utilisation of fund for non-business purposes and if it exceeds,

the proportionate disallowance can be made. We are in

complete agreement with the findings of fact arrived at by the

Tribunal.

7. In the premises aforesaid, we answer the question raised

in the present appeals in the affirmative i.e. in favour of

assessee and against the revenue. We hold that the Tribunal

was justified in holding that the interest free funds were

available with the assessee and thereby deleting the

disallowance of interest made by the Assessing Officer u/s.

36(1)(iii) of the Act. The impugned order passed by Tribunal

is confirmed. Appeals stand dismissed accordingly.

(K.S.JHAVERI, J.)

(K.J.THAKER, J)

×

Similar Ripples

Questions

Court Upholds Tribunal's Decision on Interest-Free Funds Availability

Write your CommentSimilar Posts

Generic

- Reportdata/4227.pdf