Court Upholds Tribunal's Decision on Taxing Only Gross Profit of Unaccounted Sa…

Full News

Court Upholds Tribunal's Decision on Taxing Only Gross Profit of Unaccounted Sales

Court Upholds Tribunal's Decision on Taxing Only Gross Profit of Unaccounted Sales

This case involves a dispute between the Commissioner of Income Tax and Gurubachhan Singh J. Juneja regarding the taxation of alleged unaccounted sales. The Income Tax Appellate Tribunal had ruled that only the gross profit on the unaccounted sales could be taxed, not the entire amount. The High Court upheld this decision, agreeing that in the absence of evidence showing unexplained investments, only the gross profit should be subject to tax.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Gurubachhan Singh J. Juneja (High Court of Gujarat)

Income Tax Reference No.109 of 1996

Date: 12th February 2008

Key Takeaways:

1. The court emphasized the importance of concrete evidence in tax cases.

2. Mere allegations of unaccounted sales are not sufficient for full taxation.

3. In the absence of proof of unexplained investments, only the gross profit on unaccounted sales can be taxed.

4. The judgment highlights the need for tax authorities to provide substantial evidence to support their claims.

Issue:

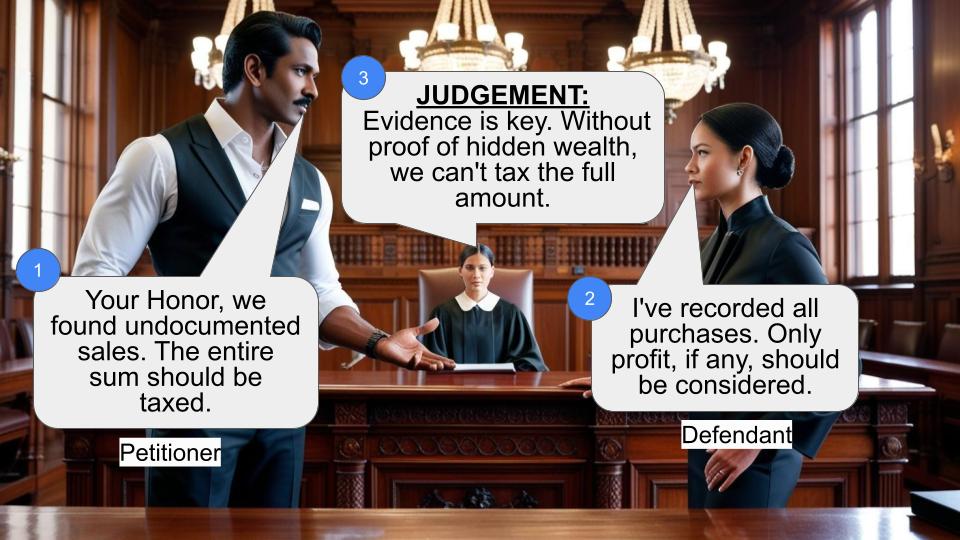

Whether the Income Tax Appellate Tribunal was correct in law and on facts in deleting the addition of Rs.10,85,003/- made on account of unaccounted cash sales?

Facts:

1. The case pertains to the Assessment Year 1984-85, with the relevant accounting period ending on June 30, 1983.

2. The assessee, Gurubachhan Singh J. Juneja, was engaged in the business of trading in tyres under the name "M/s. Punjab Tyres".

3. Search proceedings under Section 132 (of Income Tax Act, 1961) were carried out on September 6 and 7, 1984, at the assessee's residential and business premises.

4. Various books of accounts and documents were seized during the search.

5. Loose sheets (Annexures "C/4 to C/15") were found, reflecting sales made from July 15, 1983, to the end of June 1984.

6. The Income Tax Officer found that sales amounting to Rs. 10,85,003/- were not recorded in the books of accounts of either M/s. Punjab Tyres or M/s. Paul Tyres (a related concern).

7. The Income Tax Officer added the entire amount of Rs.10,85,003/- to the assessee's income.

Arguments:

1. The Revenue (Income Tax Department) argued that the entire amount of unaccounted sales (Rs.10,85,003/-) should be added to the assessee's taxable income.

2. The assessee contended that the addition was not justified and that only the gross profit on the unaccounted sales, if any, should be considered for taxation.

3. The assessee argued that all purchases were from reputed companies and fully vouched for, implying that there was no unexplained investment.

Key Legal Precedents:

The judgment doesn't explicitly mention any specific legal precedents. However, it refers to the Income Tax Act, 1961, particularly Section 256(1) (of Income Tax Act, 1961) under which the question was referred to the High Court.

Judgment:

1. The High Court upheld the Tribunal's decision to delete the addition of Rs.10,85,003/- made on account of unaccounted cash sales.

2. The court agreed that only the gross profit on the said amount could be brought to tax.

3. The basis for this decision was the lack of evidence showing any unexplained investment made by the assessee that was reflected in the alleged unaccounted sales.

4. The court answered the referred question in the affirmative, favoring the assessee and against the Revenue.

FAQs:

Q1: What was the main issue in this case?

A1: The main issue was whether the entire amount of alleged unaccounted sales should be taxed or only the gross profit on those sales.

Q2: Why did the court rule in favor of the assessee?

A2: The court ruled in favor of the assessee because there was no evidence of unexplained investments corresponding to the alleged unaccounted sales.

Q3: What is the significance of this judgment for taxpayers?

A3: This judgment emphasizes that tax authorities need to provide concrete evidence of unexplained investments or income before making additions to taxable income.

Q4: Does this mean that unaccounted sales are not taxable?

A4: No, the judgment doesn't exempt unaccounted sales from taxation. It states that in the absence of proof of unexplained investments, only the gross profit on such sales can be taxed.

Q5: What lesson can tax authorities learn from this case?

A5: Tax authorities should ensure they have substantial evidence of unexplained investments or income before making additions to a taxpayer's income, rather than relying on mere allegations or assumptions.

1. Income-Tax Appellate Tribunal, Ahmedabad Bench “C” has referred the following question for the opinion of this Court under Section 256(1) (of Income Tax Act, 1961) (“the Act”) at the instance of the Commissioner of Income-tax.

“Whether, the Appellate Tribunal is right in law and on facts in deleting the addition of Rs.10,85,003/- made on account of unaccounted cash sales ?”

2. The Assessment Year is 1984-85. The relevant accounting period being year ended on 30th June, 1983. The assessee, an individual, is engaged in business of trading in Tyres under the name and style of “M/s. Punjab Tyres”. Search proceedings under Section 132 (of Income Tax Act, 1961) were carried out on 6th and 7th September, 1984 at the residential and business premises of the assessee. In the course of search, various Books of Accounts and documents were seized. Annexures “C/4 to C/15” were some of the loose sheets which were seized during the course of Section 132 (of Income Tax Act, 1961) proceedings and the said sheets reflected sales made on various dates for the period from 15.7.1983 upto the end of June, 1984. The sales so recorded were effected by M/s. Punjab Tyres as well as M/s. Paul Tyres (a proprietary concern of one Shri Jitendra Pal Singh, son of the assessee). The loose sheets were examined and tallied by the Inspector of the Department and it was found that for the period up to 31st March, 1984 sales to the extent of Rs.10,85,003/- were not found in the Books of Accounts of either Concern. After issuing Show Cause Notice and considering the reply filed by the assessee, the Income-tax Officer did not agree with the assessee's explanation and made addition of Rs.10,85,003/-, being the value of unaccounted sales by observing as under :

“There assessee's explanation as regards the difference of sales not recorded in the books of accounts is not convincing because for each sale entry in the loose sheets there must be corresponding entry in the regular books of accounts. Besides each sale which are found in the cash book might not have been entered in the loose sheets and have been directly recorded in the books of accounts. In the circumstances it is not possible to give any relief for unaccounted cash sales found. The entry in the unaccounted sales of Rs.10,85,003/- are included in the total income of the assessee.”

3. The assessee carried the matter in Appeal before the Commissioner (Appeals), who, vide order dated 26th August, 1987, partly allowed the Appeal by holding as under :

“The ITO's finding that the sales in the regular books of accounts might not have been entered in the loose sheets is based only on surmises. The ITO's presumption of ticked or unticked as well as rounded or unrounded sales transaction has no valid and tenable basis. In this background, I am inclined to accept the contention of the appellant to a major extent. The addition made is deleted but I sustain the G.P., addition on difference of sales of Rs.2,43,339/-”

4. The Revenue, being aggrieved with the order of Commissioner (Appeals) carried the matter before the Tribunal. At the time of hearing there was difference of opinion between the two Members of the Tribunal. Ultimately, the matter was referred to 3rd Member of the Tribunal, who agreed with the view adopted by the Accountant Member. The Tribunal held that the assessee could not be taxed on the entire amount of Rs.10,85,003/-, but, was liable to be taxed only on the gross profit earned on the said sales. The basis of this finding is the fact that all the purchases are from reputed companies and/or their dealers and such purchases are fully vouched.

5. Heard Mr. B.B.Naik, learned Standing Counsel for the applicant – Revenue and Mr. M.J.Shah, learned Advocate for the respondent – assessee. Mr. Naik has not been able to dislodge the findings recorded by the Tribunal that the Revenue had not proved, by bringing any material on record, that the assessee had made any investment to make the alleged unaccounted sales.

6. Hence, in absence of any material on record to show that there was any unexplained investment made by the assessee which was reflected by the alleged unaccounted sales the finding of the Tribunal that only the gross profit on the said amount can be brought to tax does not call for any interference. The Tribunal was, therefore, justified in deleting the addition of Rs.10,85,003/- made on account of unaccounted cash sales.

7. The question referred for the opinion is, therefore, answered in the affirmative i.e. in favour of the assessee and against the Revenue.

8. Reference stands disposed of accordingly. There shall be no order as to costs.

(D.A.MEHTA, J.)

(Z.K.SAIYED,J.)

×

Similar Ripples

Questions

Court Upholds Tribunal's Decision on Taxing Only Gross Profit of Unaccounted Sales

Write your CommentSimilar Posts

Generic

- Reportdata/4826.pdf