Full News

Court Upholds Tribunal's Decision to Remand Case for Fresh Assessment

Court Upholds Tribunal's Decision to Remand Case for Fresh Assessment

This case involves an appeal by the Principal Commissioner of Income Tax against an order of the Income Tax Appellate Tribunal. The Tribunal had remanded a matter back to the Assessing Officer for a fresh decision regarding certain issues in the Assessment Year 2007-08. The High Court dismissed the appeal, upholding the Tribunal's decision to remand the case.

Get the full picture - access the original judgement of the court order here

Case Name:

Principal Commissioner of Income Tax Vs Aggarwal Sales (High Court of Punjab & Haryana)

ITA No.316 of 2016 (O&M)

Date: 10th November 2016

Key Takeaways

1. The court affirmed that when findings in an order are not conclusive and observations are merely prima facie, remanding the matter to the Assessing Officer is appropriate.

2. The Assessing Officer retains the liberty to make additions if warranted after considering all facts and circumstances.

3. References to specific case laws in a remand order are illustrative, not restrictive.

Issue

Was the Income Tax Appellate Tribunal justified in remanding the matter to the Assessing Officer for a fresh decision, and were the directions given by the Tribunal appropriate?

Facts

1. The case pertains to the Assessment Year 2007-08.

2. During a search of the assessee's premises, a document with handwritten notings was found.

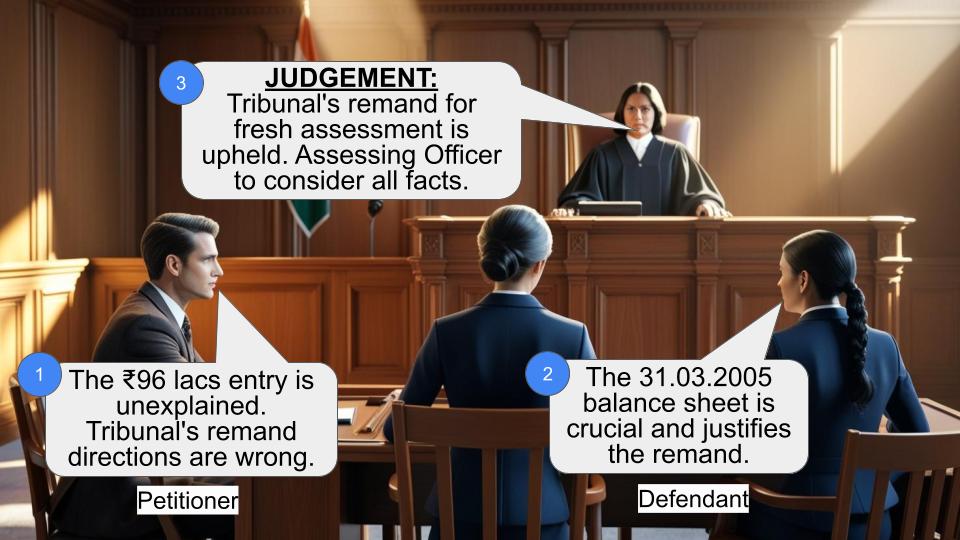

3. The appellant (Principal Commissioner of Income Tax) contended that an entry of ₹96 lacs remained unexplained and was rightly added to the assessee's income.

4. The CIT(Appeals) upheld the assessment order.

5. The Tribunal found that certain other documents, especially a balance sheet dated 31.03.2005, should be considered before making a decision.

6. The Tribunal remanded the matter to the Assessing Officer for a fresh order, considering the additional evidence.

Arguments

Appellant (Principal Commissioner of Income Tax):

- The entry of ₹96 lacs was unexplained and correctly added to the assessee's income.

- The directions issued by the Tribunal to the Assessing Officer were inappropriate.

Respondent (Aggarwal Sales):

- The balance sheet from 31.03.2005 should be considered as additional evidence.

- The Tribunal's decision to remand the matter for fresh assessment was appropriate.

Key Legal Precedents

1. CIT versus Ravi Kumar, 294 ITR 78: This case was mentioned in the Tribunal's order as an illustrative example for the Assessing Officer to consider. The court clarified that this reference was not restrictive and the Assessing Officer should consider all relevant provisions and authorities.

Judgement

1. The High Court dismissed the appeal, upholding the Tribunal's decision to remand the matter.

2. The court found no grounds for interfering with the Tribunal's discretion in remanding the matter.

3. The court clarified that the Tribunal's observations were prima facie and not conclusive.

4. The Assessing Officer was directed to decide the issue afresh, considering all relevant facts, circumstances, and legal provisions.

FAQs

Q1: Why did the court dismiss the appeal?

A: The court found no reason to interfere with the Tribunal's discretion in remanding the matter. It agreed that the balance sheet from 31.03.2005 was a relevant consideration that should be taken into account.

Q2: Does the remand order restrict the Assessing Officer's decision-making?

A: No, the court clarified that the Assessing Officer retains the liberty to make additions if warranted after considering all facts and circumstances. The reference to the Ravi Kumar case was illustrative, not restrictive.

Q3: What is the significance of the court's statement about "prima facie" observations?

A: The court emphasized that the Tribunal's observations were not conclusive but preliminary. This means the Assessing Officer should conduct a fresh, thorough examination of the evidence without being bound by these initial observations.

Q4: How does this judgment impact similar cases?

A: This judgment reinforces the principle that when findings are not conclusive and observations are merely prima facie, remanding a matter for fresh assessment is appropriate. It also emphasizes the importance of considering all relevant evidence before making a final decision in tax assessment cases.

Q5: What should the Assessing Officer do now?

A: The Assessing Officer should reconsider the case, taking into account all relevant evidence, including the balance sheet from 31.03.2005. They should also consider the Ravi Kumar case along with other relevant legal provisions and authorities before making a fresh decision.

1. This is an appeal against the order of the Income Tax Appellate Tribunal remanding the matter to the Assessing Officer to decide some of issues afresh in respect of the Assessment Year 2007-08.

2. At a search conducted in the assessee's premises a document was found which contained certain notings in hand. The appellant contends that one of the entries therein in the sum of `96 lacs remained to be explained and that the amount was therefore, rightly added to the assessee'sincome. The CIT(Appeals) upheld the assessment order. The Tribunal,however, found that certain other documents especially a balance-sheet of 31.03.2005 ought to be considered and a fresh order ought to be passed thereafter. The Tribunal noted that the balance-sheet was already a part of the record of the revenue as it pertained to the earlier assessment year.

3. There is no ground for interfering with the discretion exercised by the Tribunal in remanding the matter. The impugned order rightly notes that the balance-sheet would be a relevant consideration and therefore, ought taken into account while considering the assessee's explanation for the said entry.

4. The appellant, however, is aggrieved by the directions issued by the Tribunal to the Assessing Officer. The apprehension is not well- founded.

5. The Tribunal has merely directed the Assessing Officer to decide the issue afresh in the light of the additional evidence. The findings in the order are not conclusive. The observations are merely prima facie. If they were conclusive there would have been no question of remanding the matter. Even the finding that the assessee had prima facie explained the addition made by the Assessing Officer is precisely that prima facie. If upon a consideration of all other facts and circumstances, the Assessing Officer finds that the addition ought to be made, he is always at liberty to do so.

6. The grievance that the order directs the Assessing Officer to follow only the judgment of this Court in CIT versus Ravi Kumar, 294 ITR 78 is also not well-founded. The impugned order does not restrict the Assessing Officer to a consideration only of Ravi Kumar's case. The reference to Ravi Kumar's case is only illustrative. The Assessing Officer while deciding the issue afresh would have to consider the same in accordance with law after taking into consideration Ravi Kumar's case as well as any other relevant provisions of law and authorities.

7. The petition is accordingly dismissed.

(S.J. VAZIFDAR)

CHIEF JUSTICE

(DEEPAK SIBAL)

JUDGE

November 10, 2016

×