Deduction Under Section 80HHC (of Income Tax Act, 1961) Allowed Only After Adju…

Full News

Deduction Under Section 80HHC (of Income Tax Act, 1961) Allowed Only After Adjusting Losses and Depreciation

Deduction Under Section 80HHC (of Income Tax Act, 1961) Allowed Only After Adjusting Losses and Depreciation

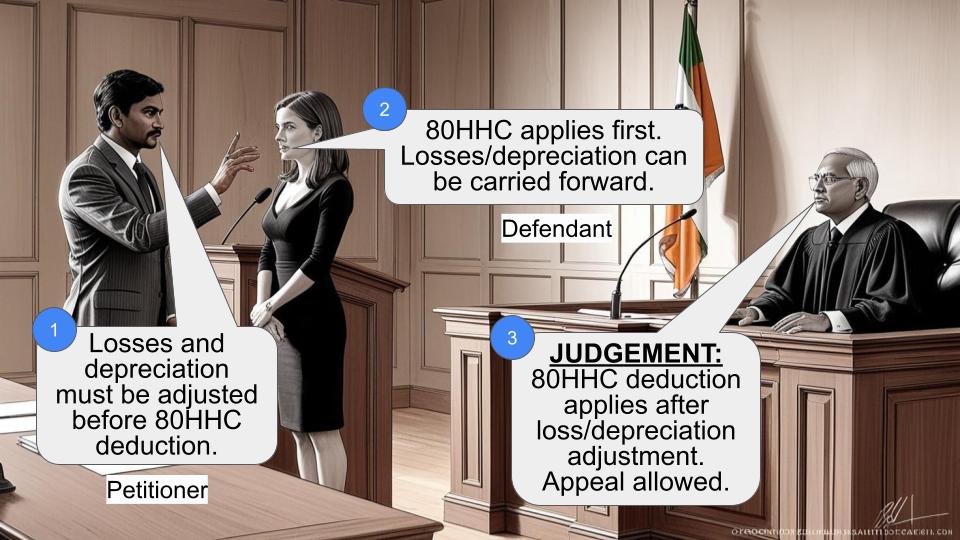

This case involves a dispute between the Commissioner of Income Tax and Exportos Apparel Group Ltd. regarding the interpretation of Section 80HHC (of Income Tax Act, 1961). The main issue was whether deductions under this section should be allowed before or after adjusting unabsorbed business losses and depreciation. The High Court ruled in favor of the Revenue, stating that deductions under Section 80HHC (of Income Tax Act, 1961) should be allowed only after adjusting these losses and depreciation.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Exports Apparel Group Ltd. (High Court of Delhi)

ITA No. 67/2005

Date: 15th November 2007

Key Takeaways:

1. Deductions under Section 80HHC (of Income Tax Act, 1961) must be calculated after adjusting unabsorbed business losses and depreciation.

2. The court's interpretation aligns with the Supreme Court's decision in the Kotagiri Industrial Co-operative Tea Factory Ltd. case.

3. This ruling clarifies the proper sequence for calculating total income under the Income Tax Act.

Issue:

Was the Income Tax Appellate Tribunal correct in holding that the assessee is entitled to a deduction under Section 80HHC (of Income Tax Act, 1961) before adjusting unabsorbed business loss and unabsorbed depreciation?

Facts:

1. The case pertains to the assessment year 1998-99.

2. The assessee, Exportos Apparel Group Ltd., claimed a deduction under Section 80HHC (of Income Tax Act, 1961) before allowing for unabsorbed business losses and unabsorbed depreciation.

3. The assessee argued that these losses and depreciation should be carried forward.

4. The Income Tax Appellate Tribunal had ruled in favor of the assessee.

Arguments:

Assessee's Argument:

- The deduction under Section 80HHC (of Income Tax Act, 1961) should be allowed before adjusting unabsorbed business losses and depreciation.

- They relied on the Andhra Pradesh High Court decision in CIT vs. Gogineni Tobacco Ltd.

Revenue's Argument:

- The gross total income should be computed first, including adjustments for losses and depreciation, before allowing deductions under Chapter VI-A.

- They cited Sections 80A and 80B(5) of the Income Tax Act to support their position.

Key Legal Precedents:

1. CIT vs. Kotagiri Industrial Co-operative Tea Factory Ltd. (1997) 139 CTR (SC) 359 : (1997) 224 ITR 604 (SC) - The Supreme Court held that gross total income must be determined by setting off business losses of earlier years before allowing deductions under Section 80P (of Income Tax Act, 1961).

2. CIT vs. Gogineni Tobacco Ltd. (2000) 158 CTR (AP) 119 : (1999) 238 ITR 970 (AP) - This Andhra Pradesh High Court decision supported the assessee's position but was ultimately not followed by the High Court in this case.

Judgement:

The High Court ruled in favor of the Revenue, stating that:

1. The Tribunal was incorrect in its interpretation of Section 80HHC (of Income Tax Act, 1961).

2. Deductions under Section 80HHC (of Income Tax Act, 1961) should be allowed only after adjusting unabsorbed business losses and unabsorbed depreciation.

3. The court's decision aligns with the Supreme Court's ruling in the Kotagiri Industrial Co-operative Tea Factory Ltd. case.

4. The Andhra Pradesh High Court's decision in Gogineni Tobacco Ltd. was not followed as it conflicted with the Supreme Court's view.

FAQs:

1. Q: What is Section 80HHC (of Income Tax Act, 1961)?

A: Section 80HHC (of Income Tax Act, 1961) deals with deductions in respect of profits related to export business.

2. Q: How should the gross total income be calculated according to this judgment?

A: The gross total income should be calculated first, including adjustments for unabsorbed losses and depreciation, before applying deductions under Chapter VI-A.

3. Q: Why did the court not follow the Andhra Pradesh High Court's decision in the Gogineni Tobacco Ltd. case?

A: The court found that the Gogineni Tobacco Ltd. decision conflicted with the Supreme Court's ruling in the Kotagiri Industrial Co-operative Tea Factory Ltd. case, which is binding on all courts.

4. Q: What sections of the Income Tax Act were crucial in this judgment?

A: Sections 80A, 80B(5), and 80HHC were key to the court's interpretation and decision.

5. Q: How does this judgment affect businesses claiming deductions under Section 80HHC (of Income Tax Act, 1961)?

A: Businesses will need to adjust their unabsorbed losses and depreciation before claiming deductions under Section 80HHC (of Income Tax Act, 1961), potentially reducing the amount of deduction they can claim.

1. Admit.

2. The following question of law is framed for consideration :

"Whether the Income-tax Appellate Tribunal (‘Tribunal’) was correct in law in holding that the assessee is entitled to a deduction under s. 80HHC of the IT Act, 1961 before adjusting unabsorbed business loss and unabsorbed depreciation ?"

3. Learned counsel for the Revenue has drawn our attention to s. 80A of the IT Act, 1961 (for short ‘Act’). This section occurs in Chapter VI-A of the Act and the relevant portion is sub-s. (1) which reads as follows :

"80A—Deductions to be made in computing total income— (1) In computing the total income of an assessee, there shall be allowed from his gross total income, in accordance with and subject to the provisions of this chapter, the deductions specified in ss. 80C to 80U."

4. A plain and simple reading of the above shows that for computing the total income of an assessee, first the gross total income of the assessee is to be computed in accordance with the provisions of Chapter VI-A of the Act.

5. Sec. 80B(5) (of Income Tax Act, 1961) defines gross total income in the following words :

"80B.—Definitions —In this chapter— (1) to (4) ............. (5) "gross total income" means the total income computed in accordance with the provisions of this Act, before making any deduction under this chapter.

6. A plain reading of s. 80B(5) of the Act shows that first the gross total income has to be computed and thereafter deductions, if any, under Chapter VI-A of the Act, may be made.

7. It follows, therefore, that on a combined reading of s. 80A and s. 80B(5) of the Act, the gross total income of an assessee is to be first calculated; thereafter any deductions that the assessee may be entitled to under Chapter VI-A of the Act have to be granted to him. The net income of the assessee will be its total income.

8. Sec. 80HHC (of Income Tax Act, 1961), with which we are concerned, occurs in Chapter VI-A of the Act and deals with deductions in respect of profits related with exports business.

9. Sec. 80HHC(1) (of Income Tax Act, 1961) reads as follows :

"80HHC .—Deduction in respect of profits retained for export business. (1) Where an assessee, being an Indian company or a person (other than a company) resident in India, is engaged in the business of export out of India of any goods or merchandise to which this section applies, there shall, in accordance with and subject to the provisions of this section, be allowed, in computing the total income of the assessee, a deduction to the extent of profits, referred to in sub-s. (1B), derived by the assessee from the export of such goods or merchandise : ........................"

10. From a reading of s. 80HHC(1) of the Act, it appears that for computing the total income of the assessee, a deduction to the extent of profits referred to in sub-s. (1B) may be granted to the assessee. The expression "total income" occurring in s. 80HHC(1) obviously has reference to s. 80A of the Act and, as we have explained earlier, that has to be read in conjunction with s. 80B(5) of the Act. Consequently, for obtaining any benefit under s. 80HHC(1) of the Act, the gross total income of the assessee has to be computed and thereafter the assessee will get an adjustment of a deduction under s. 80HHC(1) of the Act for the purpose of calculating the total income.

11. A similar issue of interpretation had arisen in CIT vs. Kotagiri Industrial Co-operative Tea Factory Ltd. (1997) 139 CTR (SC) 359 : (1997) 224 ITR 604 (SC) in the context of s. 80P of the Act which also is a part of Chapter VI-A of the Act. In that case, the Supreme Court reversed the decision of the High Court and held that in view of s. 80B(5) of the Act it is necessary for the purpose of making a deduction under s. 80P of the Act to determine the gross total income in accordance with other provisions of the Act. In other words, the gross total income must be determined by setting off against the income the business losses of the earlier years as required under s. 72 of the Act, before allowing deduction under s. 80P thereof.

12. Insofar as the facts of the present case are concerned, for the asst. yr. 1998-99, the assessee had claimed a deduction under s. 80HHC before allowing unabsorbed business losses and unabsorbed depreciation. According to the assessee, this business loss and depreciation ought to have been allowed to be carried forward. The assessee relied upon the decision of the Andhra Pradesh High Court in CIT vs. Gogineni Tobacco Ltd. (2000) 158 CTR (AP) 119 : (1999) 238 ITR 970 (AP)

13. We have gone through the decision of the Andhra Pradesh High Court and have noticed that it does not make a reference to Kotagiri Industrial Co- operative Tea Factory Ltd. (supra).

14. We are of the opinion that by relying upon Gogineni Tobacco Ltd. (supra), the Tribunal came to a wrong conclusion particularly since the view of the Andhra Pradesh High Court is in conflict with the view expressed by the Supreme Court.

15. There is no doubt that all of us are bound by the decision of the Supreme Court and, therefore, in view thereof, we answer the question in the negative, that is, in favour of the Revenue and against the assessee.

The appeal is accordingly allowed.

×

Similar Ripples

Questions

Deduction Under Section 80HHC (of Income Tax Act, 1961) Allowed Only After Adjusting Losses and Depreciation

Write your CommentSimilar Posts

Generic

- Reportdata/5181.pdf