High Court Dismisses Revenue's Appeal Due to Low Tax Effect

Full News

High Court Dismisses Revenue's Appeal Due to Low Tax Effect

High Court Dismisses Revenue's Appeal Due to Low Tax Effect

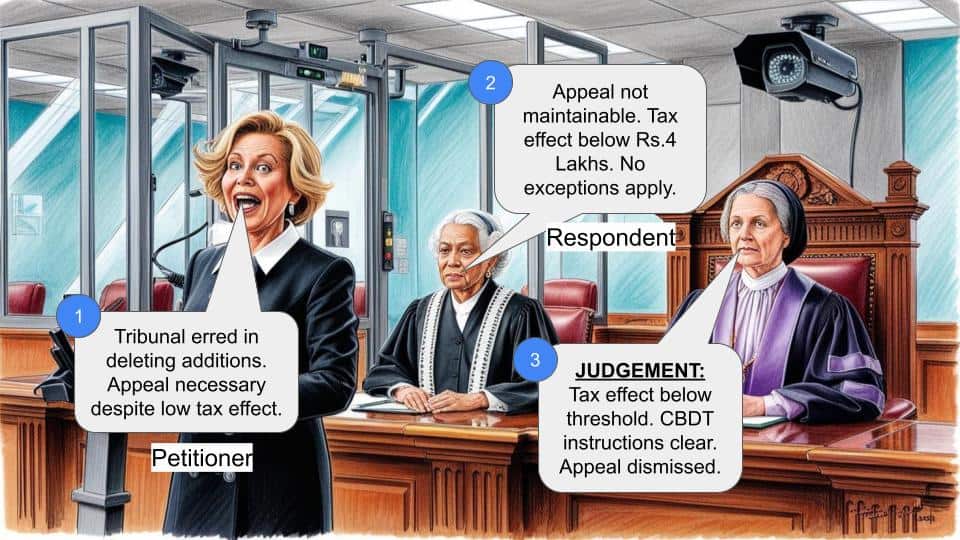

The case involves the Commissioner of Income Tax (Appellant) and Dr. C.T. Kiruba (Respondent). The Revenue challenged the Income Tax Appellate Tribunal's decision regarding tax additions for renovation and construction costs. The High Court dismissed the appeal, citing that the tax effect was below the threshold set by the Central Board of Direct Taxes (CBDT) instructions.

Get the full picture - access the original judgement of the court order here.

Case Name:

Commissioner of Income Tax vs. Dr. C.T. Kiruba (High Court of Madras)

T.C.(A).Nos.1011 and 1012 of 2007

Key Takeaways

- The High Court dismissed the Revenue's appeal because the tax effect was less than Rs.4 Lakhs.

- The case highlights the importance of adhering to CBDT instructions regarding the monetary limits for filing appeals.

- The court did not address the merits of the legal questions due to the preliminary objection on the maintainability of the appeal.

Issue

Whether the appeal by the Revenue is maintainable given that the tax effect is less than Rs.4 Lakhs, as per CBDT instructions?

Facts

- The Revenue filed appeals against the Income Tax Appellate Tribunal's order dated 27.10.2006.

- The appeals were related to the block period from 1.4.1989 to 27.10.1999.

- The Tribunal had deleted additions made by the Assessing Officer for renovation costs and construction of nurses' quarters.

- The tax effect in question was Rs. 1,90,443, which is below the Rs. 4 Lakhs threshold set by CBDT Instruction No. 2 of 2005 and Instruction No. 5 of 2007.

Arguments

- Revenue's Argument:

The Tribunal erred in deleting the additions made by the Assessing Officer.

- Assessee's Argument:

The appeal is not maintainable as the tax effect is below the Rs.4 Lakhs threshold, and the case does not fall within any exceptions specified in CBDT Instruction No. 1979.

Key Legal Precedents

- CBDT Instruction No. 2 of 2005:

Sets the monetary limit for filing appeals at Rs.4 Lakhs.

- CBDT Instruction No. 5 of 2007:

Reiterates the monetary limit and exceptions for filing appeals.

- CBDT Instruction No. 1979:

Specifies exceptions where appeals should be contested irrespective of the tax effect.

Judgement

The High Court dismissed the appeals, stating that the tax effect was less than Rs.4 Lakhs and the case did not fall within any exceptions specified by the CBDT instructions. Therefore, the appeals were not maintainable.

FAQs

Q1: Why was the appeal dismissed?

A1: The appeal was dismissed because the tax effect was less than Rs.4 Lakhs, which is below the threshold set by CBDT instructions.

Q2: What are the exceptions to the CBDT instructions?

A2: Exceptions include cases where a Revenue audit objection has been accepted, where a Board’s order or circular is the subject of an adverse order, where prosecution proceedings are contemplated, or where the constitutional validity of the Act's provisions is under challenge.

Q3: Did the court address the merits of the legal questions?

A3: No, the court did not address the merits of the legal questions due to the preliminary objection on the maintainability of the appeal.

Q4: What was the tax effect in this case?

A4: The tax effect was Rs.1,90,443, which is below the Rs.4 Lakhs threshold.

Q5: What were the additions made by the Assessing Officer?

A5: The additions were related to the cost of renovation of a residential building and the construction of nurses' quarters.

1. The Revenue has filed these appeals challenging the order of the Income Tax Appellate Tribunal 'D' Bench, Chennai, dated 27.10.2006 made in I.T.(SS) A.Nos.87/Mds/2004 and 215/Mds/2003 for the block period 1.4.1989 to 27.10.1999, and the same were admitted on the following questions of law:

“(a) Whether the Tribunal is right in deleting the addition of Rs.2.0 Lakhs made on account of renovation of residential building, including wooden work, which was admitted by the assessee himself as the cost of investment?

(b) Whether the Tribunal is right in deleting the addition ofRs.5,09,700/- made in the construction of quarters for nurses which was based on the departmental valuation report and is valid in view of the provisions of Section 142-A (of Income Tax Act, 1961)?

(c) Whether the Tribunal is right in deleting the interest charged under Section 158BFA(1) (of Income Tax Act, 1961) as the return for the block period had been filed belatedly, especially when the charging of interest is mandatory?

(d) Whether the Tribunal is right in law in not considering the sworn statement dated 27.10.1999 given by the assessee when the search under Section 132 (of Income Tax Act, 1961) had taken place?

2. Even though these appeals were admitted on the questions of law, referred supra, we are not inclined to entertain these appeals in view of the preliminary objection made by the learned counsel for the respondent that the monetary limit to prefer an appeal is pegged at Rs.4,00,000/- by the Central Board of Direct Taxes vide Instruction No.2 of 2005, dated 24.10.2005 read with Instruction No.5 of 2007, dated 16.7.2007.

3. In the case on hand, the tax liability pertains to the additions made by the Assessing Officer on account of cost of renovation and construction of nurses quarters. The preliminary objection of the assessee and the tax liability under the above heads is as under:

Preliminary objection on maintainability of Department's Tax Case Appeal:

Instruction No.2 of 2005 dated 24.10.2005 read with

Instruction No.5 of 2007 dated 16.7.2007 fixed the monetary limit to prefer a Tax Case Appeal only if the tax effect exceeds Rs.4 Lakhs. The Assessee submits that the Assessee does not fall within any of the exceptions provided in the instruction mandating the department to prefer an appeal. The total tax effect excluding interest is as follows:

4. The learned counsel for the assessee also pleaded that the case of

the assessee does not fall within the exceptions specified in Instruction No.1979 issued by the Central Board of Direct Taxes on 27.3.2000, where irrespective of revenue effect the matter should be contested by the Department. The relevant portion of the said instruction reads as under:

4. The learned counsel for the assessee also pleaded that the case of

the assessee does not fall within the exceptions specified in Instruction No.1979 issued by the Central Board of Direct Taxes on 27.3.2000, where irrespective of revenue effect the matter should be contested by the Department. The relevant portion of the said instruction reads as under:

“3. Adverse judgments relating to the following should be contested irrespective of revenue effect:

(i) Where Revenue audit objection in the case has been accepted by the Department.

(ii) Where the Board’s order, notification, instruction or circular is the subject-matter of an adverse order.

(iii) Where prosecution proceedings are contemplated against the assessee.

(iv) Where the constitutional validity of the provisions of the Act are under challenge.”

5. The learned Standing Counsel for the Revenue is not disputing the fact that the tax effect in the present case is less than Rs.4 Lakhs and that the assessee's case does not fall within the exceptions specified in Instruction No.1979, dated 27.3.2000.

6. Considering the circulars issued by the Central Board of Direct Taxes and the tax effect involved in the case on hand, this Court is not inclined to entertain these appeals. Accordingly, without going into the merits of the questions of law formulated, these appeals are dismissed as not maintainable. No costs.

(R.S.J.) (R.K.J.)

19.1.2015

Index : No

Internet : Yes To: 1. The Assistant Registrar, Income Tax Appellate Tribunal Chennai Bench "D", Chennai.

2. The Secretary, Central Board of Direct Taxes, New Delhi.

3. The Commissioner of Income Tax (Appeals) Salem.

4. The Deputy Commissioner of Income Tax Company Circle I, Salem.

R.SUDHAKAR,J.

and

R.KARUPPIAH,J.

×

Similar Ripples

Questions

High Court Dismisses Revenue's Appeal Due to Low Tax Effect

Write your CommentSimilar Posts

Generic

- Reportdata/4106.pdf