Full News

High Court Dismisses Revenue's Appeal on Profit Deduction Dispute

High Court Dismisses Revenue's Appeal on Profit Deduction Dispute

The case involves the Commissioner of Income Tax and Schmetz India P. Ltd., where the Revenue challenged the Income Tax Appellate Tribunal's decision allowing profit deductions for Schmetz India. The High Court dismissed the appeal, agreeing with the Tribunal's previous rulings.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs. Schmetz India P. Ltd. (High Court of Bombay)

Income Tax Appeal No. 1382 of 2013

Date: 24th June 2015

Key Takeaways:

- The High Court upheld the Tribunal's decision, which was consistent with a previous ruling for the same assessee.

- The court found no substantial question of law to warrant overturning the Tribunal's decision.

- The case reinforces the importance of having substantial evidence when challenging profit deductions under the Income Tax Act.

Issue

Was the Tribunal justified in allowing profit deductions for Schmetz India, despite the Revenue's claim of an extraordinary arrangement to boost profits?

Facts

- The Revenue filed an appeal under Section 260A (of Income Tax Act, 1961).

- The dispute centered around profit deductions for Schmetz India's 10A unit, which manufactures industrial sewing machine needles.

- The Revenue argued that the profits were abnormally high due to an extraordinary arrangement with a German company.

Arguments

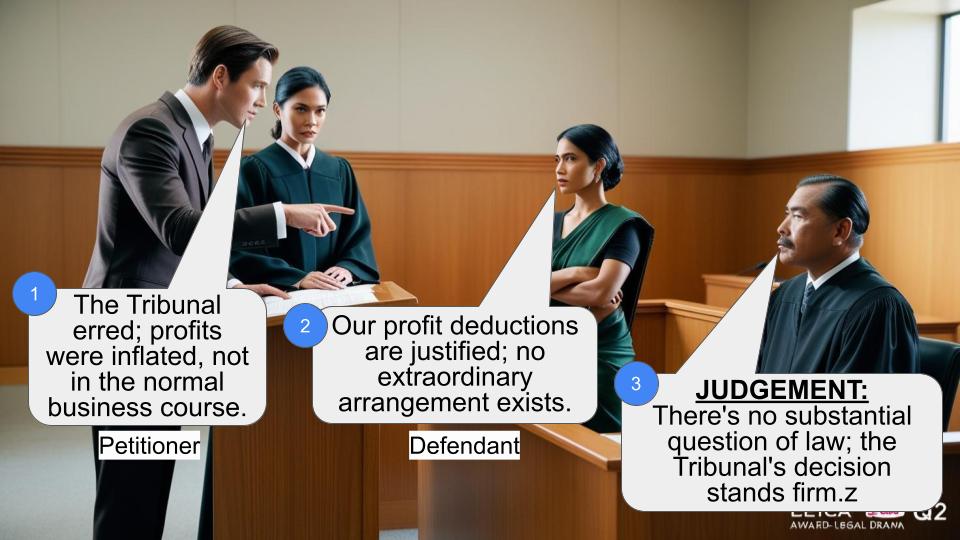

- Revenue's Argument: The Tribunal erred in allowing deductions, as the profits were not in the normal course of business and were artificially inflated.

- Schmetz India's Argument: The Tribunal's decision was based on a proper appraisal of the available material, and there was no evidence of an extraordinary arrangement.

Key Legal Precedents

- The Tribunal followed its own order for the same assessee from the previous assessment year (2004-2005).

- The High Court's decision in Appeal No. 4508 of 2010, dated September 4, 2012, was also considered, which upheld the Tribunal's earlier decision.

Judgement

The High Court dismissed the Revenue's appeal, stating that the proposed questions did not raise any substantial question of law. The court agreed with the Tribunal's assessment and found no reason to overturn its decision.

FAQs

Q1: What was the main legal question in this case?

A1: Whether the Tribunal was justified in allowing profit deductions for Schmetz India, given the Revenue's claim of an extraordinary arrangement to boost profits.

Q2: Why did the High Court dismiss the appeal?

A2: The court found no substantial question of law and agreed with the Tribunal's previous rulings, which were based on a proper appraisal of the material.

Q3: What does this decision mean for Schmetz India?

A3: Schmetz India can continue to benefit from the profit deductions as allowed by the Tribunal, as the High Court upheld the decision.

Q4: How does this case impact future tax disputes?

A4: It underscores the necessity for substantial evidence when challenging profit deductions and highlights the court's reliance on consistent legal precedents.

1. This Appeal has been filed by the Revenue under Section 260 (of Income Tax Act, 1961) A of the Income tax Act, 1961 challenging the order dated 30 November 2012 passed by the Income Tax Appellate Tribunal (the Tribunal) for the Assessment year 2005-2006.

2 Ms Bharucha, learned counsel appearing for the Revenue urges the following questions of law for our consideration.

“(a) Whether on the facts and circumstances of the case

and in law the Tribunal was justified in coming to the

conclusion that there was nothing on record to show that

the profits arrived at by the assessee in respect of the 10A

unit carrying on the business of manufacturing industrial

sewing machine needles was not in the normal course of

its business and that the abnormally high profit was due

to extraordinary arrangement between the assessee and

the German company entered into only with a view to

boost the profits of the assessee and therefore allowing

deduction of Rs.20,53,26,910/?

(b) Whether on the facts and the circumstances of the

case and in law the Tribunal was justified in holding that

there was no material available with the assessing officer

to estimate the profits of the 10A unit eligible for

deduction invoking the provisions of section 80IA(10) (of Income Tax Act, 1961)

read with section 10A(7) (of Income Tax Act, 1961) was based on proper

and reasonable appraisal of the material available on

record?”

3. The impugned order of the Tribunal has followed it's own

order in respect of the same Assessee for Assessment year 2004

2005 and the decision of this Court Appeal No.4508 of 2010

rendered on 4 September 2012 upholding the above order of the

Tribunal for Assessment year 20042005. In the circumstances, it is

an agreed position that the questions as proposed do not give rise

to any substantial question of law.

Accordingly appeal is dismissed. No order as to costs.

(N.M.Jamdar, J.) (M.S.Sanklecha, J.)

×

Similar Ripples

Questions

High Court Dismisses Revenue's Appeal on Profit Deduction Dispute

Write your CommentSimilar Posts

Generic

- Reportdata/3674.pdf