Jewelry Ownership Dispute: Court Upholds Tax Assessment on Unexplained Jewelry

Full News

Jewelry Ownership Dispute: Court Upholds Tax Assessment on Unexplained Jewelry

Jewelry Ownership Dispute: Court Upholds Tax Assessment on Unexplained Jewelry

In the case of Ajay R. Dhoot Vs Deputy Commissioner of Income Tax & Others, the court dealt with a dispute over the ownership and tax assessment of jewelry found in a locker. The jewelry was not recorded in the appellant's books, and the explanation for its acquisition was deemed unsatisfactory. The court upheld the tax assessment, treating the jewelry's value as income for the financial year it was discovered.

Get the full picture - access the original judgement of the court order here

Case Name:

Ajay R. Dhoot Vs Deputy Commissioner of Income Tax & Others (High Court of Bombay)

Income Tax Appeal No. 1127 of 2000

Date: 15th July 2015

Key Takeaways:

- Section 69A (of Income Tax Act, 1961): This section was pivotal, as it allows the value of unexplained assets to be deemed as income in the year they are discovered.

- Ownership Determination: The court determined ownership based on when the jewelry was found, not when the locker key was seized.

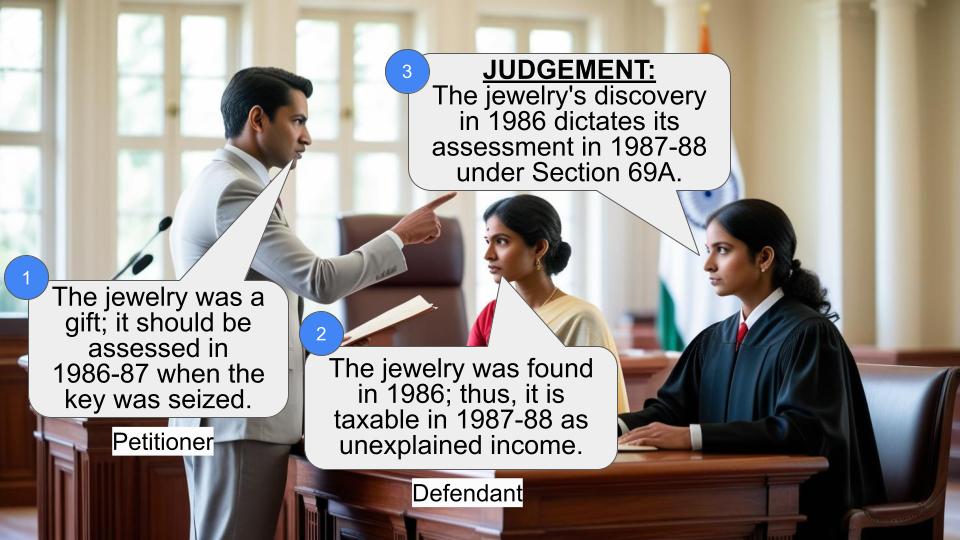

- Assessment Year: The jewelry was taxed in the year it was discovered (1987-88), not when the key was seized (1986-87).

Issue

Was the jewelry found in Mrs. Malani's locker correctly assessed as income for the financial year 1987-88 under Section 69A (of Income Tax Act, 1961)?

Facts

- On March 20, 1986, a locker key belonging to Mrs. Sujata Malani was seized during a search of the appellant's premises.

- The locker was opened on July 28, 1986, revealing jewelry valued at Rs. 2.53 lakh.

- The appellant claimed ownership of jewelry valued at Rs. 2.01 lakh, which was not recorded in his books.

- The appellant argued the jewelry should be assessed in the financial year 1986-87, when the key was seized.

Arguments

- Appellant: Argued that the jewelry should be assessed in the year the key was seized, claiming it was a gift from his aunt.

- Revenue: Contended that the jewelry was only discovered upon opening the locker, making the financial year 1987-88 the correct assessment period.

Key Legal Precedents

- Section 69A (of Income Tax Act, 1961): This section was central to the case, allowing the value of unexplained assets to be treated as income in the year they are found.

- The court referenced past cases like Patoa Brothers Vs. CIT and Harlal Mannulal Vs. CIT to support its decision, emphasizing the timing of discovery over possession.

Judgement

The court upheld the tax assessment for the financial year 1987-88, ruling that the jewelry was only discovered when the locker was opened. The appellant's explanation of the jewelry being a gift was not accepted, and the value was deemed income under Section 69A (of Income Tax Act, 1961).

FAQs

Q1: Why was the jewelry assessed in 1987-88 and not 1986-87?

A1: The jewelry was only discovered when the locker was opened in 1986, making the financial year 1987-88 the correct period for assessment.

Q2: What is Section 69A (of Income Tax Act, 1961)?

A2: It allows the value of unexplained assets to be treated as income in the year they are discovered if the owner cannot satisfactorily explain their acquisition.

Q3: Did the court accept the appellant's explanation of the jewelry being a gift?

A3: No, the court did not accept this explanation, leading to the jewelry's value being taxed as income.

1. This appeal under Section 260A (of Income Tax Act, 1961) (the 'Act') is directed against the order dated 18 April 2000 passed by the Income Tax Appellate Tribunal (the 'Tribunal'). The relevant assessment year is Assessment Year 1987-88.

2. On 5 March 2002, this appeal was admitted on the following two substantial questions of law:

“1) Whether on the facts and in the circumstances of the case and in law the Tribunal was right in law in confirming the addition of Rs.2,01,200/ under section 69A (of Income Tax Act, 1961) in the Assessment Year 1987-88 when the assessee was

not found to be owners of jewellery valued at the said amount in the financial year 198688 being the relevant previous year for the Assessment Year 1987-88 which is the requirement of section 69A (of Income Tax Act, 1961)?

2) Whether on the facts and circumstances of the case and in law the Tribunal erred in confirming the addition of Rs.2,01,100/ in the Assessment Year 198788 specially in view of the addition made in the assessee's own case for the Assessment Year 1986-87 which addition includes the alleged source of the jewellery valued at Rs.2,02,100/, thereby resulting in a double addition?”

3. The common facts necessary to answer both the above questions in this appeal are as under:

On 19 March 1986, a search action under Section 132 (of Income Tax Act, 1961)

was carried out by the revenue in respect of the appellant's

premises. During the course of the search, on 20 March 1986, a

locker key belonging to one Mrs. Sujata Malani was seized, who at

the relevant time was staying with the appellant.

4. On 28 July 1986, the locker of Mrs. Malani (the key to

which was seized on 20 March 1986) was opened by the revenue.

On opening the locker, jewellery valued in the aggregate of Rs.2.53

lakh was found therein. In the course of proceedings under Section

132(5) of the Act, the revenue on 25 November 1986 accepted the

explanation of Mrs. Malani that jewellery valued at Rs2.41 lakh out

of Rs.2.53 lakh belonged to the appellant. The appellant also

claimed to be owner of the same which was valued at the cost of

Rs.2.01 lakh.

5. On 21 March 1990, the Assessing Officer passed an order

for the Assessment Year 198788 inrespect of the appellant. In the

assessment order, it is recorded that the appellant had filed its

wealth tax return for the Assessment Year 198788 on 25 June 1987

declaring jewellery valued at Rs.2.15 lakh received as gift by him

from one Mrs. Shashikala L. Dhoot. The Assessing Officer did not

accept the appellant's explanation of source of the jewellery found

in Mrs. Malani's locker as being a gift recived from Mrs. Shashikala

L. Dhoot. Consequently, the Assessing Officer added the cost of the

jewellery which at Rs.2.01 lakh as deemed income under Section

69A of the Act.

6. In appeal, the Commissioner of Income Tax (Appeals)

(the 'CIT(A)') did not interfere with the order of the Assessing

Officer to the extent a sum of Rs.2.01 lakh which was added as

deemed income on account of unexplained jewellery owned by the

appellant.

7. On further appeal, the Tribunal by the impugned order

dismissed the appellant's appeal. In particular it did not accept the

appellant's contention that as the locker key belonging to Mrs.

Malani has been seized on 20 March 1986, the addition of deemed

income under Section 69A (of Income Tax Act, 1961) to be made on account of

jewellery found on opening of the locker on 28 July 1986 can only

be in the Assessment Year 198687 and not for the Assessment Year

198788. The impugned order holds that in terms of Section 69A (of Income Tax Act, 1961) of

the Act, the financial year in which an assessee is found to be owner

of any jewellery and for which no sufficient explanation is offered,

then the value of such jewellery is deemed to be income of the

assessee in such financial year in which the jewellery was found. In

this case, the impugned order holds that the jewellery was found to

be owned by the appellant only on opening the locker i.e. on 28

July 1986. Consequently, the year of assessment in respect of such

deemed income for unexplained jewellery would be the Assessment

Year 198788.

8. We shall now deal with the submission made in respect of

both the above questions separately as under:

9. Question 1:

(a) Mr. Subramaniam, the learned Counsel for the

appellant in support of the appeal with particular reference to

questions submits that the locker key was found by the revenue on

20 March 1986 at the time they conducted the search of the

appellant's premises. Thus it would be on that date, that the

jewellery valued at cost of Rs.2.01 lakh was found in the ownership

of the appellant for the purposes of Section 69A (of Income Tax Act, 1961). The

finding of the jewellery it is submitted was not dependent upon

opening of the locker but on the revenue having possession of the

keys to the locker which contained the jewellery. In these

circumstances, it was submitted that the jewellery was found in the

previous year relevant to Assessment Year 198687 and not

Assessment Year 198788. In support, Mr. Subramaniam also

placed reliance upon the decisions of Gauhati High Court in Patoa

Brothers Vs. CIT1

, Madhya Pradesh High Court in Harlal Mannulal

Vs. CIT2

and of this Court in Mathuradas Gokuldas Vs. CIT3

.

(b) As against the above, Mr. Pinto, the learned

Counsel for revenue in support of the impugned order states that

the locker keys which were seized on 20 March 1986 belonged not

to the appellant but to one Mrs. Malani. Therefore it is only on

opening the locker that the quantum/value of the jewellery could be

ascertained for subsequent decision/finding on ownership.

Consequently, in terms of Section 69A (of Income Tax Act, 1961), the ownership of

the appellant in respect of the jewellery in the locker of Mrs. Malani

was found only on opening of the locker. Thus the Assessment Year

198788 is the correct assessment year to which jewellery has been

brought to tax as deemed income in view of unexplained jewellery.

(c) We have considered the rival submissions.

Section 69A (of Income Tax Act, 1961) provides that where in any financial year, an

assessee is found to be the owner of any jewellery which is not

recorded in the books of account and the explanation offered by

assessee about the nature and source of acquisition is not

satisfactory, then value of such jewellery would be deemed to be

income of the assessee in the year in which the assessee was found

to be the owner of the jewellery. Admittedly, the locker key which

was seized by the department during the course of the search on 20

March 1986, did not belong to the appellant. Thus on that date the

quantum of jewellery in the locker of Mrs. Malani which belonged

to the appellant could not be ascertained/forecast. The normal

presumption would be the jewellery in the locker of Mrs. Malani

would belong to her and not to another person. Therefore, it is only

on opening of the locker of Mrs. Malani on 28 July 1986, did the

revenue find the jewellery and also that some part thereof, belonged

to the appellant as claimed by the appellant and as also declared by

Mrs. Malani in her assessment proceedings as recorded in the order

of her Assessing Officer at Kolkata on 25 November 1986. Thus it is

only in the previous year relevant to the Assessment Year 198788

i.e. financial year 1 April 1986 to 31 March 1987 that the appellant

was found to be the owner of the jewellery in the locker belonging

to Mrs. Malani.

(d) The three decisions relied upon by the

appellant do not have any application to the present facts. The

basic difference in all the cited cases to the present facts is that the

locker key which was seized on 20 March 1986 did not belong to

the appellant but to one Mrs. Malani and therefore it was only on

the opening of her locker that the question of finding jewellery in

the locker and if found, the ownership of such jewellery would arise

for determination. In all the cited cases the offending goods/money

etc was found in the possession of the party in whose hand Section

69A of the Act was applied.

(e) So far as decision in Patoa Brothers by Gauhati

High Court is concerned, the facts are that the revenue during the

course of search proceedings found at the residence of the applicant

therein undeclared articles such as Swiss made wrist watches, hair

and main springs and Indian currency notes, etc. at a total value of

Rs.1.2 crores. This was assessed to income under Section 69A (of Income Tax Act, 1961) of

the Act. The search took place on 3 March 1970. The revenue

assessed the applicant therein to tax for the Assessment Year 1970

71. However the applicant therein claimed that as ownership of the

articles found in its residence was determined only when an

assessment order was passed on 25 August 1971, the appropriate

assessment would be the Assessment Year 197273. The Gauhati

High Court on the basis of plain interpretation of Section 69A (of Income Tax Act, 1961) of the

Act held that the date on which the applicant was found to be in

possession of the jewellery, etc. would be the date to be taken into

consideration while assessing the party to tax. The fact that the

assessment order renders a finding that the applicant in whose

possession the jewellery was found is the owner will have

retrospective effect to the date the articles were seized. In this case,

admittedly the jewellery was found and seized only on the opening

of the locker of Mrs. Malani on 28 July 1986. Therefore the

assessment year in the present case is correctly the Assessment Year

198788.

(f) The next decision relied upon by the appellant

was of Madhya Pradesh High Court in the case of Harlal Mannulal.

In the that case for the Assessment Year 197374, the relevant

previous year of the applicant therein was 19 October 1971 to 5

November 1972. For the Assessment Year 197374, an addition of

Rs.20,000/ as income from undisclosed sources was made by the

Assessing Officer. This was on the basis of statement filed by the

appellant alongwith his return for the Assessment Year 197273 that

he was inter alia possessed of Rs.20,000/ on 18 October 1971 i.e.

one date before the commencement of the relevant previous year.

The Court held that as Rs.20,000/ of unexplained money declared

by the applicant on 18 October 1971 alongwith his return of income

for the Assessment Year 197273 ought to have been added to the

assessee's income for the Assessment Year 197273 and not for the

Assessment Year 197374 as done by the authorities. In this case,

the jewellery was found in the locker of Mrs.Malani only on opening

it on 28 July 1986 unlike in the case of Harlal Mannulal where an

unexplained cash of Rs.20,000/ was disclosed by the applicant in

its return of income for the Assessment Year 197273 and therefore

it was to be asessed in the Assessment Year 197273.

(g) The last case relied upon by the appellant is

Mathuradas Gokuldas decided by this Court wherein the assessee

had made a declaration on 19 January 1946 that she possessed 138

notes of Rs.1,000/ each. The revenue assessed the aforesaid

Rs.1,38,000/ representing 138 notes as income from undisclosed

sources and bought it to tax in the Assessment Year 194748. This

Court held that income from undisclosed sources has to be assessed

in the relevant assessment year dependent upon the financial year

in which such income has been declared. In these circumstances,

the assessment year applicable would be the Assessment Year 1946

47 when the income was decided and not Assessment Year 194748

as done by the authorities under the Act. The aforesaid decision

also has no application to the present facts, as admittedly the

jewellery was found only on 28 July 1986 on opening the locker

belonging to Mrs. Malani for which the relevant Assessment Year is

198788.

(h) In view of the above, so far as the first question

is concerned, we find no infirmity in the impugned order of the

Tribunal and the same is answered in the affirmative in favour of

the revenue and against the assessee.

10. Question 2:

(a) It was urged by Mr. Subramaniam that the

jewellery found in the locker of Mrs. Malani belonging to the

appellant was sourced from the amounts received by the appellant

in cash from M/s Industrial Meters Ltd. in which he was Director

and the same was a subject matter of consideration by the revenue

for the Assessment Year 198687. Thus seeking to charge the tax on

the same jewellery, as deemed income where the source of jewellery

is found in diaries which were the subject matter of consideration

during the Assessment Year 198687. Thus charging of tax in the

Assessment Year 198788 would lead to double taxation.

(b) As against the above, Mr. Pinto submits that the

occasion to tax the jewellery found in the locker of Mrs. Malani

valued at Rs.2.01 lakh during the Assessment Year 198687 does

not arise. This for the reason that it has never been the appellant's

case that the jewellery which was found on opening of Mrs. Malani's

locker was jewellery which had been purchased out of the cash

entries found in the diary maintained by the employee of M/s

Industrial Meters Ltd. evidencing receipt of cash by the appellant.

(c) The contention urged before us is that the

amount of Rs.2.01 lakh is actually a part of Rs.9.73 lakh which were

a part of the entries made in a diary by one Mr. Gandhi, the Chief

Accountant of M/s Industrial Meters Ltd. of which the appellant was

a Director. This diary kept a record of amount of cash paid by Mr.

Gandhi to the appellant. It is on the basis of the above diary that

the appellant contends that the jewellery found in the locker on 28

July 1986 had been acquired by him out of the cash amount given

by M/s Industrial Meters Ltd. to the appellant. The entries in the

diary according to the appellant were a subject matter of

consideration by the Assessing Officer for the Assessment Year

198687. Consequently, it is submitted that the addition to be made

on account of jewellery found in the locker ought to have been

made in the Assessment Year198687 and not in Assessment Year

198788.

(d) The aforesaid explanation is not acceptable for

the reason that at no point of time, the jewellery found in the locker

was sourced from the cash received by the appellant from M/s

Industrial Meters Ltd. The case of the appellant has always been

the jewellery found in the locker was a gift received by him on 27

January 1986 from his aunt. This theory of gift being received from

his aunt was not accepted by the authorities under the Act including

the Tribunal. Thus the deemed income being the cost of jewellery

found in the locker of Mr. Malani being assessed to tax in

Assessment Year 198788 cannot be found fault with.

(e) In the circumstances, the second question as

framed has to be answered in negative i.e. in favour of the revenue

and against the appellantassessee.

11. Accordingly the appeal is dismissed. No order as to costs.

[N.M. JAMDAR, J] [M.S. SANKLECHA, J.]

×

Similar Ripples

Questions

Jewelry Ownership Dispute: Court Upholds Tax Assessment on Unexplained Jewelry

Write your CommentSimilar Posts

Generic

- Reportdata/3623.pdf