Jewelry Valuation Dispute: Court Upholds Tax on Undisclosed Income

Full News

Jewelry Valuation Dispute: Court Upholds Tax on Undisclosed Income

Jewelry Valuation Dispute: Court Upholds Tax on Undisclosed Income

This case involves a dispute over whether certain jewelry found during a tax search should be considered unaccounted income. The appellants claimed the jewelry belonged to their deceased parents and minor children, supported by valuation reports. However, the court upheld the tax authorities’ decision to treat the jewelry as undisclosed income, as the appellants failed to provide sufficient evidence to prove ownership by other family members.

Get the full picture - access the original judgement of the court order here

Case Name

Paras Shantilal Shah vs. Deputy Commissioner of Income Tax (High Court of Bombay)

Income Tax Appeal No. 1134 of 2000

Date: 21st August 2015

Key Takeaways

- Valuation Reports Insufficient: The court found that valuation reports alone, without corroborative evidence, do not prove ownership of jewelry by deceased parents or minor children.

- Statements on Oath: The appellants’ statements made under oath during the search were crucial, as they admitted the jewelry was part of their undisclosed income.

- Section 69A (of Income Tax Act, 1961) Application: The court applied Section 69A (of Income Tax Act, 1961), treating the unexplained jewelry as income of the appellants.

Issue

Was the jewelry found during the tax search unaccounted income of the appellants, despite their claims of ownership by deceased parents and minor children?

Facts

- The appellants are part of a family group involved in trading electronic items.

- A tax search on October 11, 1996, revealed gold and diamond jewelry in their possession.

- The appellants claimed the jewelry belonged to their late mother, father, and minor children, supported by valuation reports.

- The mother had passed away in 1990, and the jewelry was allegedly distributed among family members.

Arguments

- Appellants: Argued that the jewelry belonged to their deceased parents and minor children, as indicated by valuation reports. They contended that the jewelry should not be taxed as their income.

- Tax Authorities: Maintained that the jewelry was unaccounted income, as the appellants failed to provide sufficient evidence of ownership by other family members. The statements made under oath during the search supported this view.

Key Legal Precedents

- Section 69A (of Income Tax Act, 1961): This section was pivotal in the court’s decision, as it allows for the treatment of unexplained assets as income.

- The court emphasized that valuation reports are “dumb documents” without corroborative evidence.

Judgement

The court ruled in favor of the tax authorities, affirming that the jewelry was unaccounted income of the appellants. The court found no reason to interfere with the Tribunal’s decision, as the appellants’ statements on oath and lack of evidence to support their claims were decisive.

FAQs

Q: Why were the valuation reports not enough to prove ownership?

A: The court considered valuation reports insufficient without additional evidence to corroborate the claims of ownership by the deceased parents or minor children.

Q: What role did the appellants’ statements on oath play in the decision?

A: The statements made under oath were crucial, as they admitted the jewelry was part of their undisclosed income, and these statements were not retracted or contradicted later.

Q: What does this decision mean for the appellants?

A: The appellants are required to pay taxes on the jewelry as it was deemed unaccounted income. The court’s decision underscores the importance of providing concrete evidence when claiming ownership of assets.

1. These four appeals under Section 260A (of Income Tax Act, 1961) (the 'Act') impeach the common order dated 7 December 1999 passed by the Income Tax Appellate Tribunal (the 'Tribunal') in respect of four appellants/assessees (belonging to the same group). The impugned order concerns itself with an assessment for the block period 1 April 1996 to 11 December 1996.

2. All these four appeals were admitted on the following substantial question of law:

“(A) Whether on the facts and circumstances of the case and in law the Tribunal was right in holding that the seized jewellery represented unaccounted income of the appellant when documentary evidence was found at the time of search to show that part of it belonged to the appellants father, late mother and the minor children who were wealthtax and income- tax assessees in the earlier years.”

3. So far as Appeal No. 1135/2000 (Pragna R. Shah) and 1136/2000 (Priti Paras Shah) are concerned, besides Question A above, the appeal was admitted on the following additional substantial question of law:

“(B) Whether on the facts and circumstances of the case and in law the Tribunal erred in rejecting the cash method of accounting followed by the assessee and substituting the mercantile method in relation to the accrued interest on loan advanced to the landlord?”

Regarding Question No.A:

4. Briefly the facts leading to these appeals are as under:

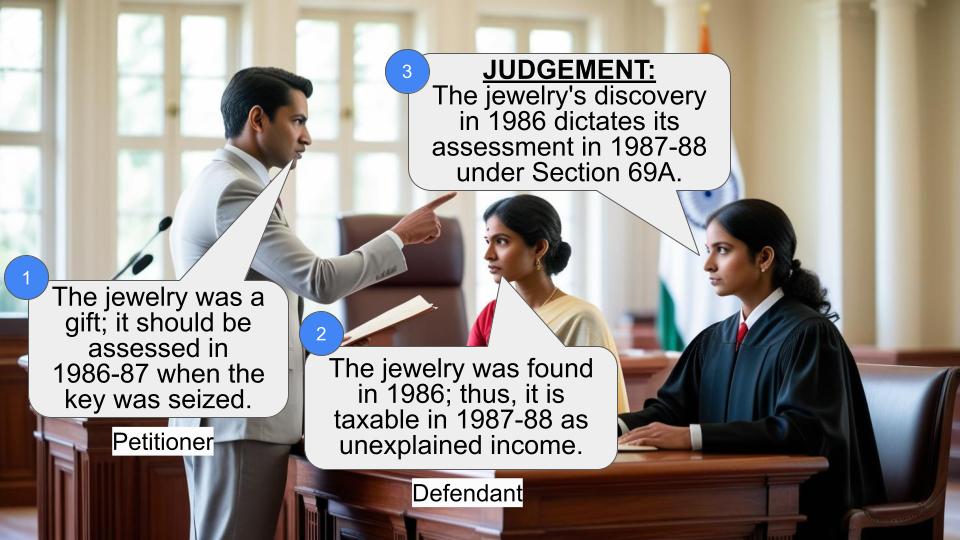

(a) The appellants/assessees are a part of the family group engaged in the business of trading in electronic items including its export to African countries. Besides the group also carries on the business of bill discounting. On 11 October 1996, a search and seizure operation under Section 132 (of Income Tax Act, 1961) was undertaken by the officers of the revenue at the residence and office premises of the appellants/assessees group. During the course of search, gold jewellery, diamond jewellery and silver articles were found in the possession of the appellants/assessees.

(b) On 12 October 1996, Paras Shah (one of the appellants herein) made a statement on oath under Section 132(4) (of Income Tax Act, 1961) in response to Question 21 as under:

“Q.21 During the search total gold and diamond jewellery found 2153 gms. and diamonds valuing at Rs.7,16,930/ and for Rs.83,075/ on person. Kindly explain to whom these items belong and the source of acquisition with relevant documentary evidences. Ans. Myself and my family members were Wealth Tax payees and till the old limit and as per the Wealth Tax Valuation Reports of total gold jewellery of 2064 gms. was already declared in the relevant years. My mother expired in 1990 had a jewellery as per a Valuation report dated 31.3.88, had a jewellery of Rs.2,34,070/ which is given to the lady members. However, I have made valuation of jewellery belongings to all my family members which is in total 34.69.5 gms. as in July 1996. Considering the gap for which I am not in a position to produce bills, etc. and declared Rs.1 lakhs on a/c, this gap. Regd. the diamond jewellery one to two items are tallying regd. the rest I make a request that jewellery on person may not be seized, value of which is in total Rs.1,50,195/ (Rs. One Lakh Fifty Thousand One Hundred Ninety Five), I voluntarily declare as my income in addition to the balance Rs.4,66,560/ (Rs. Four Lakh Sixty Six Thousand Five Hundred Sixty). In the nut shell on account of jewellery my total disclosure is Rs.7,16,750/ (Rs. Seven Lakhs Sixteen Thousand Seven Hundred and Fifty).” Thus the appellants offered/declared as a group the total amount of Rs.7.66 lacs (being undisclosed gold jewellery) and Rs.4.66 lacs (being undisclosed diamond jewellery) to tax.

(c) On 14 November 1996, on opening of the bank locker, jewellery valued at Rs.4.60 lacs was found. At that time, Mr. Paras Shah made a statement on oath under Section 132(4) (of Income Tax Act, 1961) and in response to Question 2 replied as under:

“Q.2 During the course Bank Locker Search operation of lockers No. & L 3236, gold jewellery valued as per Valuation Report of M/s S.C. Kapoor dated 14.11.96 at Rs.4,63,280/ was found. Please explain the nature of possession and the source of acquisition of the said jewellery items?

Ans. These items which are mostly ladies items have been acquired by me and my family members within the last fourfive years. Some of the items might have been received by gifts also. However, since we do not have any supporting documentary evidence for the same in our possession, I hereby offer the value thereof approp., i.e. Rs.4,60,000/ (Rs. Four Lakhs Sixty Thousand Only), as my additional income u/s. 132(4) (of Income Tax Act, 1961) I shall be paying the taxes thereon, in time as per law.”

Thus the aforesaid jewellery was also offered to tax as the appellant did not have any supporting documentary evidence to establish its purchase.

(d) Thereafter on 30 November 1996, Mr. Paras Shah addressed a communication to the Additional Director of Income Tax seeking to explain the jewellery found in the possession of the group on 11 October 1996 and 14 November 1996 as under:

“This copy of reports were handed over to ADIT Mr. Sanjay Mishra and Department Valuer Mr. Suresh Kapoor at the time of search on 11th Oct. 1996 at my residence. This we have already informed you earlier also. The valuation was done as at 31st March 1996, for filling Wealthtax return on or before the due date. All our jewellery seized by department percent matches with this valuation reports.”

5. Consequent to the above search, notices under Section 158BC (of Income Tax Act, 1961) was issued to the appellants/assessees. In response returns of income for the block period commencing from 1 April 1996 to 11 October 1996 were filed by the appellants/assessees individually. The appellants/assessees were personally heard by the Assessing Officer. At the hearing, it was submitted on behalf of the group that in case its explanation that the unaccounted/undisclosed jewellery is accounted for by valuation reports, wealth tax returns and the valuation report of the jewellery possessed by their father and their late mother who died in the year 1990 is not found acceptable, then the allegedly unexplained/undisclosed jewellery be distributed amongst the four appellants/assessees equally i.e. at 25% each.

6. The Assessing Officer by four separate orders dated 31 October 1997 did not accept the explanation offered by the appellants/assessees in respect of the unexplained/undisclosed jewellery nor the explanation by letter dated 30 November 1996. In these circumstances, the unaccounted jewellery and silver articles amounting to Rs.13,65,444/ was distributed amongst each of the four appellants/assessees at 25% each i.e. Rs.3,41,361/. The aforesaid sum of Rs.3.41/ lacs was added to the income of each of the appellants/assessees.

7. Being aggrieved by the order dated 31 October 1996, all the four appellants/assessees filed appeals before the Tribunal. The Tribunal by a common impugned order dated 7 December 1999 dismissed all the four appeals on this issue. This for the reason that the appellants had in a statement made on oath under Section 132(4) (of Income Tax Act, 1961) admitting that the jewellery recovered from them and in their locker was part of its undisclosed income and offered the same to tax. These statements on oath were voluntarily made and it is not even alleged that ill treatment and/or any unfair measures were adopted while recording the statement made by the appellants/assessee. In these circumstances, it held that there is no reason to disbelieve the statement made by the appellants/assessees immediately at the time of search/discovery of the undisclosed jewellery. Further it also held that mere possession of valuation reports does not result in the appellant having disclosed the source of jewellery. Resultantly the four appeals on the above account were dismissed by the common impugned order.

8. Mrs. S. Jagtiani, the learned Counsel in support of the appeals submits as under:

(a) The Assessing Officer as well as the Tribunal erred in having completely ignored the documentary evidence produced by the appellant. These documents show that the part of the allegedly undisclosed jewellery belonged to the appellants' father, late mother and their minor children as seen by valuation reports of jewellery in their possession.

(b) The impugned order erroneously proceeds on the basis that Section 69A (of Income Tax Act, 1961) would apply to the facts of the present case. This by ignoring the documentary evidence in the form of documentary evidence of the jewellery in the name of various family members would clearly establish the source of the excess amount of jewellery found in their possession during the search.

(c) In any view of the matter, once the appellant had produced the evidences that the jewellery belonged to their father and late mother, then the proper course for the Assessing Officer was to issue notice under Section 158BD (of Income Tax Act, 1961) to them. It is not open in such cases to assess jewellery belonging to other persons in the hands of the appellants/assessees; and

(d) No evidence was found during the course of the search that the jewellery was acquired from undisclosed sources of income. Thus no addition on the above account could have been made by the Assessing Officer and upheld in the impugned order by the Tribunal.

9. Mr. Pinto, the learned Counsel for the revenue in support of the impugned order submits that:

(a) The authorities under the Act have reached concurrent findings of fact that undisclosed/undeclared jewellery found in the possession of the appellant belonged to the appellant. Thus amount spent on acquisition of the same is chargeable to tax. The same is not shown to be perverse. Therefore this Court should not interfere with the aforesaid finding of the fact.

(b) Section 69A (of Income Tax Act, 1961) is clearly applicable to the present facts. The authorities found that the nature and source of acquisition of unexplained jewellery was not explained by the appellant. Consequently, the value of the jewellery is deemed to be an income of the assessees in terms of Section 69A (of Income Tax Act, 1961) as done in the present cases;

(c) The documents in the nature of valuation report produced by the appellant by itself do not establish that the undisclosed jewellery belonged to the appellant's father and late mother. Moreover there is no reason to presume that it had not been distributed amongst the appellants/assessees before the search operation; and

(d) The occasion to invoke Section 158BD (of Income Tax Act, 1961) and issue notices to the father, late mother and minor children in the present facts would not arise. This is for the reason that the explanation offered by the appellant that the jewellery found in their possession belonged to their father, late mother and the minor children under was not found acceptable.

10. We have considered the rival submissions. From the facts as recorded hereinabove, it is clear that when the appellant's premises was searched on 11 and 12 October 1996, gold and diamond jewellery were found in their possession which they were unable to explain. It was in that context that on 12 October 1996, a statement was made on oath under Section 132(4) (of Income Tax Act, 1961) by the appellant that they are not in a position to produce any evidence in respect of the gold and diamond jewellery found in their possession to the extent of Rs.7,16,750/. This after taking into account the jewellery belonging to their father, late mother and valuation done of the family jewellery in July 1996. Moreover it is specifically stated in the statement on oath that the jewellery belonging to their late mother already stood distributed amongst the appellants. Further on 14 November 1996 when the bank locker was opened during the search process jewellery of approximately Rs.4,60,000/ was found. The appellants on oath again stated that they are unable to produce any evidence about the purchase of the jewellery found and undertake to pay tax thereon. It was only much later i.e. on 30th November 1996 that the appellant wrote a letter to the Additional Director of Income Tax seeking to explain the jewellery seized by the department in particular the undisclosed jewellery found on 12 October 1996 and 14 November 1996 on the basis of valuation reports of the jewellery which they claim to be available at all times. It is very pertinent to note that letter dated 30 November 1996 addressed to the Additional Director of Income Tax does not indicate that they are retracting the earlier statements made on oath. Further it does not state that the statement made on 12 October 1996 and 14 November 1996 were incorrect or even make an attempt to explain away the categorical statement on oath. There is also no allegation of any ill treatment which led the appellant to make a statement on 12 October 1996 and 14 November 1996 which are contrary to the facts.

11. In the above circumstances, the communication dated 13 November 1996 cannot supersede/replace the statement made on

12 October 1996 and 14 November 1996. This is particularly so as the statements of 12 October 1996 and 14 November 1996 were statements made on oath nor any circumstances explained which would warrant/justify ignoring the earlier statements. On the aforesaid ground alone the substantial question (A) needs to be answered in favour of the revenue.

12. Notwithstanding the above, the impugned order of the Tribunal has considered the explanation offered by the appellant in respect of the excess undisclosed jewellery. The explanation now offered is that the excess jewellery found during the search of the appellant's premises belong to the appellant's late mother and the appellant's father and all stand explained by the valuation report of July 1996. It is not disputed that the valuation report indicates the name of the father and mother as being the persons who claim to be the owner of the jewellery. The mother of the appellant passed away far back as 1990. In the normal course of human conduct the jewellery of the mother would have been distributed amongst her children soon after her death. This is also corroborated by the statement made on 12 October 1996 wherein it is stated that the jewellery belonging to their late mother has been distributed amongst the lady members of the family. So far as the valuation report indicates that some jewellery belongs to the father and it is in their possession, it would have been so stated at the time when the excess jewellery was found in their possession. The valuation reports are dumb documents and by itself do not indicate in the absence of any other corroborative evidence that the jewellery belongs to the father and the late mother and/or the minor children of the appellants. In the above view, we find that the impugned order of the Tribunal calls for no intereference.

13. The next submission of the appellant with regard to the applicability of Section 69A (of Income Tax Act, 1961) is not required to be considered, as we find that the authorities have proceeded on the basis of the statement made on oath under Section 132(4) (of Income Tax Act, 1961) declaring that the undisclosed jewellery belonged to them. These statements of oath has not been withdrawn and/or retracted by appellant at any point of time till date. Therefore, there is no occasion for the authorities to come to the conclusion that the undisclosed jewellery belongs to the father or late mother. Consequently issuing a notice under Section 158BD (of Income Tax Act, 1961) to the father and to the legal heirs of the late mother does not airse.

14. In the above view, there is no reason to examine various decisions cited by the appellants in support of the either Section 69A (of Income Tax Act, 1961) or Section 158BD (of Income Tax Act, 1961). Accordingly, Question A as formulated is answered in affirmative i.e. against the appellants/assessees and in favour of the revenue.

Regarding Question No.B :

15. During the course of the search operation, the officers of the revenue on 11 October 1996 found documents dated 13 August 1996 indicating Rs.16 lacs and Rs.34 lacs were given as construction loan to Mrs. Kausalya Bajaj and Mr. Kishor Bajaj. Clause 7 thereof reads as under:

“the owner shall pay to the prospective tenants interest on the amount of such construction loan paid by the prospective tenants to the owners as aforesaid the rate of 4% per annum from the date of such loan is paid by the prospective tenants to the owners. Till the time outstanding amount of such loan is prepaid.”

16. On the basis of the above clause, during the course of assessment proceedings, the appellants viz. Mrs. Priti Shah and Mrs. Pragna Shah were called upon to show cause why the interest amount contemplated in the agreement which has not been shown in the return of income should not be charged to tax. The appellants in response pointed out that the interest amount had not been received. The same would be disclosed to the revenue in the year of receipt. Therefore there was no obligation to disclose the interest amount which were receivable and pay tax on it till such time as the interest is received. The Assessing Officer did not accept the submission of the appellants and held that in view of the clause in the agreement, the appellants are liable to pay interest on loan of Rs.16 lacs and Rs.34 lacs made by Mrs. Priti Shah and Mrs. Prgna Shah for the period 13 August 1992 to 10 October 1996. This interest income which had not been disclosed was also added to the income of the appellants i.e. Mrs. Priti Shah and Mrs. Prgna Shah.

17. Being aggrieved, Mrs. Priti Shah and Mrs. Pragna Shah filed appeals to the Tribunal. The Tribunal as a part of a common impugned order held that in view of the Clause 7 of the agreement, the interest income receivable for the period 1992 to 1996 would be payable on accrual basis. This was undisclosed income and had not been returned in their regular return of income. Therefore the same was brought to tax in block assessment of the appellants i.e. Mrs. Priti Shah and Mrs. Pragna Shah.

18. Mrs. Jagtiani, the learned Counsel appearing for the appellant in support of the impugned appeal submits as under:

(a) The appellants are following a cash method of accounting i.e. receipt basis. Consequently till such time as the interest amount is received, no question of payment of tax on the receipt of interest can arise; and

(b) The interest income earned could not be treated as undisclosed income in a block assessment. The interest income could be assessed to tax in regular assessment but could never be a part of a block assessment. This is so as block assessment only applies to undisclosed income found during the course of a search. On the above basis, it was submitted that Question B as formulated be answered in favour of the appellant.

19. As against the above, Mr. Pinto, the learned Counsel for revenue in support of the impugned order urges:

(a) The appellants/assessees did not follow the cash system of accounting i.e. receipt basis. In the present case, there is no evidence to indicate that the appellants/assessees were maintaining any account in writing so as to hold that they were following the cash system of accounting; and

(b) The loan agreement dated 13 August 1992 was found during the search process under Section 132 (of Income Tax Act, 1961). It was this loan agreement which led the revenue to conclude that as the appellants/assessees had not disclosed its income during the regular course of assessment, interest income earned by the appellant/assessees in terms of loan agreement dated 13 August 1992 is certainly an undisclosed income chargeable to tax for the block assessment period 1 April 1988 to 11 October 1996. In the above view, it is submitted that the Question B as formulated be answered in favour of the revenue.

20. We have considered the rival submission. The loan agreement dated 13 August 1992 was found only during the course of search operation under Section 132 (of Income Tax Act, 1961). Prior to the search, the revenue was unaware of the aforementioned grant of loan and accrued interest thereon. Consequently the interest amount earned on the loan was chargeable to tax in the block assessment period as undisclosed income.

21. The substantial question of law which arises for our consideration has proceeded on the basis that the impugned order of the Tribunal erred in rejecting/ignoring the cash method of accounting followed by the appellants/assessees. We find that both the authorities have rendered a finding of fact that the borrower would pay the appellant an interest at 4% p.a. from the date of loan till its repayment. The Tribunal in the impugned order has clearly recorded a finding of fact that the appellant do not maintain regular books of account. Consequently no occasion to claim benefit of cash system of accounting can arise as there was no method of accounting followed by the appellant. In the above view, the finding of the Tribunal being a finding of fact is not shown to be perverse. The interest which has been received by the appellant was in terms of Clause 7 of the agreement and this being a part of the undisclosed document found during the course of the search would necessarily result in the interest being earned thereon as provided therein being added to the appellants'/assessees' income for the block period.

22. The appellants have not established before the authorities that they were following the cash system of accounting. In fact at no stage was it brought to the notice of the authorities in the return of income filed that loans have been advanced to the extent of Rs.16 lacs and Rs.34 lacs to Mr. and Mrs. Bajaj as a part of their assets in the balance sheet to be filed alongwith the return of income by the two appellants. In fact as the assessee was not following any method of accounting, non disclosure of giving of loan to Mr. and Mrs. Bajaj and the interest received in fact or in accrual method has not been disclosed to the authorities. In fact, the best evidence which could be produced by the appellants/assessees was the evidence of Mr. and Mrs. Bajaj to point out that they have not paid any interest during the period under consideration for the loan of Rs.15 lacs and Rs.34 lacs. However the appellant did not choose to produce Mr. and Mrs. Bajaj as their witnesses and/or any evidence from them indicating that no interest is paid by them.

23. In these facts, the impugned orders of the Tribunal does not call for any intereference. Accordingly, in view of the above, so far as Question B is concerned, we answer the same in favour of the respondent/revenue and against the appellants/assessees.

24. Question Nos. A and B are answered in favour of the respondent/revenue and against the appellants/assessees. Thus, we see no reason to interfere with the impugned order of the Tribunal. Accordingly, the appeal filed by the appellants/assessees is dismissed. No order as to costs.

[N.M. JAMDAR, J] [M.S. SANKLECHA, J.]

×

Similar Ripples

Questions

Jewelry Valuation Dispute: Court Upholds Tax on Undisclosed Income

Write your CommentSimilar Posts

Generic

- Reportdata/3509.pdf