Late Notice Invalidates Tax Assessment: Court Rules on Timely Service

Full News

Late Notice Invalidates Tax Assessment: Court Rules on Timely Service

Late Notice Invalidates Tax Assessment: Court Rules on Timely Service

This case involves the Commissioner of Income Tax (CIT) appealing against an order passed by the Tribunal, Delhi Bench 'B', concerning the assessment year 1992-93. The central issue was whether a notice under section 143(2) (of Income Tax Act, 1961) was served on the assessee within the period of limitation. The High Court dismissed the appeal, ruling in favor of the assessee.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs. Inderpal Malhotra (High Court of Delhi)

ITA 742/2006

Date: 11th October 2007

Key Takeaways:

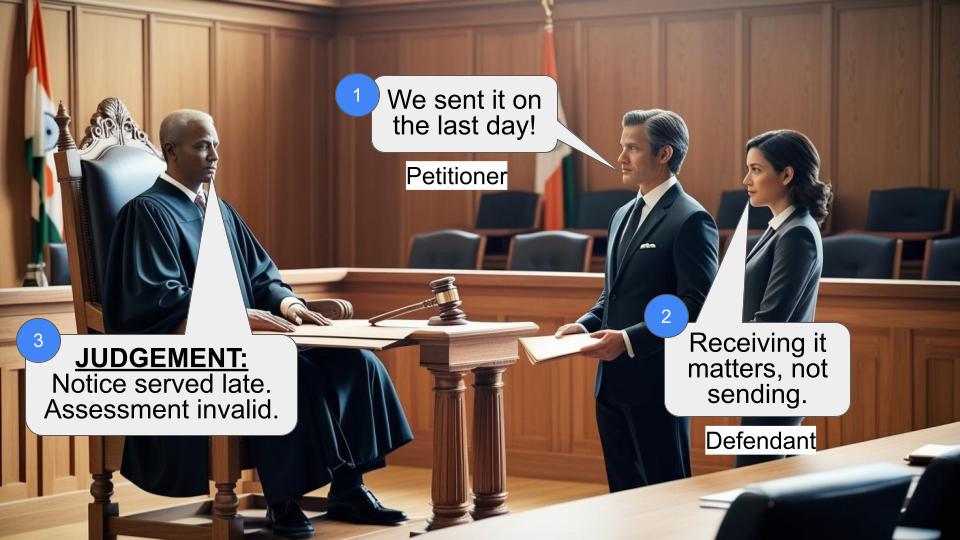

1. Mere issuance of notice is not sufficient; actual service within the limitation period is crucial.

2. Sending a notice by registered post on the last day of the limitation period is not considered timely service.

3. The court prioritizes the actual receipt of notice by the assessee over the act of sending it.

Issue:

Was the notice under section 143(2) (of Income Tax Act, 1961) served on the assessee within the period of limitation?

Facts:

1. The case pertains to the assessment year 1992-93.

2. The notice under section 143(2) (of Income Tax Act, 1961) was issued on November 30, 1993, by registered post.

3. November 30, 1993, was the last date of the limitation period.

4. The notice was not sent by any other method, such as hand delivery.

Arguments:

The Revenue (CIT) likely argued that the issuance of the notice on the last day of the limitation period should be considered valid service. However, the specific arguments are not detailed in the provided judgment.

The assessee's arguments are not explicitly mentioned, but it can be inferred that they contested the validity of the notice based on the timing of its service.

Key Legal Precedents:

The court relied on the case of CIT vs. Vardhman Estate (P) Ltd. (2007) 208 CTR (Del) 251 : (2006) 287 ITR 368 (Del). In this case:

1. A notice was sent by speed-post one day before the expiry of the limitation period (October 30, 2002).

2. The Revenue's contention that the notice should be deemed served was rejected.

3. The court clarified that the statute requires actual service of the notice, not merely its dispatch or issuance.

Judgement:

1. The High Court dismissed the appeal, ruling in favor of the assessee.

2. The court held that since the notice was issued by registered post on the last day of the limitation period, there was no possibility of it being served in time.

3. The court emphasized that actual service of the notice within the limitation period is required, not just its issuance.

4. No substantial question of law was found to arise from this case.

FAQs:

1. Q: What is the significance of section 143(2) (of Income Tax Act, 1961) notice?

A: Section 143(2) (of Income Tax Act, 1961) notice is a crucial step in the income tax assessment process, allowing the tax department to scrutinize a taxpayer's return.

2. Q: Does sending a notice on the last day of the limitation period always invalidate it?

A: Not necessarily, but if sent by post on the last day, it's unlikely to be considered valid as it cannot be received by the assessee on the same day.

3. Q: What's the difference between issuance and service of a notice?

A: Issuance refers to sending out the notice, while service means the actual receipt of the notice by the intended recipient.

4. Q: How does this judgment impact tax authorities?

A: It emphasizes the need for tax authorities to ensure timely service of notices, not just their issuance, to maintain the validity of their actions.

5. Q: Can tax authorities use other methods to serve notices?

A: Yes, they can use methods like hand delivery to ensure timely service, especially when close to the limitation period.

1. The Revenue is aggrieved by an order dt. 31st May, 2005 passed by the Tribunal, Delhi Bench ‘B’, in ITA No. 416/Del/1996 relevant for the asst. yr. 1992-93.

2. The only issue that arises in this case is whether notice under s. 143(2) was served on the assessee within the period of limitation.

3. It transpires from a perusal of the record of the case that the notice was actually issued on 30th Nov., 1993 by registered post, which was the last date of limitation. There is no way that the notice could have been received by the assessee on the same day unless the notice was sent by hand, which is not so in the present case.

4. In CIT vs. Vardhman Estate (P) Ltd. (2007) 208 CTR (Del) 251 : (2006) 287 ITR 368 (Del) , a notice was sent by speed-post one day before the period of limitation was to expire, that is, on 30th Oct., 2002 and the contention urged by the Revenue in that case was that the notice sent should be deemed to have been served on the assessee. This argument was rejected by this Court and it was made clear that what is required by the statute is not merely the despatch or issuance of the notice but its actual service.

5. Since in the present case it is admitted that as a matter of fact, notice was issued by registered post on the last day of the period of limitation and by no other method, there was no possibility of it being served in time. No substantial question of law arises.

Dismissed.

MADAN B. LOKUR, J

OCTOBER 11, 2007 S. MURALIDHAR, J kapil

×

Questions

Late Notice Invalidates Tax Assessment: Court Rules on Timely Service

Write your CommentSimilar Posts

Generic

- Reportdata/5273.pdf