Full News

Revenue's belated plea on wrong section citation rejected by High Court

Revenue's belated plea on wrong section citation rejected by High Court

This case involves the Commissioner of Central Excise (appellant) against Onkar Travels (P) Ltd. (respondent). The dispute centered around a service tax assessment and the application of Section 74 of the Finance Act, 1994. The High Court dismissed the appeal, rejecting the Revenue's attempt to change their stance on the applicable section.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Central Excise vs Onkar Travels (P) Ltd. (High Court of Punjab & Haryana)

C.E.A. No. 169 of 2006

Date: 17th January 2008

Key Takeaways:

1. Courts are unlikely to entertain new arguments raised for the first time in higher appeals.

2. Consistency in legal arguments throughout the appeal process is crucial.

3. The importance of citing the correct legal provisions in show cause notices and orders.

Issue:

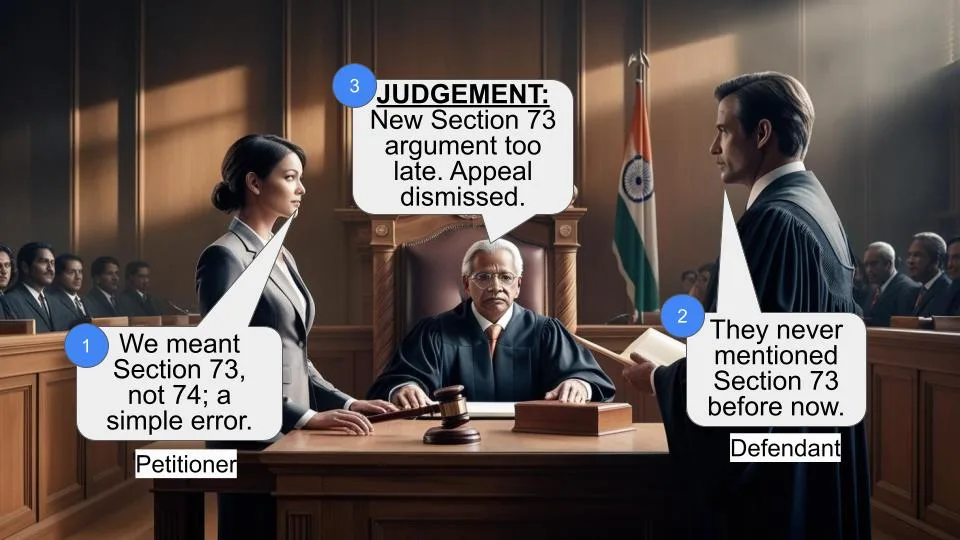

Can the Revenue raise a new plea in the High Court that Section 74 (of Income Tax Act, 1961) was inadvertently mentioned instead of Section 73 (of Income Tax Act, 1961) in earlier proceedings?

Facts:

1. Onkar Travels (P) Ltd. is registered as an Air Travel Agent under the Finance Act, 1994.

2. The company filed quarterly ST-3 returns for several periods ending March 1999.

3. A show cause notice was issued under Section 74 (of Income Tax Act, 1961) to enhance the assessment.

4. The Deputy Commissioner confirmed a demand of Rs.91,858 and imposed a penalty of Rs.1,000.

5. The respondent appealed to the Commissioner (Appeals), who dismissed the appeal.

6. The Customs, Excise & Service Tax Appellate Tribunal allowed the respondent's appeal.

7. The Department filed an appeal in the High Court.

Arguments:

Appellant (Revenue):

- The show cause notice was meant to be issued under Section 73 (of Income Tax Act, 1961), but Section 74 (of Income Tax Act, 1961) was inadvertently mentioned.

- The wrong mention of law should not prevent the assessment of escaped taxable service.

Respondent:

- The question of wrong section mention doesn't arise from the Tribunal's order.

- The Department consistently argued for the applicability of Section 74 (of Income Tax Act, 1961) in lower forums.

- The new argument about Section 73 (of Income Tax Act, 1961) is being raised for the first time in the High Court.

Key Legal Precedents:

No specific legal precedents were cited in this judgment. The case primarily focused on procedural aspects and the consistency of arguments through various stages of appeal.

Judgement:

The High Court dismissed the appeal, stating:

1. The Revenue consistently argued for the applicability of Section 74 (of Income Tax Act, 1961) in lower forums.

2. The new plea about inadvertent mention of Section 74 (of Income Tax Act, 1961) instead of Section 73 (of Income Tax Act, 1961) cannot be entertained for the first time in the High Court appeal.

3. Only substantial questions of law arising from the Tribunal's order can be considered by the High Court.

4. As the argument about wrong section mention was not raised before the Tribunal, it doesn't constitute a substantial question of law arising from the Tribunal's order.

FAQs:

1. Q: Why did the High Court dismiss the Revenue's appeal?

A: The court dismissed the appeal because the Revenue tried to introduce a new argument that wasn't raised in lower forums.

2. Q: What is the significance of Section 74 (of Income Tax Act, 1961) in this case?

A: Section 74 (of Income Tax Act, 1961) pertains to rectification of mistakes in orders, which was not applicable in this case as there was no apparent mistake in the assessment.

3. Q: Could the outcome have been different if the Revenue had consistently argued about the wrong section from the beginning?

A: Possibly. If the Revenue had raised this issue in earlier stages of appeal, the courts might have considered the merits of their argument.

4. Q: What lesson can be learned from this case for future tax proceedings?

A: It's crucial to cite the correct legal provisions in notices and orders, and maintain consistency in legal arguments throughout the appeal process.

5. Q: Does this judgment set any new legal precedent?

A: While it doesn't set a new precedent, it reinforces the principle that courts are unlikely to entertain new arguments raised for the first time in higher appeals.

This order shall dispose of Central Excise Appeals No. 169 of 2006 and 93 of 2007, as in both these appeals, not only the common questions of facts and law are involved, but in CEA No. 93 of 2007, the Customs Excise and Service Tax Appellate Tribunal has decided the appeal by following its earlier decision in the case of M/s Onkar Travels (Pvt.) Ltd.(against which the CEA No. 169 of 2006 has been filed). The facts are being taken from CEA No. 169 of 2006.

In the present case, M/s Onkar Travels (P) Ltd., respondent herein, is a holder of Certificate of Registration in Form ST2 under Section 69 of the Finance Act, 1994 (hereinafter referred to as `the Act') in the category of Air Travel Agent. The respondent had filed quarterly ST-3 returns for the quarter ending September, 1997, December, 1997, March, 1998, June, 1998, September, 1998 and half year ending March, 1999 with the jurisdictional Superintendent of Service Tax. All the ST-3 returns filed were assessed finally by the Superintendent of Service Tax. Subsequently, a show cause notice was issued by the Deputy Commissioner of Service Tax under Section 74 (of Income Tax Act, 1961) to enhance the assessment on the allegation that short levy of service tax was made on the respondent. Vide order dated 20.12.2000, the Deputy Commissioner, Central Excise Division, Jalandhar, confirmed the demand of Rs.91,858/- and also imposed a penalty of Rs.1,000/- upon the respondent.

Feeling aggrieved against the said order, the respondent filed an appeal before the Commissioner (Appeals), Central Excise, Jalandhar, which was dismissed on 27.2.2004, whereby the order of confirming the demand of Rs. 91,858/- and imposing of penalty of Rs. 1,000/- on the respondent by the Adjudicating Authority, was upheld.

Still feeling aggrieved against the said order, the respondent filed an appeal before the Customs, Excise & Service Tax Appellate Tribunal, New Delhi. The Tribunal has allowed the said appeal, while observing that provision of Section 74 (of Income Tax Act, 1961), which pertains to rectification of a mistake, is not applicable, in the facts and circumstances of the case, as there is no apparent mistake in the assessment, which has become final under Section 71 (of Income Tax Act, 1961). Against the said order of the Tribunal, the instant appeal has been filed by the Department, in which it has been claimed that the following three substantial questions of law are arising from the order of the Tribunal :

“(i) Has the Tribunal not committed grave error in arriving at the conclusion that the department did not choose to file appeal before the Commissioner (Appeals); when as per section 85 of the Finance Act “any person” does not include the department; has the opportunity for Rectification of Mistake & Revision (under this section) been taken ?

(ii) Whether the action of department i.e. issue of Show cause notice against improper/faulty assessment order and late decision was not in order ?

(iii) Whether inadvertent mentioning of Section 74 (of Income Tax Act, 1961) in place of Section 73 (of Income Tax Act, 1961) in the show cause notice can deprive the revenue of the legal demand when the Tribunal in the instant order has no where questioned this legality demand on any other ground ? During the course of arguments, learned counsel for the appellant pressed only question No.(iii) and has submitted that actually, while giving notice dated 25.2.2000, the department has inadvertently mentioned Section 74 (of Income Tax Act, 1961) in place of Section 73 (of Income Tax Act, 1961). He submits that actually, the said notice was given under Section 73 (of Income Tax Act, 1961). He further submits that the same mistake was committed, when the Deputy Commissioner, Central Excise Division,Jalandhar, confirmed the demand of Rs. 91,858/- and imposed penalty upon the respondent, while observing in the order dated 20.12.2000 that the assessment requires to be enhanced under Section 74 (of Income Tax Act, 1961). Learned counsel submits that merely because the Revenue Authority has issued show cause notice under the wrong provisions will not debar the Revenue Authority from assessing the escaped taxable service, as it is settled proposition that wrong mentioning of law does not make any difference. Therefore, in the facts and circumstances of the case, question No.(iii) requires consideration by this Court.

On the other hand, learned counsel for the respondent submits that the aforesaid question does not arise from the order of the Tribunal. She submits that before the Tribunal, it was not the stand of the appellant that provision of Section 74 (of Income Tax Act, 1961) is not applicable in the instant case,rather the notice was issued and impugned order was passed under Section 73 (of Income Tax Act, 1961). While referring to the portion of the impugned order, where the departmental representative had submitted before the Tribunal that the order passed by the Superintendent of Service Tax was perfectly legal to recover the service tax which has escaped the assessment and provision of Section 74 (of Income Tax Act, 1961) was fully applicable to the facts and circumstances of the case. She further submits that notice under Section 74 (of Income Tax Act, 1961) can be issued within two years of the date of order, therefore, the said notice was within limitation. Learned counsel submits that throughout before the authorities below, the department had taken the stand that the show cause notice was rightly issued under Section 74 (of Income Tax Act, 1961) as recourse can only be taken under Section 74 (of Income Tax Act, 1961) for recovering the escaped service tax at the time of assessment. The present stand that the revenue authorities initially mentioned the wrong provision in the show cause notice has been taken for the first time before this Court, therefore, it cannot be said that the said substantial question of law is arising from the order passed by the Tribunal.

We have heard learned counsel for the parties and have perused the show cause notice dated 25.2.200, the order dated 20.12.2000, passed by the Deputy Commissioner, Central Excise Division, Jalandhar, order of the Appellate Authority and the order of the Tribunal. The notice was given under Section 74 (of Income Tax Act, 1961). The order confirming the demand of Rs.91,858/- and imposing a penalty of Rs.1,000/- upon the respondent, was passed by the Deputy Commissioner, Central Excise Division, Jalandhar, under Section 74 (of Income Tax Act, 1961). Before the Appellate Authority as well as the Tribunal, the department had taken the stand that the Revenue Authorities have rightly passed the order assessing the escaped service tax by invoking the provision of Section 74 (of Income Tax Act, 1961). Even before the Tribunal, the same stand was taken. For the first time, in this appeal, the appellant has taken the stand that actually, the show cause notice was to be issued under section 73 (of Income Tax Act, 1961), but inadvertently, the provision was wrongly mentioned as Section 74 (of Income Tax Act, 1961). Such plea was never taken by the appellant either before the Appellate Authority or before the Tribunal. Rather before the Tribunal, the representative of the Department had categorically taken the stand that the Revenue Authority was within its power to pass the impugned order under Section 74 (of Income Tax Act, 1961). Undisputedly, Section 74 (of Income Tax Act, 1961) pertains to rectification of the mistake in the order and a rectification can only be made by the same Authority if the mistake is apparent on the record. In the grounds of appeal, the appellant has taken the stand that provision of Section 74 (of Income Tax Act, 1961) is not applicable. Therefore, the only stand is that in the notice as well as the orders passed by the Authorities below, Section 74 (of Income Tax Act, 1961) was inadvertently mentioned instead of Section 73 (of Income Tax Act, 1961). In our opinion, this question cannot be permitted to be raised for the first time in this appeal.

Only those substantial questions of law are to be considered and decided by this Court, which are arising from the order of the Tribunal. In this case, since no such argument was raised before the Tribunal, in our opinion, no such substantial question of law arises from the order of the Tribunal.

Therefore, we do not find any ground to entertain this appeal.

Dismissed.

( SATISH KUMAR MITTAL )

JUDGE

January 17, 2008 ( RAKESH KUMAR GARG )

JUDGE

×

Similar Ripples

Questions

Revenue's belated plea on wrong section citation rejected by High Court

Write your CommentSimilar Posts

Generic

- Reportdata/4995.pdf