Tax Appeal Dismissed: Court Upholds Tribunal's Decision on Transfer Pricing Dis…

Full News

Tax Appeal Dismissed: Court Upholds Tribunal's Decision on Transfer Pricing Dispute

Tax Appeal Dismissed: Court Upholds Tribunal's Decision on Transfer Pricing Dispute

This case involves an appeal by the Principal Commissioner of Income Tax against RBS Financial Services (India) Pvt. Ltd. The dispute centered around transfer pricing issues for the assessment year 2008-09. The Income Tax Appellate Tribunal (ITAT) had remanded the case back to the Assessing Officer for fresh consideration. The High Court dismissed the Revenue's appeal, affirming the ITAT's decision.

Get the full picture - access the original judgement of the court order here

Case Name:

Principal Commissioner of Income Tax Vs RBS Financial Services (India) Pvt. Ltd. (High Court of Bombay)

Income Tax Appeal No.1417 of 2017

Date: 20th January 2020

Key Takeaways:

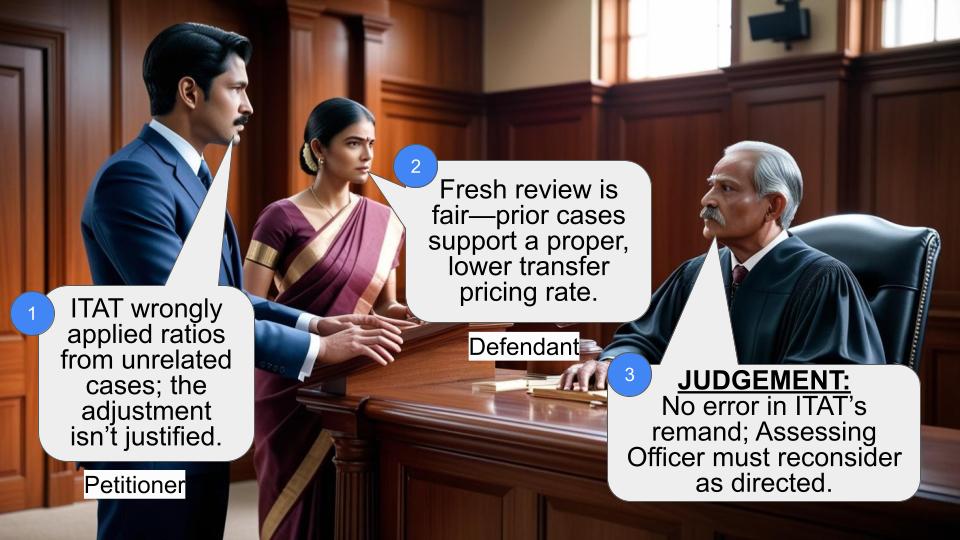

1. The court upheld the ITAT's decision to remand the case for fresh consideration.

2. The judgment emphasizes the importance of proper determination of Arm's Length Price in transfer pricing cases.

3. The court relied on previous ITAT decisions in similar cases to guide the fresh assessment.

Issue:

Was the Income Tax Appellate Tribunal (ITAT) correct in directing the Assessing Officer to reconsider the transfer pricing adjustment by following the ratios of previous decisions in similar cases?

Facts:

1. The case pertains to the assessment year 2008-09.

2. The Transfer Pricing Officer (TPO) determined the Arm's Length Price of syndication fee at 100% and added Rs.22,63,47,950/- to the assessee's income.

3. The Commissioner of Income Tax (Appeals) upheld the Assessing Officer's findings.

4. The ITAT remanded the matter back to the Assessing Officer for fresh consideration, citing previous decisions in similar cases.

5. The Revenue appealed this decision to the High Court under Section 260A (of Income Tax Act, 1961).

Arguments:

Revenue's Arguments:

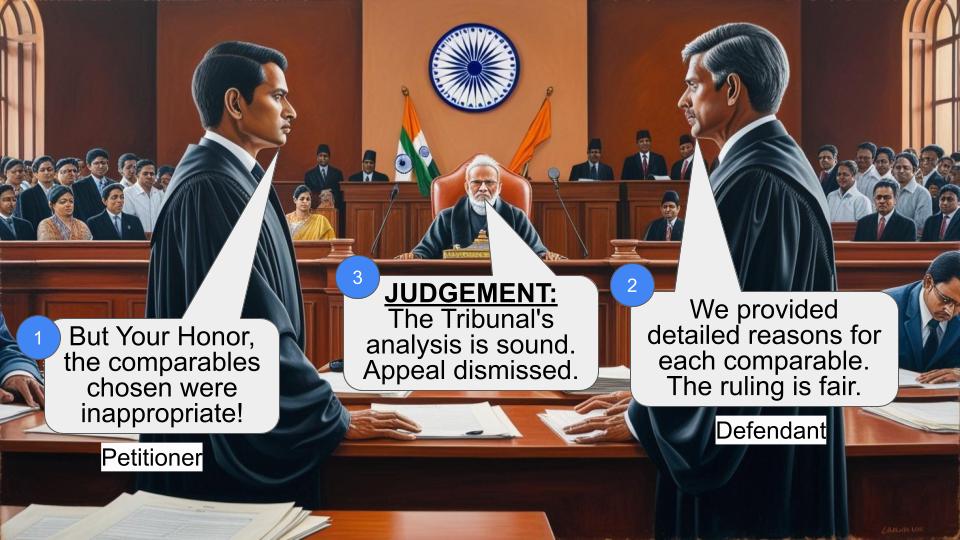

1. The ITAT erred in directing the Assessing Officer to follow ratios from cases with dissimilar facts.

2. The ITAT's direction to apply a 20% rate violated Section 92(3) (of Income Tax Act, 1961), as the assessee had considered a 50% rate.

Assessee's Arguments:

While not explicitly stated, it can be inferred that the assessee supported the ITAT's decision to remand the case for fresh consideration.

Key Legal Precedents:

1. M/s Credit Lyonnais Vs. ADIT (ITA No.1935/Mum/2007 dated 30.09.2013): This case held that for transfer pricing adjustments, only fees and charges (excluding interest) received by foreign branches should be considered. It suggested a 20% rate for adjustment.

2. Calyon Bank Vs. DDIT (ITA No.4474/M/2009 dated 21.03.2014): This case relied on the M/s Credit Lyonnais decision.

Judgement:

1. The High Court dismissed the Revenue's appeal.

2. The court found no error in the ITAT's decision to remand the matter to the Assessing Officer for fresh consideration.

3. The court held that the proposed questions of law did not arise from the ITAT's order.

FAQs:

Q1: What was the main issue in this case?

A1: The main issue was whether the ITAT was correct in directing the Assessing Officer to reconsider the transfer pricing adjustment based on previous decisions in similar cases.

Q2: Why did the High Court dismiss the appeal?

A2: The High Court found no error in the ITAT's decision to remand the case for fresh consideration and determined that the questions of law proposed by the Revenue did not arise from the ITAT's order.

Q3: What guidance did the ITAT provide for the fresh assessment?

A3: The ITAT directed the Assessing Officer to consider only the fees and charges (excluding interest) received by foreign branches when making transfer pricing adjustments, based on the M/s Credit Lyonnais case.

Q4: What is the significance of this judgment for transfer pricing cases?

A4: This judgment emphasizes the importance of considering relevant precedents and properly determining the Arm's Length Price in transfer pricing cases, even if it means remanding the case for fresh consideration.

Q5: Does this judgment provide a definitive ruling on the transfer pricing dispute?

A5: No, the judgment doesn't provide a final ruling on the transfer pricing dispute itself. Instead, it upholds the ITAT's decision to have the case reconsidered by the Assessing Officer, taking into account specific precedents and principles.

1. Heard Mr. Suresh Kumar, learned standing counsel, Revenue for the appellant and Mr. P. J. Pardiwalla, learned senior counsel for the respondent/assessee.

2. This appeal has been preferred by the Revenue

under Section 260A (of Income Tax Act, 1961) (briefly

“the Act” hereinafter) assailing the legality and

correctness of order dated 2nd January, 2017 passed by

the Income Tax Appellate Tribunal (ITAT), Mumbai in ITA

No.5997/Mum/2013 for the assessment year 2008-09.

3. The appeal has been preferred on the following

questions, projected as substantial questions of law:-

“(i) Whether on facts and circumstances of

the case and in law, the ITAT was correct in

directing the Assessing Officer to follow the

ratio of decision in case of M/s Credit Lyonnais

(ITA No.1935/Mum/2007 dated 30.09.2013)

and M/s Calyon Bank (ITA No.4474/M/2009

dated 21.03.2014) when the facts of those

cases are not similar to facts of the assessee

and hence cannot be considered as a valid

comparable under Rule 10B (of Income Tax Rules, 1962)

so as to adopt the rates as adopted in those

cases?

(ii) Whether on the facts and circumstances

of the case and in law, the ITAT was correct

in directing the Assessing Officer to decide

the issue by applying rate of 20% in violation

of provision of section 92(3) (of Income Tax Act, 1961),

1961 when the assessee itself had considered

the rate of 50%?”

4. In the course of the assessment proceeding the

Transfer Pricing Officer passed an order dated 30th

September, 2011 under Section 92CA(3) (of Income Tax Act, 1961)

determining the arms length price of the syndication

fee at 100%. He held that the entire amount of

Rs.22,63,47,950/- was received by the assessee.

5. In the assessment order dated 25th January, 2012

which followed, the same was incorporated whereafter

an addition of Rs.22,63,47,950/- was made to the income

of the assessee.

6. On appeal before the first appellate authority,

Commissioner of Income Tax (Appeals) by his order dated

25th July, 2013 upheld the findings of the Assessing

Officer and dismissed the appeal.

7. Assessee thereafter preferred further appeal before

the Tribunal. Tribunal by the impugned order dated 2nd

January, 2017 remanded the matter back to the file of

the Assessing Officer to decide the issue afresh by

considering the decisions relied upon by the Tribunal for

allocation of non-syndication fee between the assessee

and associated enterprise after giving opportunity of

being heard to the assessee.

8. While passing the said order, Tribunal relied upon a

decision of the Coordinated Bench of the Tribunal in the

case of M/s Credit Lyonnais Vs. ADIT decided on

30th September, 2012 where it was held as under:-

‘8.8 Having held that para 4 of the Protocol

does not apply to the case of the assessee,

now, the question arises as to whether the

adjustment made by the authorities below is

justified. For making the adjustment, the

authorities below have taken into

consideration, the income towards interest as

well as the fee charged by the foreign branch

from the clients. It is pertinent to note that

when the loan is provided by the syndicate and

the assessee has not contributed to the loan

amount then as regards the income of interest,

the same cannot be attributed to the assessee

for providing the services of the financial

analysis of the borrowers, market condition

and regulatory environment in India. Since the

assessee has provided certain services for that

arms length charges can be determined as per

the provisions of transfer pricing regulation.

The TPO as well as CIT(A) has not brought out

any comparable for determination of the arms

length price but took the total income

comprising interest as well as other fees

charged by the foreign branches for allocation/

attribution to the assessee. In this case, the

ALP has not been determined by taking into

consideration uncontrolled similar transaction.

In our view, the interest cannot be taken into

account for attribution of income towards

service charges/fees and, therefore, in the

facts and circumstances of the case only the

fee charged by the foreign branches can be

taken into consideration for making

adjustment under transfer pricing provisions.

Accordingly, we direct the AO/TPO to make

adjustment in respect of the services

performed by the assessee for foreign currency

loan arranged for its existing clients by taking

into account only the fee and other charges

received by the foreign branches from the

borrowers in question. Since none of the

parties have come out with the suitable

comparables, therefore, we find that the

estimation made by the CIT(A) at the rate of

20% is just and proper, however, the same

would be only in respect of the fee and

charges other than interest received by the

foreign branches. Thus, these grounds of the

assessee are partly allowed.”

9. Further reference was made to another decision of a

Coordinated Bench of the Tribunal in the case of Calyon

Bank Vs. DDIT decided on 21st March, 2014 wherein

the decision in M/s Credit Lyonnais was relied upon.

10. Following the above decisions, Tribunal restored the

issue to the file of the Assessing Officer for a fresh

decision in accordance with law.

11. In the facts and circumstances of the case, we do

not find any error or infirmity in the view taken by the

Tribunal in remanding the matter back to the file of the

Assessing Officer for a fresh decision in accordance with

law.

12. On thorough consideration, we are of the opinion

that the proposed questions of law does not arise out of

the impugned order of the Tribunal.

13. In above view, Appeal is dismissed, but without any

order as to costs.

(MILIND N. JADHAV, J.) (UJJAL BHUYAN, J.)

×

Similar Ripples

Questions

Tax Appeal Dismissed: Court Upholds Tribunal's Decision on Transfer Pricing Dispute

Write your CommentSimilar Posts

Generic

- Reportdata/6319.pdf