Tax Exemption Upheld: High Court Dismisses Revenue's Appeal in Capital Gains Ca…

Full News

Tax Exemption Upheld: High Court Dismisses Revenue's Appeal in Capital Gains Case

Tax Exemption Upheld: High Court Dismisses Revenue's Appeal in Capital Gains Case

This case involves an appeal by the Commissioner of Income Tax (the Revenue) against Smt. Umayal Annamalai (the assessee) regarding the interpretation of Section 54F (of Income Tax Act, 1961). The High Court dismissed the Revenue's appeal, upholding the Income Tax Appellate Tribunal's decision to grant the assessee exemption under Section 54F (of Income Tax Act, 1961) for capital gains earned during the previous year.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Smt. Umayal Annamalai (High Court of Madras)

T.C.A.No.456 of 2017

Date: 22nd July 2020

Key Takeaways:

1. The court emphasized a liberal interpretation of Section 54F (of Income Tax Act, 1961), considering it a beneficial provision for taxpayers.

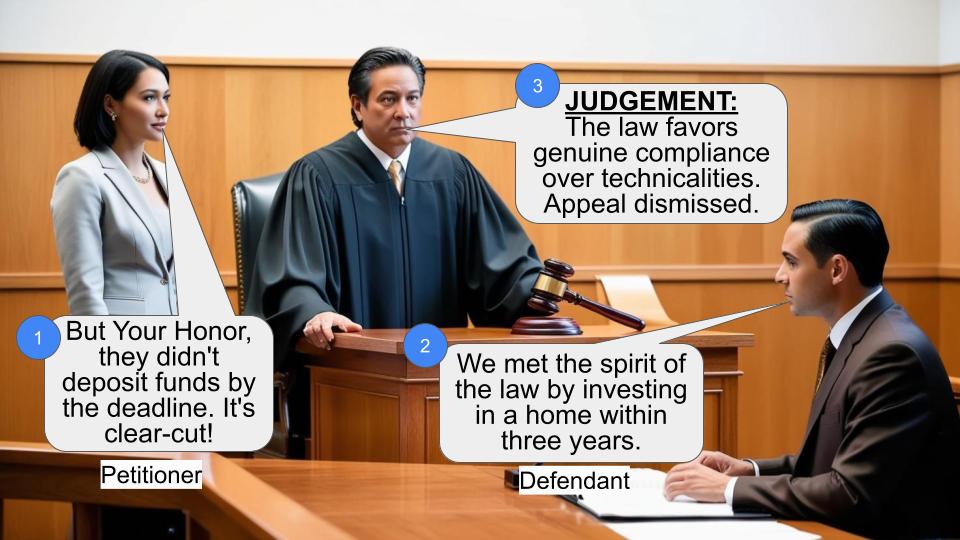

2. Compliance with the conditions of Section 54F(1) (of Income Tax Act, 1961), particularly the purchase and construction of residential property within three years from the date of transfer of the original asset, is crucial for claiming exemption.

3. The court prioritized the genuineness of transactions and factual aspects over strict adherence to filing deadlines.

Issue:

Was the Income Tax Appellate Tribunal justified in granting exemption under Section 54F (of Income Tax Act, 1961) when the unutilized portion of the sale proceeds was not deposited in the Capital Gains Account Scheme before the due date for filing the return under Section 139(1) (of Income Tax Act, 1961)?

Facts:

- The assessee earned capital gains during the previous year.

- Key dates:

- Date of transfer of original asset: 14.2.2005

- Date of filing return: 17.3.2006

- Due date of return for Assessment Year 2005-06: 31.07.2005

- Due date of filing belated return: 31.03.2007

- Possession of the new property: 15.12.2007

- The assessee invested Rs. 68,00,000/- before the due date of filing the belated return (31.03.2007).

- The assessee took possession of the new property on 15.12.2007, within three years from the date of transfer of the original asset.

Arguments:

Revenue's Arguments:

1. The exemption under Section 54F (of Income Tax Act, 1961) should not be granted as the unutilized portion of the sale proceeds was not deposited in the Capital Gains Account Scheme before the due date for filing the return.

2. The Tribunal's interpretation of Section 54F (of Income Tax Act, 1961) was incorrect.

Assessee's Arguments:

1. The conditions of Section 54F(1) (of Income Tax Act, 1961) were complied with by purchasing and constructing residential property within three years from the date of transfer of the original asset.

2. Section 54F (of Income Tax Act, 1961) should be interpreted liberally as it is a beneficial provision.

Key Legal Precedents:

The judgment doesn't explicitly mention any specific legal precedents. However, it notes that the Commissioner of Income Tax (Appeals) relied on legal provisions, the assessee's submissions, and judicial decisions in making their decision.

Judgement:

1. The High Court dismissed the Revenue's appeal, finding no substantial question of law arising from the case.

2. The court agreed with the Tribunal's findings, stating they were "perfectly in order and justified and correct" based on the facts.

3. The court held that the assessee had satisfied the conditions for availing the benefit of exemption under Section 54F (of Income Tax Act, 1961) by purchasing new property and taking possession within the stipulated period of three years.

4. The court emphasized the importance of considering the factual aspects, genuineness of transactions, and the beneficial nature of the provisions in Section 54F (of Income Tax Act, 1961).

FAQs:

1. Q: What is Section 54F (of Income Tax Act, 1961)?

A: Section 54F (of Income Tax Act, 1961) provides for exemption on capital gains arising from the transfer of certain capital assets if the proceeds are invested in a residential house.

2. Q: Why did the court emphasize a liberal interpretation of Section 54F (of Income Tax Act, 1961)?

A: The court considered Section 54F (of Income Tax Act, 1961) as a beneficial provision for taxpayers, and therefore believed it should be interpreted liberally to serve its intended purpose.

3. Q: What was the main reason for dismissing the Revenue's appeal?

A: The court found that the assessee had complied with the conditions of Section 54F(1) (of Income Tax Act, 1961) by purchasing and constructing residential property within the stipulated three-year period from the date of transfer of the original asset.

4. Q: Does this judgment set a precedent for similar cases?

A: While each case is unique, this judgment emphasizes the importance of considering the factual aspects and genuineness of transactions in interpreting Section 54F (of Income Tax Act, 1961), which could influence similar cases in the future.

5. Q: What is the significance of the Capital Gains Account Scheme in this case?

A: Although the assessee didn't invest in the Capital Gains Account Scheme before the due date under Section 139(1) (of Income Tax Act, 1961), the court prioritized the actual investment in residential property within the stipulated time frame over this technicality.

The Court was held by Video Conference, as per the Resolution of the Full Court dated 3 July 2020, by Judges at their respective residences and the counsel, staff of the Court appearing from their respective residences.

2. Heard Mr.J.Narayanaswamy, learned Senior Standing counsel appearing for the appellant Department and Mr.N.Quadir Hoseyn, learned counsel appearing for the respondent.

3. The Revenue has filed the present appeal under Section 260-A (of Income Tax Act, 1961), purportedly raising the following substantial questions of law for consideration.

“ 1. Whether on the facts and in the circumstances of the case the tribunal was right and justified in granting exemption u/s 54F (of Income Tax Act, 1961) when the unutilised portion of the sale proceeds were not deposited in the capital gains account scheme before the due date for filing of return u/s 139(1) (of Income Tax Act, 1961)?

2. Whether on the facts and in the circumstances of the case the tribunal was right in interpreting the provisions of section 54F (of Income Tax Act, 1961) to conclude that the assessee is entitled for exemption ignoring the ration of the decisions reported in 197 taxman 52?'

4. The learned Tribunal, with regard to exemption under Section 54F(1) (of Income Tax Act, 1961), with respect to capital gains earned by the assessee during the previous year, has given the following finding of facts in paragraph 8 and the relevant portion of paragraph 8 is quoted hereunder;

The assessee has complied the provisions considering the dates as under:-

(i) Date of transfer of original asset : 14.2.2005

(Ii) The date of filing of return : 17.3.2006

(iii) Due date of return for the Assessment year 2005-06 : 31.07.2005

(iv) Due date of filing belated return : 31.03.2007

(v) Possession of the property : 15.12.2007

"On considering the provisions of law and facts of the case, the assessee has invested Rs.68,00,000/-before due date of filing belated return i.e. 31.03.2007 and took the possession as per the findings of the Commissioner of Income Tax (Appeals) on 15.12.2007, being within three years from the date of transfer/sale of original asset being 14.02.2005. The assessee has not invested in Capital Gain Account Scheme before 139(1) of the Act but complied with the conditions u/s.54F(1) (of Income Tax Act, 1961) by purchasing and construction of residential property within three years from the date of transfer of original asset which is not disputed in the assessment proceedings or in appellate proceedings. The provisions of Sec. 54F (of Income Tax Act, 1961) are beneficial provisions and are to be considered liberally in the aspect of limitation period. But the investment in residential property is must which the assessee has proved with evidence and complied before the lower authorities. The learned Commissioner of Income tax (Appeals) relied on the legal provision and submissions of the assessee exhaustively with judicial decisions. Considering the factual aspects, genuineness of the transactions and beneficial aspects of the provisions, we are of the opinion that the Commissioner of Income Tax (Appeals) has rightly construed the findings and the explanation of the assessee with observation in his order and allowed the deduction u/s.54F (of Income Tax Act, 1961). Therefore, we are not inclined to interfere with the order of Commissioner of Income Tax (Appeals) and dismiss the ground of the Revenue.'

5. Though the Revenue stake involved in the present case is much below the limit of rupees one crore for withdrawal of the appeal by the Revenue, since the present case involved some audit objection because of exemption in the said Circular, the learned counsel for the Revenue press the appeal on merits.

6. However, after hearing both the learned counsel, we are satisfied that the finding of the facts arrived at by the learned Tribunal are perfectly in order and justified and correct on the basis of facts stated in the quoted paragraph 8 of the order. The assessee has clearly satisfied the conditions for availing the benefit of exemption under section 54F (of Income Tax Act, 1961), as it has purchased new property and has taken the possession within the stipulated period of three years, as aforesaid. Thus, we do not find any perversity in the said findings of facts given by the learned Tribunal.

7. Therefore, in our opinion, no substantial question of law arises in the present appeal filed by the Revenue and it is without any merits. Accordingly, the appeal filed by the Revenue is dismissed. There shall be no order as to costs.

DR. VINEET KOTHARI, J.

&

KRISHNAN RAMASAMY,J.

×

Similar Ripples

Questions

Tax Exemption Upheld: High Court Dismisses Revenue's Appeal in Capital Gains Case

Write your CommentSimilar Posts

Generic

- Reportdata/6212.pdf