Full News

Tax Tribunal Upholds Assessee's Revised Income Declaration, Overrules Revenue's Appeal

Tax Tribunal Upholds Assessee's Revised Income Declaration, Overrules Revenue's Appeal

This case involves an appeal by the Income Tax Department against an order of the Income Tax Appellate Tribunal (ITAT) that favored the assessee. The dispute centered around the amount of income surrendered by the assessee during a tax survey and subsequent revised tax returns. The ITAT's decision to accept the assessee's revised declaration was upheld by the High Court, dismissing the revenue department's appeal.

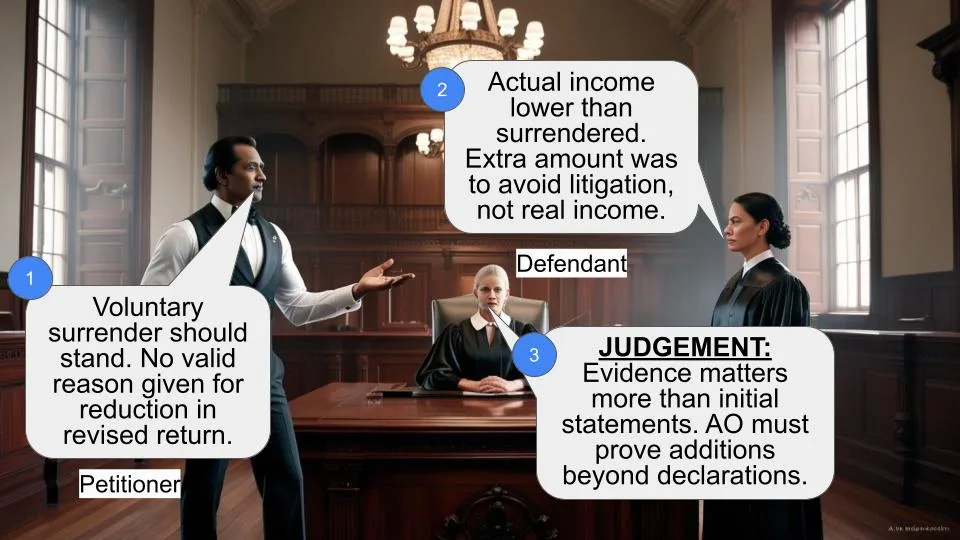

Case Name**: Commissioner of Income Tax vs Ashok Kumar Jain **Key Takeaways**: 1. Voluntary surrenders during tax surveys are not binding if the assessee provides proper explanations later. 2. The Assessing Officer must provide concrete evidence to support additions beyond the assessee's declarations. 3. The ITAT's factual findings based on evidence appreciation are generally not interfered with by higher courts. **Issue**: Whether the Income Tax Appellate Tribunal (ITAT) was correct in accepting the assessee's revised income declaration of Rs. 3 crore instead of the Rs. 5 crore initially surrendered during a tax survey? **Facts**: 1. A survey under Section 133A (of Income Tax Act, 1961) was conducted at the assessee's business premises on 25/11/2009. 2. During the survey, the assessee initially surrendered a total of Rs. 8 crore across three assessment years, including Rs. 5 crore for the assessment year 2008-09. 3. In the revised return for 2008-09, the assessee declared only Rs. 3 crore instead of Rs. 5 crore. 4. The Assessing Officer (AO) made an addition of Rs. 2 crore based on the initial surrender. 5. The Commissioner of Income Tax (Appeals) gave partial relief, sustaining only Rs. 50 lacs of the addition. 6. The ITAT allowed the assessee's appeal and deleted the entire addition of Rs. 2 crore. **Arguments**: Revenue's Arguments: 1. The initial surrender of Rs. 5 crore was voluntary and should be adhered to. 2. No valid reason was provided for reducing the surrendered amount in the revised return. 3. The ITAT's order was perverse in accepting the assessee's entire claim without proper reasoning. Assessee's Arguments: 1. The actual income based on peak credits and documents was lower than Rs. 3 crore. 2. An additional amount was surrendered to maintain peace and avoid litigation. 3. The funds from the previous year's surrender (2007-08) had rotated and were available for investments in the current year. **Key Legal Precedents**: No specific legal precedents were cited in the judgment. However, the court emphasized the principle that the Assessing Officer must bring on record cogent material and evidence to support additions rather than relying solely on statements made during surveys. **Judgement**: 1. The High Court dismissed the revenue's appeal, upholding the ITAT's order. 2. The court found that the ITAT's conclusion was based on appreciation of evidence and was a finding of fact. 3. The court noted that the AO had not found any additional evidence from the survey beyond the recorded statements. 4. The court agreed with the ITAT that the funds from the previous year's surrender and the current year's declaration had a direct nexus to the investments made. 5. The court emphasized that if an assessee doesn't adhere to a survey surrender, it's the AO's responsibility to provide cogent evidence for additions. **FAQs**: Q1: Why did the court dismiss the revenue's appeal? A1: The court found that the ITAT's decision was based on appreciation of evidence and was a finding of fact. No substantial question of law arose from the ITAT's order that required the High Court's intervention. Q2: What is the significance of this judgment for taxpayers? A2: This judgment emphasizes that statements made during tax surveys are not binding if the assessee can later provide proper explanations and evidence for a lower income declaration. Q3: What responsibility does the Assessing Officer have in such cases? A3: The AO must bring on record cogent material and other evidence to support any additions beyond what the assessee has declared, rather than relying solely on statements made during surveys. Q4: Can a taxpayer revise their income declaration after a survey? A4: Yes, this case shows that a taxpayer can revise their income declaration after a survey if they can provide proper explanations and evidence to support the revised figure. Q5: What role did the previous year's surrendered income play in this case? A5: The court accepted the argument that the previous year's surrendered income (2007-08) had rotated and was available as funds for investments in the current year (2008-09), establishing a direct nexus between the declared income and investments.

1. This appeal u/s 260-A (of Income Tax Act, 1961) (for short, 'IT Act') is directed against the order of the Income Tax Appellate Tribunal (for short, 'ITAT') dt.16/04/2013 and it relates to the assessment year 2008-09.

2. Brief facts, which can be noticed on perusal of the order impugned and the arguments of the counsel for the appellant, are that in the case of the respondent-assessee a survey u/s 133 (of Income Tax Act, 1961) A of the IT Act was carried out at the business premises on 25/11/2009 and during the course of survey some incriminating documents were found, inventorised and impounded, inventory of cash & stock was also prepared. At the time of survey, statement of the assessee-respondent was also recorded wherein on the basis of impounded loose papers, diaries, documents etc. he surrendered a total sum of Rs.8 crore which comprised of income of Rs.2 crore in the assessment year 2007-08; Rs.5 crore for the current year and Rs.1 crore for the assessment year 2009-10. In the assessment year 2007-08, though the assessee had surrendered Rs.2 crore but in the return of income an additional income was offered to the tune of Rs.1.5 crore only and even the AO was satisfied and accepted Rs.1.5 crore and he passed assessment order for the assessment year 2007-08 on 24/12/2009.

3. In the revised return, for the assessment year 2008-09 which is under appeal which the respondent-assessee filed pursuant to the said surrender, he surrendered a sum of Rs.3 crore only instead of Rs.5 crore which he admitted during the course of survey. A show cause notice was issued by the Assessing Officer (for short, 'AO') to the respondent-assessee wherein query was raised that as to when during the course of survey surrender was made to the tune of Rs.5 crore, then what was the reason for surrendering only Rs.3 crore in the revised return filed. It was explained by the assessee before the AO that the surrender of Rs.5 crore was made by him which was not correct as according to the transactions, in actuality and based on the peak credits and after having gone through the loose papers and documents, the actual surrender comes to lower than Rs.3 crore but to maintain peace and not to litigate the matter further, he has offered Rs.3 crore. He further contended that though the actual surrender on the basis of investment in shares application money,non-verifiable creditors etc or transactions recorded in the diary, comes to about Rs.2.20 crore only but he had additionally surrendered an amount of Rs.80 lacs on other defects, transaction in the diary or other transactions in the books of accounts so as to make the total surrender to the tune of Rs.3 crore and according to the assessee, the actual offer of Rs. 3 crore based on the material was proper and accordingly prayed for acceptance of the said surrender, however, the AO was not satisfied and merely because the assessee had surrendered an amount of Rs.5 crore, during the course of survey an addition of Rs.2 crore was made by the AO.

4. Dissatisfied with the addition of Rs.2 crore, as aforesaid, the matter was carried in appeal before the CIT(A) and the CIT (A), after analyzing the evidence on record and the explanation so offered, gave a further relief of Rs.1.50 crores and sustained addition to the tune of Rs. 50 lacs.

5. Dissatisfied with the deletion as well as sustenance, both i.e. the revenue as well as the assessee preferred appeal before the ITAT and the ITAT vide order impugned allowed appeal of the assessee and further deleted the amount of Rs.50 lacs and dismissed the appeal of the revenue and thus entire addition of Rs. 2 crore stood deleted which is assailed before us by the revenue.

6. Ld. counsel for the revenue contended that the surrender was voluntary. However, during the previous year relevant to the year under appeal, in the revised return, offer was made only to the tune of Rs. 3 crore as against to Rs.5 crore without assigning any reason. She contended that the assessee was well aware of the transactions recorded in the loose papers and other material and after complete satisfaction and deliberations, during the course of survey the assessee voluntarily offered Rs.

5 crores and there is no reason not to adhere to the said surrender and to wriggle out of the surrender or to restrict the amount at a later point of time. She further contended that no material was placed as to reducing the amount by Rs.2 crore out of the surrender made by the assessee earlier and surrender ought to have been at Rs. 5 crore, and such reduction is improper. She further contended that order of the Tribunal is perverse by accepting the total claim of the assessee and no reason is forthcoming by the ITAT and therefore, substantial question of law arise out of the order of the ITAT.

7. We have considered the arguments of the counsel for the revenue and have also gone through the impugned order.

8. In our view, the ITAT, after appreciating the evidence on record and the evidence placed by the assessee, has accepted the surrender to the tune of Rs. 3 crore which was made in the return of income and is based on appreciation of evidence and it is a finding of fact. The assessee gave an explanation supported by material on record, that on the basis of the documents and whatever was un-recorded in the diary/loose papers/other unverifiable creditors, the total amount of surrender came to the tune of Rs.2.20 crore only. However, additionally the assessee, on account of the other defects, transactions in diary or other transactions in the books of accounts, which might have escaped the attention of the assessee, offered further amount of Rs.80 lacs to make the total surrender to the tune of Rs.3 crore. Admittedly, even the AO has not pointed out any evidence or material entered in the loose papers or diaries or incriminating documents which could justify addition over and above of Rs. 3.00 crore or even Rs. 5.00 crore or more. The AO has not controverted the working/explanation offered by the assessee while working out surrender at Rs. 3.00 crore. If the assessee has offered an explanation then it was for the AO to highlight the mistakes or to prove that the transactions stated in loose papers/ documents depicted income to the tune of more than Rs. 3 crores or more. On perusal of the order of the AO, we notice that no exercise has been made by the AO as to hold that the surrender of Rs.3 crore made by the assessee was not proper. The explanation was offered by the assessee which was also considered by the CIT(A), who too was partly satisfied with the explanation and sustained addition of Rs.50 lacs by giving relief to the tune of Rs.1.5 crore. It was the claim of the assessee that the additional surrender made in the assessment year 2007-08 had rotated and constituted a fund and was available with assessee and thus there is a direct nexus of availability of funds. The said amount and the amount of surrender made during this year at Rs. 3 crore was available to the assessee for the investment in the share capital, etc. of Rs. 3,76,89,000/- requiring telescoping therein. As we have noticed earlier the AO has not found or bothered to found or traced anything additional as a result of survey from the assessee except relying on the recorded statements at the time of survey and therefore this view found favour with the two appellate authorities that the funds are arising from the same business and have a direct nexus and the income was invested/utilized during the year under consideration. In our view, the conclusion reached by the ITAT is based on the appreciation of evidence and is reached on the basis of finding of fact. It is also a finding of fact admittedly that in assessment year 2007-08 despite surrender in statements of Rs.2 crore the income was offered at Rs.1.5 crore only and accepted by the Revenue/A.O.

9. Thus, the ITAT, after appreciation of evidence, has come to the conclusion that the amount of Rs.1.5 crore, which was surrendered/offered in the assessment year 2007-08, was also available as a fund which came to be used partly in the investment of share capital, creditors or other investments as well as other defects, unverifiable creditors etc.

10. We may add that if the assessee does not adhere to the surrender made during the course of survey, then it is for the Assessing Officer to bring on record cogent material and other evidences to support the addition rather than rely on statements simplicitor.

11. In view of what we have observed herein above, no question much less substantial question of law can be said to emerge out of the impugned order of the ITAT and we do not find any infirmity or perversity in the order of the ITAT so as to call for any interference of this Court. In our view, no substantial question of law arise out of the order passed by the ITAT.

12. Consequently, the appeal, being devoid of merit, is hereby dismissed in limine.

[J.K. RANKA],J. [AJAY RASTOGI],J.

×

Similar Ripples

Questions

Tax Tribunal Upholds Assessee's Revised Income Declaration, Overrules Revenue's Appeal

Write your CommentSimilar Posts

Generic

- Reportdata/4581.pdf