Tax Tribunal Upholds Commission Payments, High Court Affirms Decision

Full News

Tax Tribunal Upholds Commission Payments, High Court Affirms Decision

Tax Tribunal Upholds Commission Payments, High Court Affirms Decision

This case involves the Commissioner of Income Tax (appellant) challenging a decision made by the Income Tax Appellate Tribunal (ITAT) in favor of Septu India (P) Ltd. (respondent). The ITAT had allowed the respondent's claim for commission and service expenses, which the Income Tax Department had initially disallowed. The High Court upheld the ITAT's decision, finding no reason to interfere with the Tribunal's factual findings.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Septu India (P) Ltd. (High Court of Punjab & Haryana)

ITA No. 608 of 2007

Date: 6th February 2008

Key Takeaways:

1. The Tribunal's factual findings, when based on sufficient evidence, are generally not interfered with by higher courts.

2. Actual payment and receipt of commission/service expenses can be crucial in proving the legitimacy of such claims.

3. Disallowance of expenses solely due to lack of documentary evidence may not be justified if other forms of proof are available.

Issue:

Was the Income Tax Appellate Tribunal (ITAT) correct in law when it deleted the addition made by the Assessing Officer on account of commission paid, even though the assessee allegedly failed to provide details showing that real services were rendered by the commission recipients?

Facts:

1. Septu India (P) Ltd. claimed commission expenses of Rs.10,38,860/- on the sale of machinery worth Rs.1,03,88,600/- to M/s. K.C. Cements Inds. Limited.

2. The company also claimed service charges of Rs.1,29,600/- for the sale of a plant worth Rs.10.80 lacs to M/s. Kanshi Ram Madan Lal.

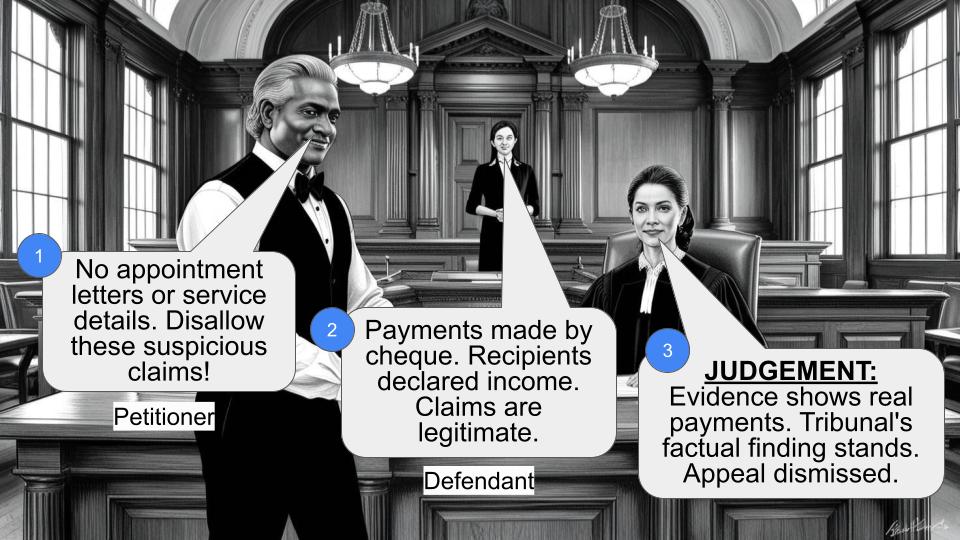

3. The Assessing Officer disallowed both expenses, citing lack of appointment letters and details of commission/service charges paid.

4. The Commissioner of Income Tax (Appeals) confirmed the addition.

5. The ITAT, on further appeal, deleted the addition.

Arguments:

Assessee's arguments:

1. Commission was paid for procuring orders.

2. Payments were made by cross account payee cheques.

3. Correspondence and MOU with parties were provided as evidence.

4. Commission recipients were assessed to tax and declared the income.

Revenue's arguments:

1. No agreement of appointment for commission agents was provided.

2. The parties receiving commission were engaged in unrelated businesses (wine and cement).

3. Insufficient documentary evidence was provided to support the claim.

Key Legal Precedents:

The judgment doesn't explicitly mention any specific legal precedents. However, it relies on the principle that findings of fact by the Tribunal, when based on sufficient evidence, should not be interfered with by higher courts.

Judgement:

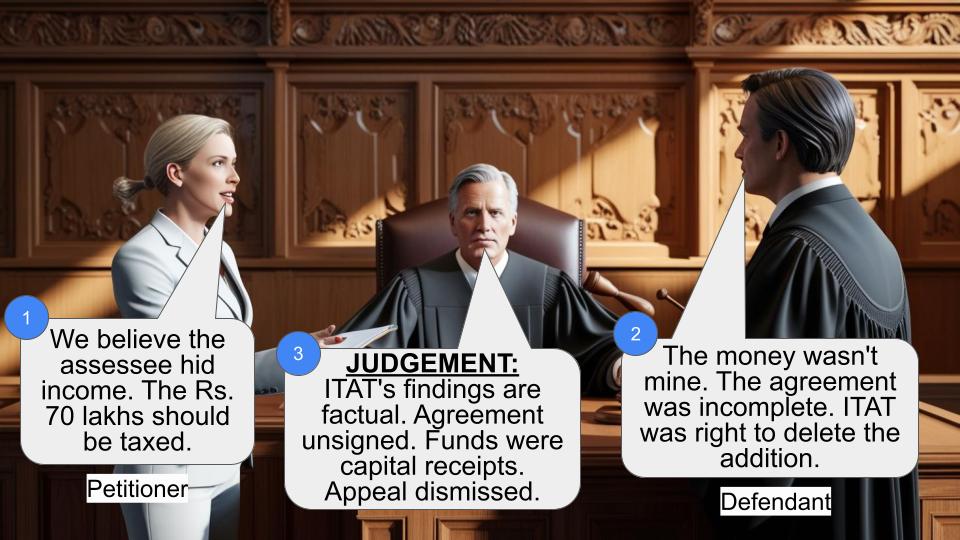

1. The High Court dismissed the appeal filed by the Commissioner of Income Tax.

2. The court found that the ITAT had based its conclusion on sufficient evidence proving the actual payment of commission/service expenses.

3. The High Court agreed that when actual payment and receipt are proved, claims should not be disallowed merely due to lack of documentary evidence.

4. The court viewed the ITAT's decision as a pure finding of fact, which doesn't require interference in appeal.

5. No substantial question of law was found to be involved in the appeal.

FAQs:

Q1: Why did the High Court uphold the ITAT's decision?

A1: The High Court found that the ITAT had based its decision on sufficient evidence and considered it a pure finding of fact, which doesn't typically warrant interference from higher courts.

Q2: What kind of evidence did the assessee provide to support their claim?

A2: The assessee provided copies of account statements showing bank details and cheque numbers, correspondence regarding order procurement, and even a Memorandum of Understanding (MOU) with one of the parties.

Q3: Why was the initial disallowance by the Assessing Officer overturned?

A3: The ITAT and High Court found that actual payment and receipt of the commission were proved, which was considered more important than the lack of certain documentary evidence.

Q4: Does this case set any new legal precedent?

A4: While it doesn't set a new precedent, it reinforces the principle that factual findings by tribunals, when based on sufficient evidence, should generally not be interfered with by higher courts.

Q5: What lesson can taxpayers learn from this case?

A5: While documentary evidence is important, proving actual payment and receipt of expenses can be crucial in defending tax deductions, even in the absence of formal agreements or appointment letters.

The instant appeal filed by the revenue is directed against the order dated 22.12.2006 passed by the Income Tax Appellate Tribunal, Delhi Bench “D” New Delhi (hereinafter referred to as `the ITAT') in ITA No.2011/DEL/03 in case of the respondent for the Assessment Year 1997-98 by raising the following substantial question of law:-

Whether, on the facts and in the circumstances of the case, the Hon'ble ITAT was right in law in deleting the addition on account of commission paid though assessee failed to discharge its onus to provide any details to show that real services were rendered by persons to whom commission had been paid?

In this case, the assessee had given commission of Rs.10,38,860/- on sale of machinery worth Rs.1,03,88,600/- to M/s. K.C. Cements Inds. Limited. Similarly it also paid an amount of Rs.1,29,600/- as service charges in execution of sale of plant worth Rs.10.80 lacs to M/s. Kanshi Ram Madan Lal.

The Assessing Officer disallowed both the expenses on the ground that the assessee failed to furnish appointment letters of commission agents, details of commission/service charges paid. On appeal by the assessee, the Commissioner of Income Tax (Appeals) confirmed the said addition. On further appeal filed by the assessee, the ITAT deleted the said addition while observing as under:-

“We have heard the parties and perused the record of the case. The assessee claimed to have paid comm @ 10% of Rs.10,38,860/- on sale of machinery to K.C. Cement Ltd. and Rs.1,29,600/- on sale of plant to Mr. Kanshi Ram Madan Lal. The Assessing Officer disallowed the claim of the assessee on the ground that there were no agreement of appointment of these parties as commission agents. The Assessing Officer noticed that these parties were found to have been engaged in totally diametrically different business, one is in wine business and other is engaged in cement business. The assessee claimed that commission was paid for procuring orders by these parties. The sales were made to M/s. Kishan Dehyration, National High Way, Bhojpura P.O., Gondal, Distt. Rajkot (Gujarat) (P.155/PB) and Neelkanth Polymers (P.160/PB). The payment of commission is made by cross account payee cheques. The assessee has filed the copies of statement of account of these parties showing the name of banks and cheque nos. and amount credited in their accounts at page 152 and 159 of paper book. The necessary correspondence entered into between the assessee and these parties regarding procurement of orders are also placed on record (page 152 to 162/PB). There is even MOU dated 25.4.96 signed with one of the parties (M/s. K.C.Cement Ltd.) for procurement of order which is available at page 161/PB. The name of the parties and their address from whom supplies were made would appear from these correspondence. The claim that the parties to whom the commission was paid are assessed to tax and have shown the same as income in their return has not been disputed by the Revenue. The Revenue has made no further enquiry with parties to whom the sale have been made by assessee to ascertain as to whether the purchase orders were made by them on account of the effort/services of these commission agents. In the facts and circumstances of the case, we are of the view that there is no justification to disallow the claim of payment of commission to these parties. We, therefore, direct to delete the same.”

In our opinion, the ITAT has come to the aforesaid conclusion on the basis of sufficient evidence available on the record which clearly prove that the amount of commission/service expenses was actually paid by the assessee to those parties. The ITAT on the basis of the said evidence has recorded a pure finding of fact while coming to the conclusion that the assessee has clearly proved the payment of the aforesaid two amounts to the above-said parties. In our opinion, when the assessee has proved the actual payment of the aforesaid amounts as well as receipt of the same amount by the above-said parties, then the claim put forth by the assessee should not have been disallowed merely on the ground that the same was not supported by any documentary evidence.

Therefore, in our view the ITAT has rightly held that the adjudicating authorities below were not justified in disallowing the deduction claimed by the assessee. In our view, a pure finding of fact has been recorded by the ITAT which does not require any interference in this appeal.

No substantial question of law is involved in this appeal.

Dismissed.

(SATISH KUMAR MITTAL)

JUDGE

(RAKESH KUMAR GARG)

JUDGE

February 06, 2008

×

Similar Ripples

Questions

Tax Tribunal Upholds Commission Payments, High Court Affirms Decision

Write your CommentSimilar Posts

Generic

- Reportdata/4882.pdf