Tribunal's Factual Findings on Tax Deduction Upheld by High Court

Full News

Tribunal's Factual Findings on Tax Deduction Upheld by High Court

Tribunal's Factual Findings on Tax Deduction Upheld by High Court

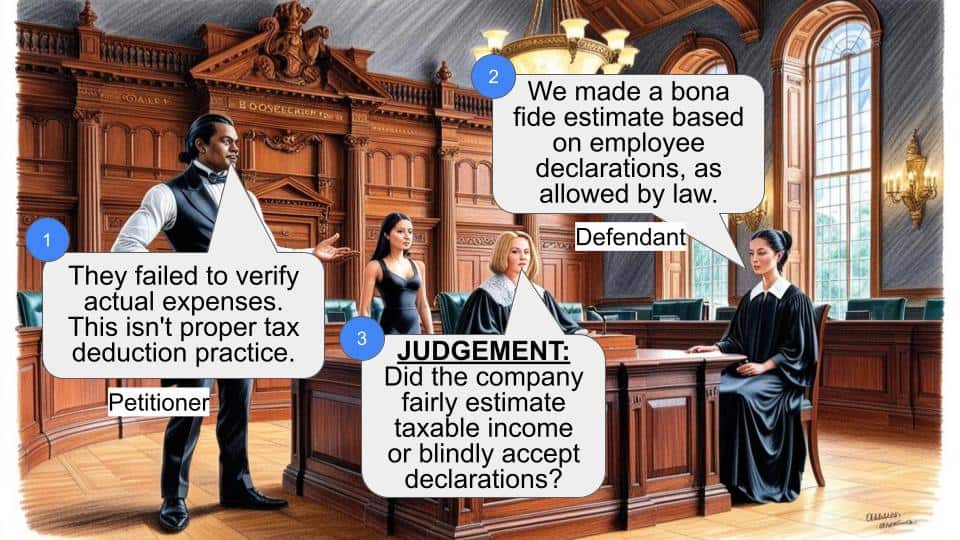

This case involves a dispute between the Commissioner of Income Tax and Nicholas Piramal India Ltd. regarding the company's tax deduction practices for children's education allowance and leave travel allowance (LTA) paid to its employees. The key issue was whether the company had fairly estimated the taxable income for the purpose of tax deduction at source, or if it had blindly accepted the declarations filed by its employees without verifying the actual expenditure incurred.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs. Nicholas Piramal India Ltd. (High Court of Bombay)

Income Tax Appeal No.432 of 2001

Date: 15th January 2008

Key Takeaways:

1. The Tribunal's factual findings that the company had not blindly accepted the employee declarations, but had fairly estimated the taxable income, were upheld by the High Court.

2. The court emphasized that the test for the company's actions is whether it made a bona fide estimate of the taxable income, not whether it verified every detail of the employee declarations.

3. The High Court distinguished this case from previous rulings where the issue was the failure to deposit the deducted tax, rather than the estimation of taxable income.

Issue:

Whether the Tribunal was justified in holding that the company had fairly estimated the taxable income for the purpose of tax deduction at source, based on the employee declarations, without verifying the actual expenditure incurred.

Facts:

- The Income Tax Department had raised demands on the company, alleging that it had wrongly treated the children's education allowance and LTA as exempt from tax.

- The Department claimed the company had blindly accepted the employee declarations without verifying the actual expenditure.

- The Tribunal, after considering the employee declarations and affidavits, held that the company had not acted dishonestly and had fairly estimated the taxable income.

- The High Court was hearing the Department's appeal against the Tribunal's decision.

Arguments:

- The Department argued that the company should have verified the actual expenditure incurred by the employees, rather than relying solely on their declarations.

- The company argued that it had made a bona fide estimate of the taxable income, as required under the law, and the Tribunal's factual findings on this should be upheld.

Key Legal Precedents:

- Glaxo India Ltd. v. First Income Tax Officer, TDS Circle, Bombay (1995): The Tribunal held that the test is whether the company made a bona fide estimate of the taxable income, not whether it verified every detail.

- Bennet Coleman & Co. Ltd. v. Mrs. V.P. Damle, ITO (1986) and Pentagon Engineering (P) Ltd. v. CIT (1995):

These cases dealt with the failure to deposit the deducted tax, which is distinguishable from the present case.

Judgment:

The High Court upheld the Tribunal's decision, holding that the Tribunal's factual findings on the company's fair estimation of the taxable income cannot be faulted. The court ruled that the questions of law framed by the Department did not arise, and dismissed the appeal.

FAQs:

Q1: Why did the High Court uphold the Tribunal's decision?

A1: The High Court found that the Tribunal's factual findings that the company had not blindly accepted the employee declarations, but had fairly estimated the taxable income, were reasonable and could not be faulted.

Q2: What is the key legal principle established in this case?

A2: The key principle is that the test for the company's actions is whether it made a bona fide estimate of the taxable income, not whether it verified every detail of the employee declarations. As long as the company's estimation was reasonable, it does not have to scrutinize every aspect of the employee declarations.

Q3: How does this case differ from the previous rulings cited by the Department?

A3: The previous cases dealt with the failure to deposit the deducted tax, which is a different issue from the estimation of taxable income. In this case, the court found that the company had made a bona fide estimate, so the principles from the earlier cases did not apply.

Q4: What are the implications of this judgment?

A4: This judgment reinforces the principle that employers are expected to make a reasonable estimate of taxable income for the purpose of tax deduction, without being required to verify every detail of employee declarations. As long as the estimation is made in good faith, the employer will not be penalized.

The revenue has preferred this appeal on the following questions :

(i) Whether on the facts and in the circumstances of the case, the Tribunal was justified in law in holding that Children’s Education Allowance paid by the assessee to their employees at the fixed rate is exempt u.s.10(14) only on the basis of declaration filed by the employees without verifying actual expenditure incurred by the employee & maintaining records thereof & not including the same for the purpose of taxable income for the deduction of tax at source u.s. 192 of the I.T. Act, 1961?

(ii) Whether on the facts and in the circumstances of the case the Tribunal was justified in law in holding that L.T.A. paid by the assessee to their employees at the fixed rate is exempt u.s. 10(5) only on the basis of declaration field by the employees without verifying actual expenditure incurred by the employee & maintaining records thereof and not including the same for the purpose of taxable income for deduction of tax at source u.s. 192 of the I.T. Act, 1961?"

. The present appeal is in respect of assessment years 1995-96. That appeal was heard along with several other appeals which were disposed of by common order dated 6.6.2001. The A.O. observed that the children education allowances and Leave travel allowances were treated as exempted merely on the basis of declaration filed by the assessee and no sufficient proof of incurring expenditure either on the education of the children or on travel was examined by the assessee and as such held that the allowances were wrongly treated as exempted and consequently made demands. That order was confirmed in appeal by C.I.T. (Appeal) which held that by solely acting on the declarations obtained from the employees was not sufficient to form the honest belief as claimed by the assessee.

. The learned tribunal proceeded to pose to itself a question whether the employer/assessee had acted honestly and fairly or not? The tribunal considered the declarations given by the employees of the Assessee as also affidavits filed by the employees to the effect that they had incurred expenditure. It also noted that the T.D.S. is not effected only on the part of the allowances which is exempted and on the balance portion tax has duly been deducted and paid into the Government treasury. The tribunal as an illustration considered cases of two employees and on considering the facts therein, was of the opinion that it was difficult to hold that the assessee did not act honestly and fairly and or that there was any reason for the assessee to raise any suspicion with regard to the declaration filed by the employees. The tribunal held that it was not a case where the assessee had blindly accepted the declarations and for the aforesaid reasons, considering that the employer is expected to deduct tax only on estimated income and on facts on recording held that the assessee has fairly estimated the income and for that reasons, quashed the demands raised. In our opinion, these are purely findings of fact recorded by the tribunal with which no fault can be found.

. Apart from that our attention has been invited to the judgment on the similar issue in ITA No. 104 to 107/BOM/90 in Glaxo India Limited Vs. First Income Tax Officer, T.D.S. Circle, Bombay disposed of on 12.6.1995. In that case the issue pertains to short deductions in regard to the estimation of drivers salary as also of domestic servants. Various judgments were placed for consideration before the learned tribunal. The only issue was in respect of short deductions in salaries paid to the employees. The tribunal noted that on the facts on record, it cannot be said that the assessee has deliberately or dishonestly resorted to under estimation of the salary income of the employees for the purpose of deduction of tax at source. It noted that the deduction of tax at source is to facilitate the department to collect the tax earlier to assessment of the same. It does not mean that the department should blindly go by the returns filed by the employees in making the assessments of the employees. The tribunal held that what is to be seen for the purpose of Section 201 (of Income Tax Act, 1961) as it then stood was whether the assessee has made bona fide estimate for the purpose of deduction of tax. The tribunal held that from the details furnished the assessee has only made bona fide estimate. An application for reference which was made was rejected. An application was made to this court being Income Tax Application No. 171 of 1997 which was disposed of by this court by observing as under :

"Considering the fact that the tribunal has recorded a finding of fact which concludes the controversy, in our opinion no referable question of law arises. Hence, rejected."

. The revenue took out the matter in Appeal before the Supreme Court. The Special Leave Petition was dismissed.

. It will be clear therefore, that even if the amendment to section 201 (of Income Tax Act, 1961) has been applied retrospectively, the test whether the assessee acted bona fide is still available as what the assessee under Section 192(1) (of Income Tax Act, 1961) is called upon, is to deduct tax "on the estimated income". In our opinion, the facts in Glaxo (supra) would clearly apply. On behalf of the Revenue, the learned counsel had brought to our attention the judgment of this court in the case of Benett Coleman & Co. Ltd. Vs. V.P. Damle, Third Income Tax Officer, TDS Circle, Bombay, 157 ITR 812. In that case the assessee had deducted tax but failed to deposit the same. It is in this context that the court had observed that Section 201(1)(a) (of Income Tax Act, 1961) makes payment of simple interest mandatory. That case is clearly distinguishable and cannot be applied to the facts of the present case as the present case is of deduction on estimated income. Reliance is also placed on the judgment in Pentagon Engg. (P) Ltd. Vs. CIT, 212 ITR 92 Bombay. There again the issue for consideration was whether the tribunal was right in law in taking a view that the provisions of Section 201(1)(a) (of Income Tax Act, 1961) for levying interest is mandatory. Once it is held that the authority was deducting tax then there is no escapement from levying interest if that amount is not deposited. That is not the case here.

. Considering the findings of fact and the issue involved in this case, we are clearly of the opinion that the question of law as framed would not arise and consequently appeal is dismissed.

(R.S. MOHITE, J.) (F.I.REBELLO, J.)

×

Similar Ripples

Questions

Tribunal's Factual Findings on Tax Deduction Upheld by High Court

Write your CommentSimilar Posts

Generic

- Reportdata/5007.pdf