Full News

Windmill Tax Deduction Victory: Court Upholds Assessee’s Right to Deduction Without Offsetting Losses

Windmill Tax Deduction Victory: Court Upholds Assessee’s Right to Deduction Without Offsetting Losses

In this case, the court ruled in favor of the assessee, allowing them to claim a tax deduction under Section 80IA (of Income Tax Act, 1961) without having to offset losses or unabsorbed depreciation related to their windmill operations. This decision was challenged by the Revenue, but the court upheld the assessee’s entitlement to the deduction, reinforcing a precedent that supports businesses in similar situations.

Get the full picture - access the original judgement of the court order here

Case Name

Commissioner of Income Tax vs. SAS Hotels and Enterprises Ltd. (High Court of Madras)

T.C.A.Nos.741 to 743 of 2015 and M.P.Nos.1 & 1 of 2015

Date: 29th September 2015

Key Takeaways

- The court confirmed that the assessee can claim deductions under Section 80IA (of Income Tax Act, 1961) without setting off losses or unabsorbed depreciation from windmill operations.

- This decision aligns with previous rulings, such as in the case of “C.I.T. Vs. Yuvaraj” and “Velayudhaswamy Spinning Mills Vs Asst. CIT.”

- The ruling provides clarity and support for businesses investing in renewable energy projects, ensuring they can benefit from tax incentives without being penalized for past losses.

Issue

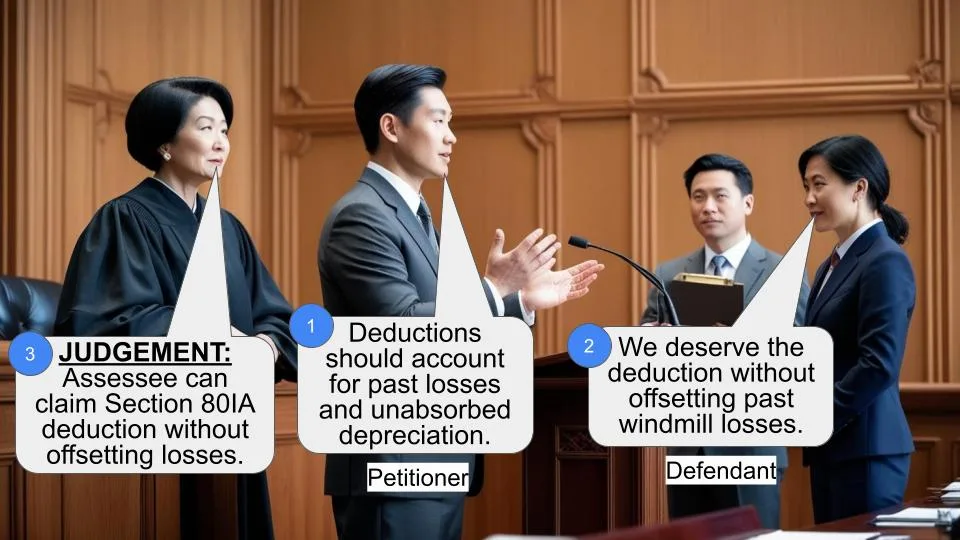

Can an assessee claim a deduction under Section 80IA (of Income Tax Act, 1961) without setting off losses or unabsorbed depreciation related to windmill operations?

Facts

The case involves SAS Hotels and Enterprises Ltd., which sought to claim a tax deduction under Section 80IA (of Income Tax Act, 1961) for their windmill operations. The Revenue challenged this, arguing that the deduction should not be allowed without setting off previous losses and unabsorbed depreciation. The case was brought to the High Court after the Tribunal ruled in favor of the assessee.

Arguments

- Assessee’s Argument: The assessee argued that they are entitled to the deduction under Section 80IA (of Income Tax Act, 1961) without the need to offset past losses or unabsorbed depreciation, as supported by previous court decisions.

- Revenue’s Argument: The Revenue contended that the deduction should only be allowed after setting off any losses or unabsorbed depreciation from the windmill operations, as these should be accounted for before claiming such benefits.

Key Legal Precedents

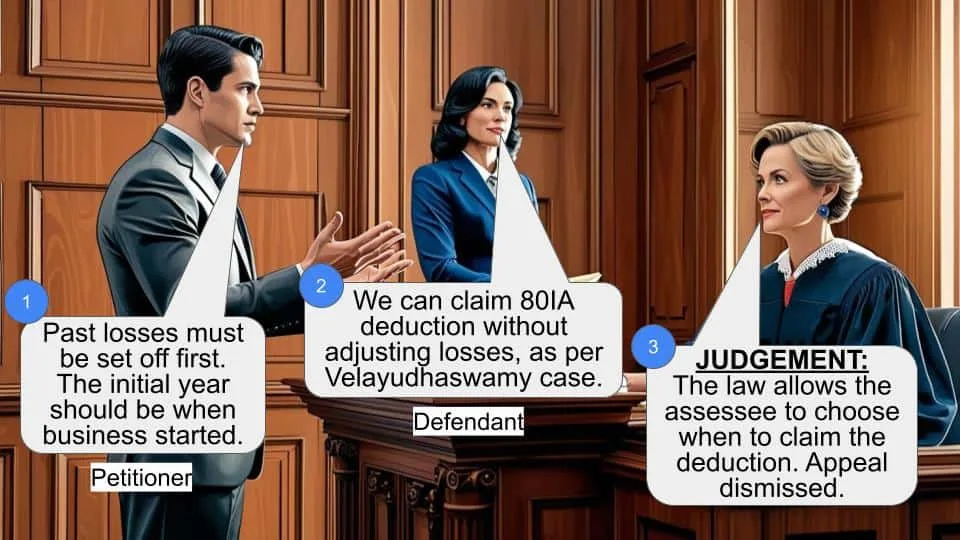

- C.I.T. Vs. Yuvaraj: This case supported the assessee’s position, allowing deductions without setting off losses.

- Velayudhaswamy Spinning Mills Vs Asst. CIT: Reinforced the principle that deductions under Section 80IA (of Income Tax Act, 1961) can be claimed without offsetting past losses, following the Supreme Court’s decision in “Liberty India Vs CIT.”

Judgement

The court ruled in favor of the assessee, SAS Hotels and Enterprises Ltd., affirming their right to claim the deduction under Section 80IA (of Income Tax Act, 1961) without setting off losses or unabsorbed depreciation related to their windmill operations. The court’s decision was based on established precedents, ensuring consistency in the application of tax laws for renewable energy projects.

FAQs

Q: What does this ruling mean for businesses with windmill operations?

A: It means that businesses can claim tax deductions under Section 80IA (of Income Tax Act, 1961) without having to offset past losses or unabsorbed depreciation, encouraging investment in renewable energy.

Q: Why did the court rule in favor of the assessee?

A: The court relied on previous legal precedents that support the assessee’s right to claim deductions without offsetting losses, ensuring consistency in the application of tax laws.

Q: How does this decision impact future cases?

A: This decision reinforces the legal framework that allows businesses to benefit from tax incentives for renewable energy projects, potentially influencing similar cases in the future.

These appeals are filed by the Revenue under Section 260-A (of Income Tax Act, 1961), 1961 raising the following substantial questions of law.

"(i) Whether the Appellate Tribunal was correct in following the earlier order of the Tribunal in assessee's own case without verifying the nature of issue therein?

(ii) Whether the Tribunal is correct in observing that this Court has not so far delivered any judgment against the order of the Tribunal in I.T.A.No.2176/Mds/2008 without considering the reported decision in (2011) 16 Taxmann.com 34 of the very same assessee ? and

(iii) Whether under the facts and circumstances of the case, the Income Tax Appellate Tribunal is right in law in holding that the assessee is entitled to deduction under Section 80IA (of Income Tax Act, 1961) without setting off the losses/unabsorbed depreciation pertaining to the windmill, which were set off in the earlier year against other business income of the assessee ?"

2. Though on the questions 1 and 2, the appellant/Revenue is entitled to have our answers in their favour, we did not think fit to admit the appeal and order notice, in view of the fact that in any case, the third question of law has to be answered against the appellant/Revenue, which would eventually lead to the dismissal of the appeal. Therefore, without ordering notice of admission, we have taken up the appeal.

3. In so far as the questions 1 and 2 are concerned, the same relates to a finding recorded by the Tribunal as though the issue on hand was covered by the decision of the Tribunal in I.T.A.No.2176/Mds/2008. But, the decision of the Tribunal in I.T.A.No.2176/Mds/2008 related to the method of accounting. The appeal filed by the Department was already disposed of in favour of the same assessee in 2011 (16) Taxmann.com 34. The case on hand has nothing to do with the decision rendered in I.T.A.No.2176/ Mds/2008. Therefore, the finding of the Tribunal in relation to this aspect is clearly erroneous and the questions 1 and 2 are liable to be answered in favour of the appellant.

4. However, on question No.3, we have already held in C.I.T. Vs. Yuvaraj [T.C.A.No.163 of 2015 dated 21.4.2015], following the decision of this Court in Velayudhaswamy Spinning Mills Vs Asst. CIT [2012) 340 ITR 477] that the Tribunal was right in holding that the assessee is entitled to deduction under Section 80IA (of Income Tax Act, 1961) without setting off the losses/unabsorbed depreciation pertaining to the windmill. The decision in Velayudhaswamy Spinning Mills followed the decision of the Supreme Court in Liberty India Vs CIT [2009) 317 ITR 218 (SC)].

5. Though we are inclined to answer questions 1 and 2 in favour of the appellant/Revenue, the appeal is dismissed in view of the fact that the same result would follow on account of our answer to the question No.3. Consequently, the above MPs are also dismissed.

29.9.2015

Internet : Yes

To

The Income Tax Appellate Tribunal 'A' Bench, Chennai.

V.RAMASUBRAMANIAN,J

AND

T.MATHIVANAN,J

T.C.A.Nos.741 to 743 of 2015

and M.P.Nos.1 and 1 of 2015

×

Similar Ripples

Questions

Windmill Tax Deduction Victory: Court Upholds Assessee’s Right to Deduction Without Offsetting Losses

Write your CommentSimilar Posts

Generic

- Reportdata/3415.pdf